At the start of this week, European and US stock futures are eking out gains, the oil price is higher by more than 1% and Brent crude is just below $105 per barrel, as the conflict in the Middle East moves into its third week.

Diplomatic efforts to secure tanker safety through Strait of Hormuz

The same themes are likely to dominate this week, as geopolitics are the main driver of price action. There is still no sign of the war in Iran concluding. The latest development is from Tehran, who said that it was not looking for a ceasefire with the US. India hailed their diplomatic efforts at getting two gas tankers through the Strait of Hormuz, after directly negotiating with the Iranian regime. France and Italy are reportedly doing the same.

At this stage, the Strait of Hormuz remains closed, but this is a hopeful sign that Iran is open to diplomatic efforts to give oil tankers and cargo ships safe passage through the strait. Iran seems to be dealing on a ship-by-ship basis, so any downside in the oil price could be limited.

Oil: could a shipping crisis expand to a deeper supply crisis?

There are also other fears building that intense strikes at Iran’s key export hub on Kharg island risks retaliation against energy infrastructure in the Gulf state and across the region. So far, this crisis has mostly been a shipping crisis, however, it could expand to a broader supply crisis if key export hubs are hit by Iran. I that situation, it would lead to a much longer supply disruption. A shipping crisis has already caused the oil price to rise above $100 per barrel, the threat of a broad and prolonged supply disruption could see the oil price rise even higher.

As we start a new week, investors are faced with balancing hopes that ships can pass through the Strait of Hormuz, with fears that the crisis could get worse before it gets better. This is unlikely to ease risk aversion or upward pressure on the oil price in the coming days.

Global stock futures are slightly higher at the start of this week, and the oil price is comfortably above $100 per barrel. We think that market sentiment remains fragile, although a sharp decline in stocks last week could cause a slight easing of selling pressure as we move into the third week of the conflict.

Will US stocks continue to face deep selling pressure?

Last week, US stocks started to play catch up to their global peers and experienced a deeper selloff than European indices. The S&P 500 dipped by 1.6%, compared to a 0.23% decline in dollar terms for the FTSE 100. Although there are a plethora of oil producers in both the US and UK index, BP and Exxon have a sizeable proportion of their assets across the Gulf region that are stuck due to the closure of the Strait of Hormuz. This has been reflected in Exxon Mobil’s share price, which has only risen by 1.5% since the onset of this crisis, compared with a 12.5% rise in BP’s share price, which seems more immune to the supply crisis.

Although stock futures are higher at the start of this week, we are not convinced that dip buyers are here to stay. Short term signals look shaky. The percentage of companies on the S&P 500 making a 4-week high is 4%, compared to 22% make a new 4-week low. The Nasdaq is faring slightly better, 4% of companies are making new 4-week highs, compared with 15% making new 4-week lows. In Europe, defensive stocks and energy majors are providing some protection, 8% of the Eurostoxx 50 index made a new 4-week high last week, compared to 14% that made a 4-week low.

The dollar has a strong end to the week, and the dollar index rose above 100.00, the highest level of the year so far. The euro plunged 1.8% and the pound dipped 1.5% vs. the USD. The rapid repricing of the USD adds to global inflation pressures caused by the energy price spike. Global bonds had another bruising week, with US Treasuries leading the sell off. The 10-year US yield rose by 18bps, UK and Italian 10-year yields both rose 17bps, and French yields also rose 16bps.

Chart 1: The dollar inde, long term chart

Source: XTB

The sharp rise in bond yields is a difficult backdrop for some key market events in the coming days. Below we look at what to expect from the world’s major central banks and other data points that could move markets.

Events to watch this week

1, Central Bank Fest: Why Fed can be focused on growth, while inflaiton concerns will dominate in Europe

The conflict in the Middle East is front and centre as we wait for two thirds of the world’s major central banks to announce their latest policy decisions this week. Global investors want to hear what the world’s central bankers think about a potential inflation shock and a prolonged energy crisis and how this feeds into their future decision making, especially since most of the world’s central banks are now expected to delay cuts or even reverse course and start raising interest rates in the coming months.

The Federal Reserve, ECB, the Bank of England and the Bank of Japan are all expected to keep rates on hold this week, while the Reserve Bank of Australia is expected to be the first of the world’s major central banks to hike rates as a result of the conflict in the Middle East.

The plethora of central banks will be the main event this week. The Federal Reserve is the one to watch mid-week. There is now less than one cut priced in for the Fed this year. Although rate hikes are not imminent for any of the major central banks, policy makers are likely to stress the need to stay vigilant to see how the crisis impacts energy prices and inflation in the coming months.

The problem policy makers face is that they cannot open the Strait of Hormuz, instead, they have to react to events completely outside of their control. While the rapid repricing in bonds, and the sharp increase in yields around the world could limit some of the effect of rising prices, rising bond yields can also choke off growth. We expect the ECB, BOE, the BOJ and the Fed to sound serious about the threats to price stability and the global economy and strike a very cautious tone in their press conferences. Most central bankers have never dealt with an inflation shock like this in their career.

The risk is that central bankers, typically a conservative bunch, spook markets with bleak outlooks. The inflation shock of 2022, when global inflation rates were double figures, are still painful for central bankers who were accused of being behind the curve. Thus, central bankers will be sensitive to the mistakes of the past and may focus on inflation rather than growth, which could further weigh on risky assets like stocks and risk sentiment in the coming days.

