The Week Ahead – Oil tops $100 as energy supply crisis dominates markets

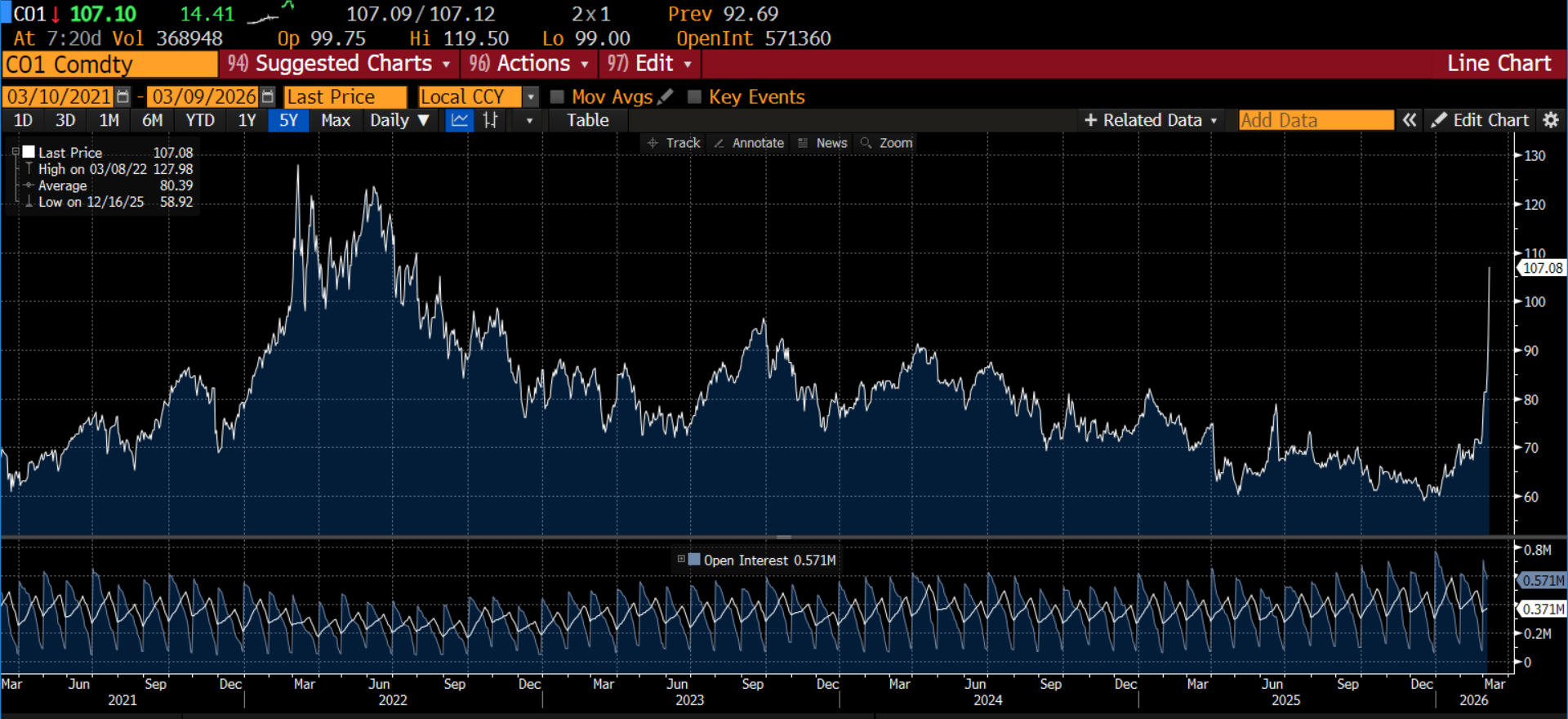

It finally happened, the price of oil surged at the open late on Sunday, with Brent crude rising from $93 to a high of $119, the highest level since 2022 on the back of supply shutdowns across the Gulf. At one stage, the WTI price jumped nearly 30%, its largest daily price gain ever. The oil price has moderated as we move through the morning, and Brent crude is currently trading just above $108 per barrel. As we wait for the start of the trading day, the oil price remains comfortably in triple figure territory, with huge ramifications for financial markets at the start of this week.

Chart 1: Oil price spikes to 2022 levels

Source: XTB and Bloomberg

Equity sell off gathers pace

The spike in the oil price is dominating global financial markets. There have been sharp losses in equities in Asia overnight, the Nikkei is lower by 5% and the Australian index is lower by nearly 3%. Equity futures markets are pointing to large losses across Europe and the US, and global bonds are tumbling. The UK 10-year Gilt yield is set to surge at the open on Monday, after a 26bp jump last week. The Italian yield, which is moving closely with UK Gilt yields is higher by another 12bps this morning. The UK is paying for natural gas than our European neighbors, so it is natural that our bond market sell off could be worse than Europe’s today.

