Micron Q2 2026 Preview – Memory Super-Cycle in Full Swing

Today, after the market closes, Micron Technology will release its results for the second quarter of fiscal year 2026. This event is closely watched not only by investors but also by the entire semiconductor industry and participants in the artificial intelligence sector. The Micron report has the potential to set the tone for the high-bandwidth memory segment, particularly in the context of rising demand for DRAM, NAND, and HBM in AI-powered data centers.

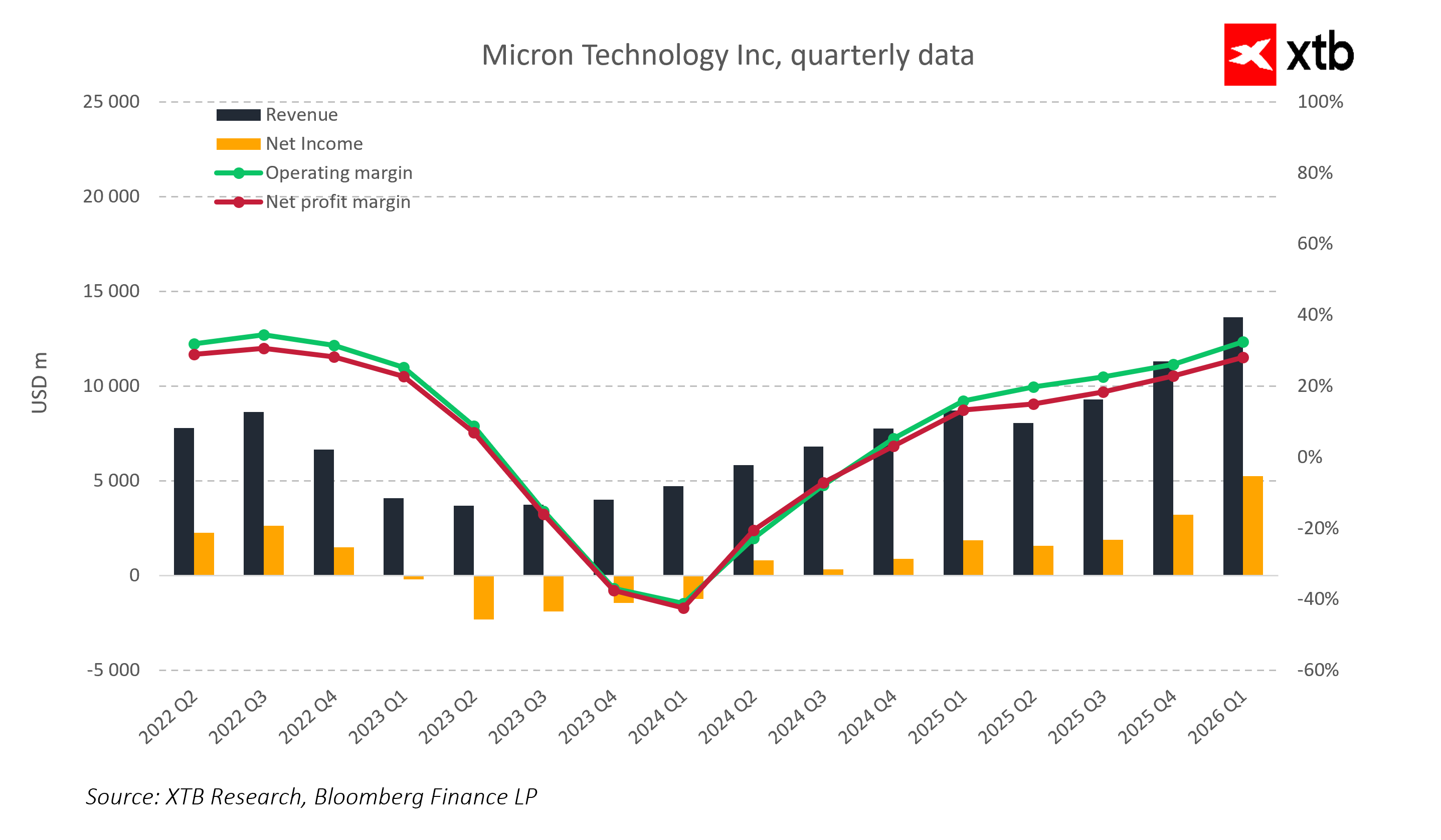

Expectations for Micron are extremely high. Analysts’ consensus forecasts revenue around 19.4 billion dollars, representing roughly 150 percent year-on-year growth, and earnings per share of approximately 8.7 USD. Gross margin is expected at about 69 percent, with an operating margin of 62 percent.