However, the global economy is more vulnerable to an inflation shock right now as AI threats were already weighing on global labour markets and growth was slowing down before the conflict broke out. Thus, central bankers will need to tread a narrow path not to cause panic in the markets and crash global consumer confidence this week.

The market remains confident that the US will see lower rates this year, not least because the new Fed chair, picked by the President, could face political pressure to lower rates ahead of the midterms in November.

The picture is different in Europe, where inflation risks are in focus. The volatility in the interest rate futures market is unprecedented. The ECB is expected to increase rates twice this year, while in the UK, there has been a 180-degree pivot in rate expectations. Before the conflict and the spike in the oil price, there was an 80% chance of a rate cut at this week’s meeting, now there is a mere 1.2% chance of a cut,

Ultimately, the duration of this conflict will determine what central banks do next, and they are at the mercy of news flow as much as the rest of us.

2, UK labour market woes

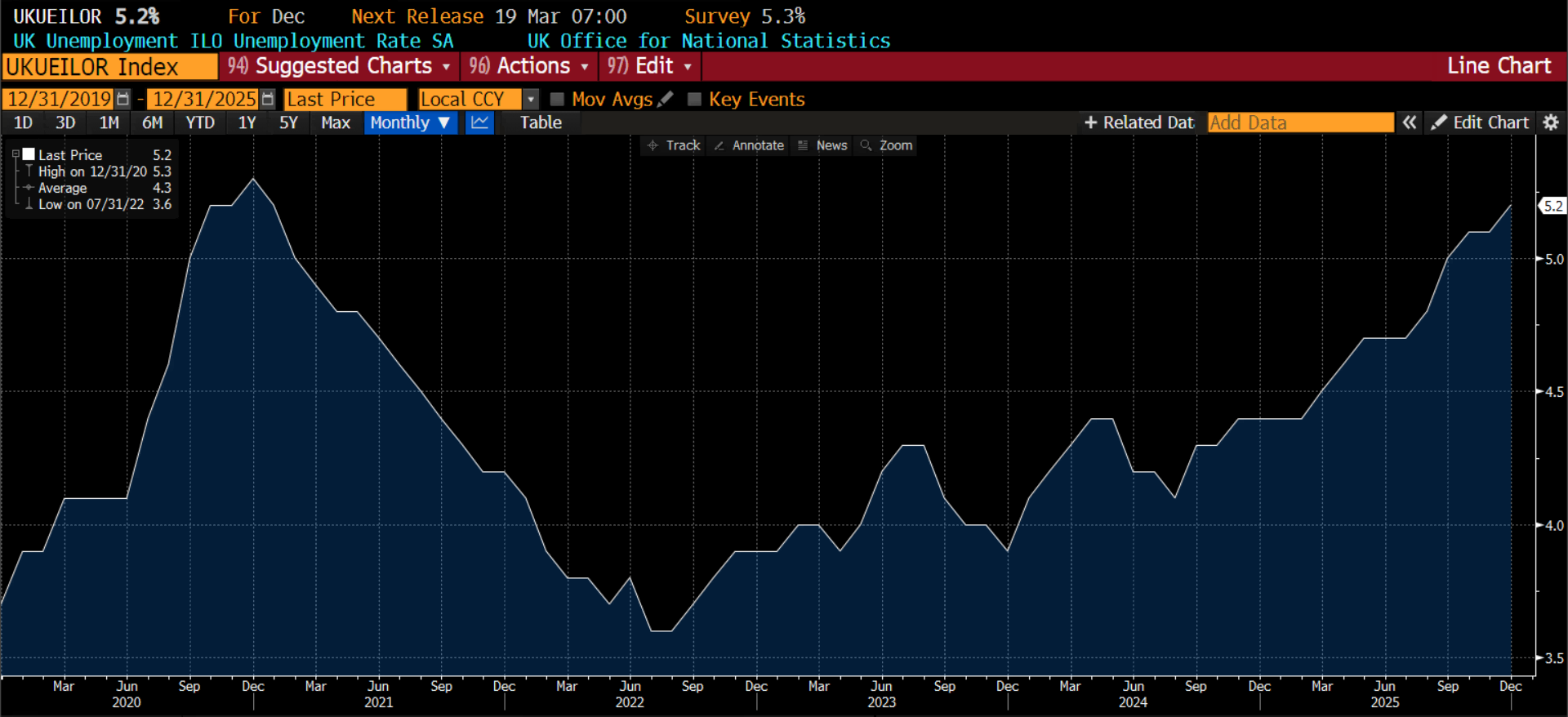

Another weak labour market report is expected for the UK. The unemployment rate is expected to have risen to 5.3% in January from 5.2%, a 5-year high, and jobs growth is expected to be negative. Weekly earnings are also expected to decline. The sharp rise in the unemployment rate is a headache for the BOE as it now faces an inflation shock. The unemployment rate is already expected to exceed the BOE’s February forecasts, and we think that the risks are to the downside for the UK’s beleaguered jobs market.

The pound is coming under pressure as the dollar resurgence continues, however, it was not the weakest performer in the G10 even though UK GDP at the start of the year showed no growth. Although inflation remains a key risk for the UK economy, the rising unemployment rate suggests that the UK economy is not operating at full employment, which may tilt the BOE away from rate hikes this year and towards remaining on hold instead. If the sharp rise in UK Gilt yields ease, then the pound may take a breather from its recent sell off.

Chart 2: The UK’s rising unemployment rate

Source: XTB and Bloomberg

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.