This is likely to be another rough day for stocks and bonds as they sell off sharply. Precious metals are also lower as energy prices rip higher, as the impact from the war continues to dominate markets.

There was an escalation in attacks by both Iran and US forces over the weekend and there were more strikes on key energy infrastructure across the Gulf region, and further shutdowns in oil and gas production facilities. Although there are some key economic data releases this week, including US CPI and the UK GDP, developments in energy price markets will determine risk sentiment in the coming days.

Energy supply crisis

As we start a new week, the market is watching a deeper energy supply crisis. For example, Iraq is now producing a quarter of the oil it was producing before the US and Israeli air strikes on Iran. Iraq’s southern oilfields are now producing 1.3mn barrels per day, down from 4.3mn barrels per day. This is roughly 3% of global oil supply lost in a single event. Shockingly, this is worse than the oil supply situation after Russia attacked Ukraine.

Strait of Hormuz critical to energy prices

There is nothing wrong with the oil reservoirs in Southern Iraq, instead this is a storage crisis. Iraq has lost 3mn barrels per day of supply because the Strait of Hormuz is closed, with no ships passing through it during the weekend. Since Iraq derives 90% of its state revenue from oil exports, the risk is that a commodity crisis sparks a social crisis, if the situation persists.

The optimistic view

While there does not appear to be a deescalation of this conflict, if the Strait of Hormuz reopens in the coming weeks, then oil prices will fall. This is more likely to happen if Iran’s regime collapses. After intense bombing by US forces over the weekend, the Iranian regime is likely to be weakened even further, and the odds of a collapse of the regime are increasing as this dreadful conflict drags on. Any signs that the regime is on its way out could take the pressure off the oil price, and we think that markets will remain sensitive to news flow over the coming days.

Governments prepare for inflation spike

G7 finance ministers are preparing to meet later today. On the agenda is the potential release of strategic oil reserves to dampen inflationary threats. The finance ministers can only react to the situation, a ceasefire, or the collapse of the Iranian regime are the main factors necessary to calm the oil price right now.

However, a large release of strategic oil reserves could keep the oil price stable at these levels at the start of the week. There are some who argue a large decline in US and global equities, along with signs that the market is preparing for Fed rate hikes on the back of the oil price spike will force President Trump to deescalate the situation, but the hawkish comments from the US Secretary of War, that the US is close to winning, makes this less likely, and ordinary people around the world will face the consequences of the fall out from this conflict.

The growing economic and financial risks of a prolonged conflict

Zooming out from the oil price, Polymarket, the prediction marketplace, is pricing a mere 23% of a ceasefire between the US and Iran by the end of March, a week ago this was 44%. As we start a new week, we could see another bout of risk aversion, and a broad-based equity market sell off, as investors remain in panic mode. Oil prices well above $100 per barrel is souring the mood for investors this morning. The impact on the real economy will depend on the duration that oil prices remain at elevated levels. However, with petrol prices rising sharply already, we could see consumer confidence slump around the world. Although the US is a net oil exporter and is the world’s largest oil producer right now, the gasoline price rose by the most in two decades last week and was higher by more than 30%. In the UK, the price of a litre of unleaded has risen by 5p to an average of 137.5p, the price of diesel is nearly 150p. The rise in petrol costs is acting as a major drag on equity prices and if oil prices continue to move higher this week, then the pumps will move with it. The cost of living crisis is back, and it makes global rate cuts unlikely in the coming months.

Europe remains more vulnerable than US

The selloff in equities was worse in Europe than anywhere else globally. Although the UK index has a strong mix of big oil companies, utilities and defense firms, this only gave it a slim margin of resilience vs. the Eurostoxx 50 index last week. The FTSE 100 fell 6.23% on a currency-adjusted basis, vs, an 8.3% decline for the European index.

The spike in the oil price on Monday is having a big effect on equities, but the futures market is pointing to some further resilience in the FTSE 100 this morning. It is currently expected to open down 1.18%, as gains for the oil majors balance losses elsewhere.

Bond market risks

Last week, we saw the bond market sell off more sharply than the equity market. For example, UK 10-year Gilt yields surged 25bps, French yields were up 22bps and Italian yields rose 26bps in 5 days. US bonds also sold off, but the sell off was milder compared to Europe, and US 10-year Treasuries rose by 10bps. The risk is that equity traders align with bond markets and we get a deeper selloff across risky assets this week.