Market expectations

Q2 FY26 revenue: 19.4 billion USD (150% y/y)

EPS: 8.7 USD

Gross margin: 69%

Operating margin: 62%

Guidance for the next quarter

- Q3 FY26 revenue: approximately 23.8 billion USD, gross margin above 71%, EPS around 11 USD

Analysts anticipate a record-breaking beat of consensus estimates and a strong increase in memory prices driven by AI-related demand. Projections for Q3 also reflect revenue of 23.8 billion USD, gross margin above 71 percent, and EPS around 11 USD. Such high figures highlight the exceptional nature of the current memory supercycle, fueled primarily by AI investments and constrained supply.

Market position and significance for the semiconductor sector

In 2026, Micron shares have already risen by around 60 percent, following an almost threefold increase in 2025. Many competitors in the semiconductor industry posted only moderate gains by comparison. Micron’s market capitalization has exceeded 500 billion dollars, surpassing companies such as Oracle and placing the firm among the world’s leading memory manufacturers.

Rising prices and strong demand for data center memory allow Micron to maintain control over revenues and margins. Its strong position in the high-bandwidth memory segment gives the company leverage in negotiations with hyperscalers and stabilizes revenue from AI server applications.

Major market players, including Amazon, Google, Microsoft, and Meta, are increasing memory investments for AI workloads and next-generation GPUs. Consequently, much of Micron’s revenue growth is driven by stable corporate and server demand.

