NFP – Non Farm Payrolls Preview

NFP preview: February jobs data expected to remain subdued

The February jobs report is scheduled for release this Friday; 6th March at 1330 GMT. Analysts are expecting NFP’s to increase by 60,000 last month, and the unemployment rate is expected to remain steady. Average hourly earnings are also expected to remain steady for last month at 3.7%, and private sector payrolls are expected to grow by 65k, down from 170k in January.

Lead indicators are positive for payrolls growth

Ahead of the payrolls report, the leading indicators for the US labour market point to a moderate improvement in the data. The ADP private sector payrolls report for February was higher than expected at 63k for February, the highest reading since November. The ISM employment index for both the manufacturing and services sectors also reported increases in hiring sentiment for the US private sector compared to January. The employment index for the service sector rose to 51.8, its highest reading for a year, which suggests that the US’s labour market could be gathering momentum as we move through the first quarter of the year.

Strikes and weather-related disruption could impact February jobs growth

There are some factors that are worth noting ahead of this week’s payrolls report. Firstly, there could be some weather-related disruption. A boost of 25,000 jobs could be down to delayed hiring because of severe winter storms across the US at the end of January. Added to this, there was also some notable strike action, approximately 5,000 workers were on strike last month, including 1000 Starbucks employees who have been on strike since November. This could weigh on jobs growth.

Potential market reactions

While the lead up to this payrolls report has been overshadowed by the conflict in the Middle East, if there is a big miss or a much larger than expected increase in payrolls for last month then we expect the markets to react. Treasuries tend to have the biggest reaction to payrolls per standard deviation of a beat or a miss. For example, if we see a weaker than expected payrolls, this could push Treasuries higher and yields lower. The opposite is also true, a stronger than expected report could weigh on Treasuries and push yields even higher across the curve. However, January’s stronger than expected payrolls report did not push yields higher and the dollar only had a mild reaction because the data was partly distorted by revisions for 2025. If the data is not seen as credible, the financial market reaction to payrolls can be tepid and short lived.

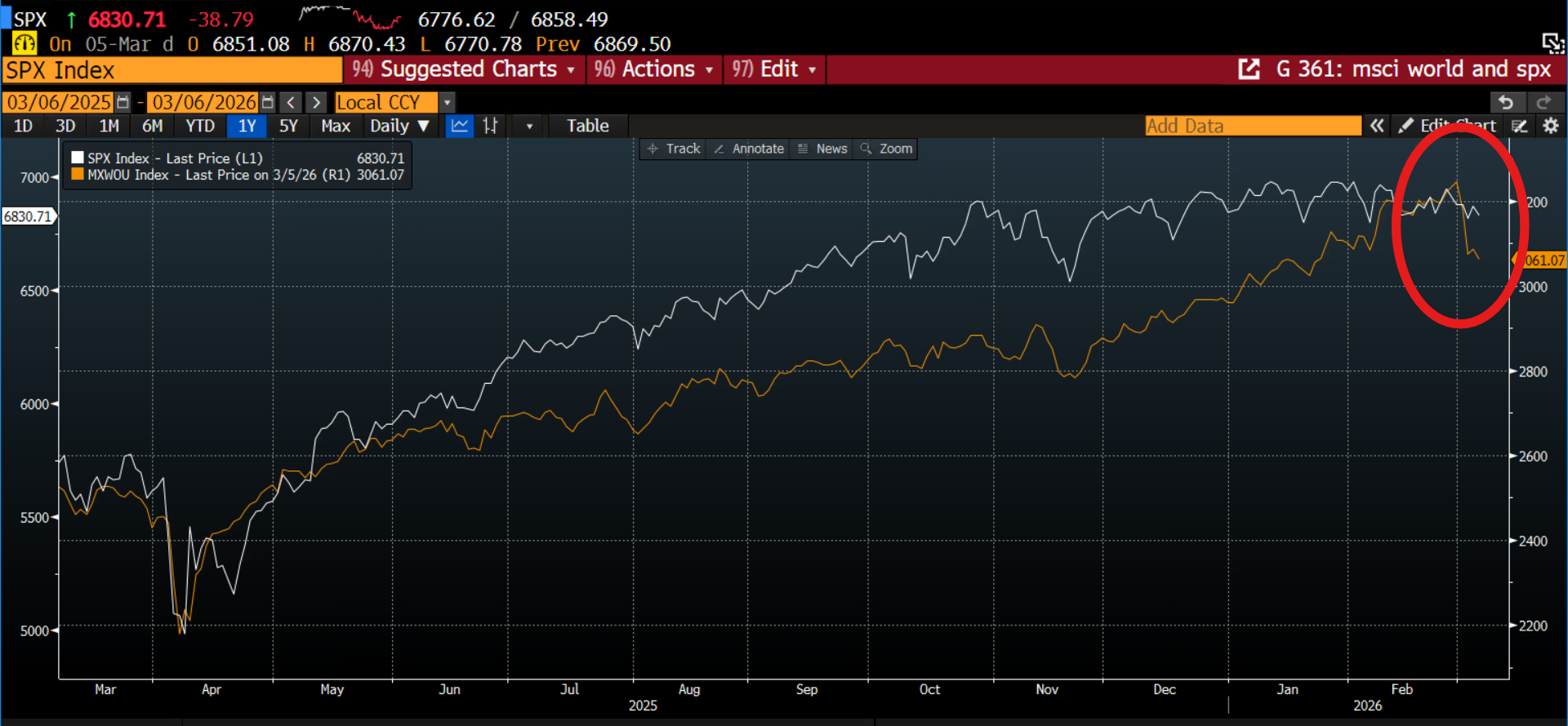

Ahead of this labour market report, risk sentiment has been shaky due to events in the Middle East. The potential for an oil price shock that damages the prospects of the global economy is weighing on stock markets, although the S&P 500 and the Nasdaq have been resilient compared to other global indices, as you can see below. The dollar is rallying into this report and is one of the strongest currencies in the G10 FX space behind the traditional commodity currencies like the Aussie dollar, the Norwegian krone and the Canadian dollar.

Rate cut expectations from the Federal Reserve have also been scaled back in recent days on the back of higher energy prices. There are now just over 1.5 cuts priced in for this year, down from over 2 before the outbreak of this crisis, which is helping to boost the dollar.

Market to return to fundamentals

Overall, the market has been focusing on geopolitics rather than fundamentals this week. Thus, a surprising NFP report could trigger a strong market reaction on Friday. A stronger reading may boost the dollar even further, and add upward pressure to Treasury yields, which are already biased to the upside due to fears about inflation caused by the recent rise in commodity prices. However, a weaker than expected payrolls reading could see the dollar struggle on Friday, and a further recalibration of Fed rate cut expectations, with a growing chance of a second rate cut at some stage later this year.

Chart 1: Dollar index after the January NFP report

Source XTB and Bloomberg

Chart 2: S&P 500 and MSCI ex US world index. US stock markets have proven more resilient than other global indices during the crisis in the Middle East.

Source: XTB and Bloomberg

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.