Will the deterioration in the special relationship weigh on the UK bond market risk premium?

It will be worth watching to see if the UK bond market continues to underperform this week. The deeper sell-off in UK Gilts was down to a recalibration of rate cut expectations, with only 0.3 rate cuts priced in by the interest rate swaps market by the end of last week, previously two cuts were expected. It may also have been down to deteriorating relations between the US and the UK, with the UK choosing not to enter the war with the US, signaling a major shift in the special relationship. This ignited the ire of President Trump, who lambasted PM Starmer at the weekend. According to reports, the UK is racing to improve diplomatic relations with the US, and if these work, could the risk premium attached to UK bonds decrease this week? This is something to watch.

Investors booking profits in UK stocks as uncertainty continues

The top performing stocks in the UK this week included BP, Shell and BAE Systems, in contrast, the worst performers were the materials companies and the miners, in particular. This suggests that the market is rotating out of formerly top performing sectors, and into oil and defense stocks as this conflict unfolds. The miners had a very strong start to the year, so investors may be booking in profits in this period of deep uncertainty.

Software stocks bounce back, as US investors look beyond Middle East conflict

In the US, the top performing sector on the S&P 500 last week was commodities. However, the biggest surprise was the bounce back in the application software sector, which rose more than 9%. This sector had sold off sharply earlier this year as fears about cheap AI plugins have battered the sector. The top performing tech stocks included AppLovin, Trade Desk, Expedia, and CrowdStrike. Interestingly, no big US oil company was a top 10 performer last week, suggesting that investors are still looking to the US for bargains, especially in the tech space which sold off heavily earlier in 2026. The rebound in software companies helped the US index to remain resilient to the conflict in the Middle East, and we expect this outperformance to continue.

In the FX space, the dollar is also worth watching this week. The dollar is poised to extend gains this week and is higher in early trading, which is weighing on risky assets. The liquidity of the dollar is driving high demand right now and it is likely to remain well supported as investors confront the possibility of a prolonged war in the Middle East that disrupts oil and gas supplies for months rather than weeks. While the dollar attracted inflows at the beginning of the week, it gave back gains on Friday, after a weaker than expected payrolls report for February. This boosted rate cut expectations in the US, and the Fed Fund Futures market is now pricing in 1.8 rate cuts this year, up from 1.5 on Thursday.

This suggests that fundamentals matter, especially in the US, which investors are treating as being less exposed to the conflict in the Middle East. Below, we look at two key fundamental events in the week ahead:

1, US CPI

The US inflation report for February will be released on Wednesday, and the market is expecting headline inflation to remain at 2.4% for last month, and core inflation to remain stable at 2.5%. This inflation report will seem very out of date after the rocketing energy and gas prices that we have seen in recent days, which is likely to put upward pressure on the March CPI reading. The Fed is in its quiet period ahead of its meeting on 18th March, so we will have to wait to hear how the Fed is treating this crisis. Is this something that the Fed and other global central banks will look through as a temporary increase, or will they see this as a real threat to price stability going forward?

The March meeting is one of Jerome Powell’s final meetings before he leaves the role of chair in May. However, he is likely to stay on as an FOMC member, so his opinion still counts. If he suggests that the Fed is scared by their view that inflation would prove temporary in 2021-2, before having to play catch up and rapidly raise interest rates, then we could see another rout in the bond market the coming weeks, as the Fed is the de-facto central bank to the world right now.

A weaker than expected reading for CPI could have a big impact on financial markets and it could weigh on the dollar and boost risk sentiment as it would suggest that US price growth is on a weaker trajectory, which could ease concerns about the current energy price spikes.

2, UK Monthly GDP

The monthly GDP reading for January in the UK will be worth noting after an extremely weak end to 2025. Q4 GDP rose by a worryingly low 0.1%. Before the conflict in the Middle East caused an energy price shock, the UK economy looked like it was potentially bouncing back. Stronger PMI growth gave hope that the private sector could finally shed concerns about the Budget that weighed heavily on growth in Q4. This could be reflected in January’s data, with a 0.2% monthly rate expected, and a 0.3% 3-month on month rate of growth expected by analysts.

While this is still a sluggish rate of growth, it would suggest that the UK economy did not slow further at the start of this year. It seems cruel that the ‘bounce’ in UK growth is likely to be wiped out by a surge in inflation caused by a damaging oil price spike. However, a stronger rate of growth than expected could provide some cushioning to the coming blow.

Overall, we think that this week’s UK economic data will have a marginal impact on UK asset prices, with news flow from the Middle East a much bigger driver for the second week in a row.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.