HBM and DRAM as the foundation of the supercycle

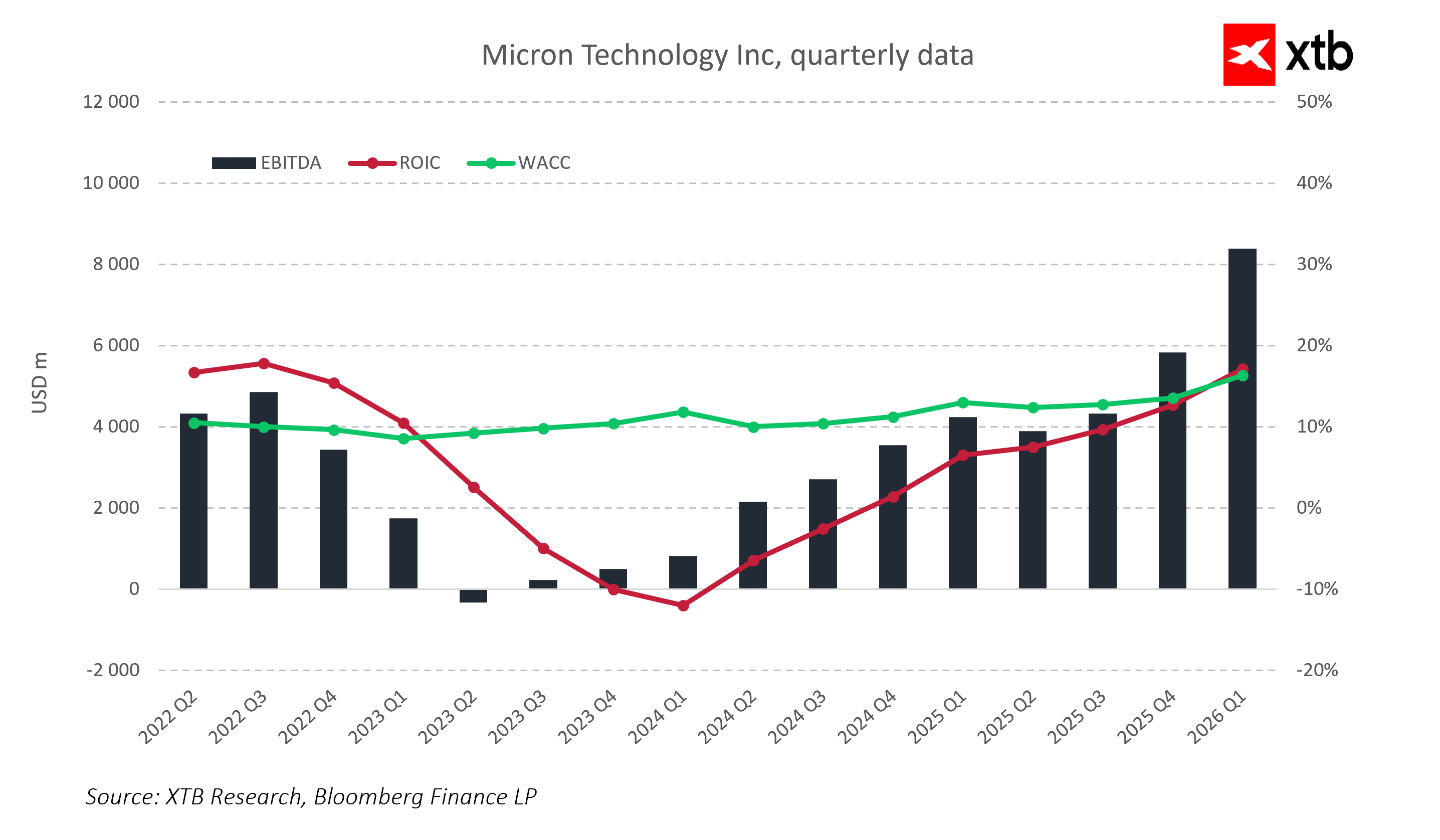

HBM4e memory has become Micron’s core product. All production capacity for 2026 has already been contracted, with new clients joining waiting lists. Limited supply combined with growing demand keeps prices exceptionally high, and the backlog serves as a key stabilizing factor for revenue in upcoming quarters.

The DRAM segment continues to account for a significant portion of revenues. DDR5 and DDR5X server deployments are growing 20 to 25 percent year-on-year, driven by new data center construction and modernization of existing facilities. Supply discipline among the three largest manufacturers – Micron, Samsung, and SK Hynix – maintains high prices and supports gross margins exceeding 50 percent.

Although the NAND segment is regaining momentum due to enterprise SSD demand in data centers, the consumer market remains weaker. Micron emphasizes high-margin industrial applications, which helps stabilize revenues despite slower PC and smartphone markets.

Production investments and the 2027 plan

Micron continues to expand its factories in New York and has opened a facility in India, which will increase production capacity in the medium term. New HBM production lines are expected to reach full operational capacity only in 2027. In 2026, the company is fully utilizing existing capacity, allowing it to maintain high memory prices and strong margins.

The market will closely monitor how new factory investments translate into increased supply and price stabilization. Full utilization of existing plants, along with the HBM and DRAM backlog, is critical for maintaining competitive advantage and profitability.

Hyperscaler demand and global factors

Demand from leading players such as Amazon, Google, and Microsoft drives HBM and DRAM sales in data centers. GPU and memory orders are closely tied to hyperscaler AI investment plans. Any slowdown in CapEx in this segment could affect Micron’s demand and margins.

The memory industry also remains sensitive to geopolitical developments. Export restrictions, government subsidies, and CHIPS Act policies influence production allocation and factory capacity. Despite these risks, Micron benefits from tax incentives and local government support, reducing cost pressure and enabling ambitious investment plans.

Market reaction scenarios

The market’s response will depend not only on Q2 results but also on management commentary regarding upcoming quarters.

In a positive scenario, a strong beat in revenue and earnings per share combined with sustained high memory prices could drive Micron’s share price higher and generate positive sentiment across the semiconductor sector.

A neutral scenario, with results in line with expectations and stable guidance, will likely lead to a moderate market reaction and be interpreted as confirmation of the ongoing growth trajectory.

A negative scenario, including revenue or EPS disappointment, slower HBM sales, and margin pressure, could trigger sector-wide declines and dampen enthusiasm for AI memory.

Ultimately, today’s report will serve as a test of the durability of the AI boom and memory demand in data centers. The results will indicate whether record Q2 performance marks the beginning of a long-term trend, with guidance for upcoming quarters being crucial to assessing the company’s growth potential and broader semiconductor market sentiment.

Key takeaways

- Q2 revenue is estimated at approximately 19.4 billion USD, EPS around 8.7 USD, gross margin at 69 percent

- HBM4e and high-bandwidth DRAM are the primary drivers of revenue growth and profitability improvement

- Traditional DRAM and NAND remain revenue pillars due to growing data center demand and supply discipline

- Investments in new factories in the US and India will increase production capacity in the coming years and may stabilize prices

- Hyperscaler demand from companies like Amazon, Google, and Microsoft fuels Micron’s revenue and margin growth

- Q2 results and guidance for upcoming quarters are critical to evaluating the sustainability of AI-driven memory demand

- Publication of results may impact the entire semiconductor sector and investor decisions regarding tech ETFs and competitor stocks

- Full utilization of existing production capacity and HBM and DRAM backlog are key for maintaining technological advantage and profitability

Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.