Fed Preview: markets gain confidence heading into Fed meeting

News flow continues to dominate right now, both on the upside and the downside. The stock rally is extending into a third day, and the oil price is lower after Iraq signed a deal with Turkey to export oil without using the Strait of Hormuz. As oil producers adapt to the situation in the Middle East, the oil price will also adjust, and the Brent crude price is down 1.6 % on this news.

Corporate news jostles with Middle East headlines

Stock market futures are a sea of green across the US and Europe this morning, as risk is rallying into tonight’s Fed meeting. Although the Middle East conflict continues to dominate, corporate news is also grabbing the headlines. Nvidia’s CEO projected that the company would generate $1 trillion in chip revenue through to 2027, and that it will use more of its free cash flow on share buybacks and investor returns in the second half of this year. Unilever will also be in focus today after it said that it is considering spinning off its food assets. As we move to the middle of the week, central banks will dominate.

Central banks to dominate

Two thirds of the world’s major central banks will announce interest rate decisions this week. While Australia’s RBA has bitten the bullet and raised interest rates on Tuesday, the highlight is undoubtedly the Federal Reserve meeting later this evening.

Which Fed will we get?

The Fed is expected to remain on hold, but it will be the tone of the Fed statement and Jerome Powell’s press conference that will determine the market reaction. Too concerned about inflation pressures from the energy price spike and market sentiment could get hit, disrupting the recent recovery in stocks and bonds, not concerned enough about the inflation and the market could start questioning the Fed’s credibility. Jerome Powell and co have a narrow path to walk later on Wednesday.

Even before the outbreak of war, there were signs that US inflation pressures were building and some Fed members wanted the Fed to shift away from dovish language to a more neutral stance around the future direction of monetary policy. We believe that the Fed is likely to make this shift, with this evening’s statement expected to show that the Fed will remain on hold for the long term.

Fed expected to be in wait and see mode, regardless of what the doves think

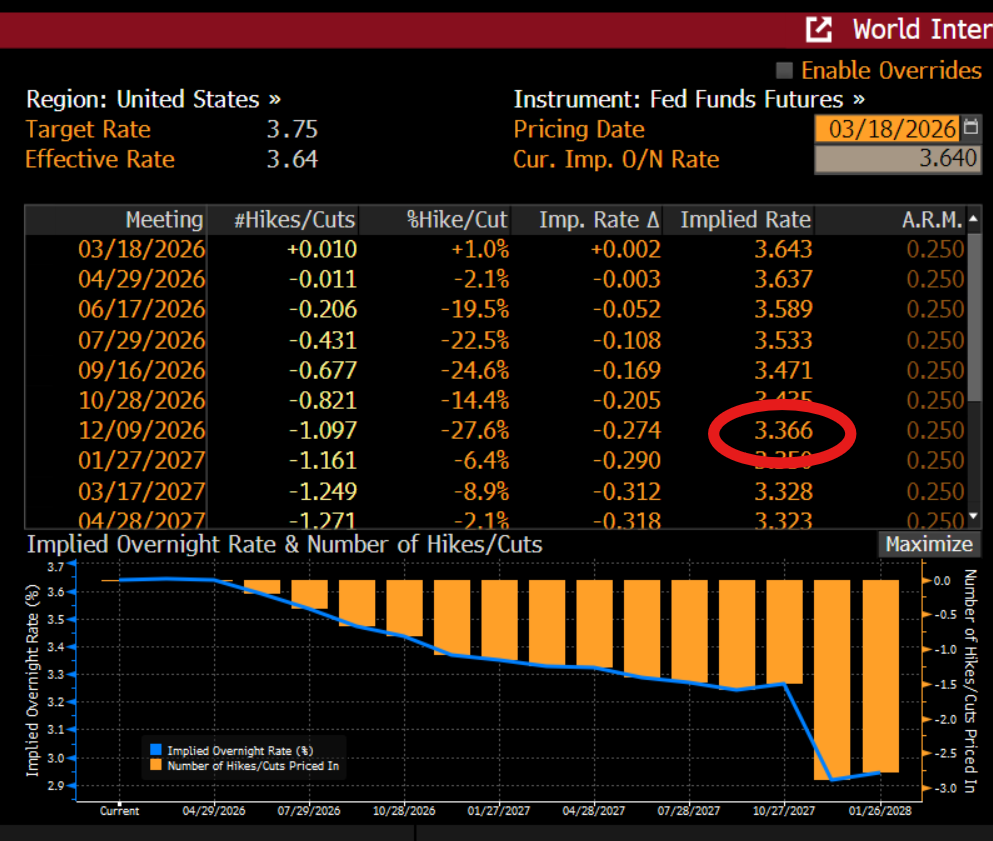

The Fed Fund Futures market is now expecting just one cut from the FOMC this year, prior to the outbreak of war two cuts were priced in. A rate cut is not expected until the second half of the year, around September. While some Fed members are concerned about the inflation outlook, others are also worried about the labour market after a weak February NFP market report.

Due to this, we do not expect a unanimous vote in favour of remaining on hold. Instead, we could see multiple dissenters, including Stephen Miran, the noted dove, Christopher Waller, and the vice chair Michelle Bowman.

This is unlikely to shift the dial for the Fed. Ultimately, the bulk of members are expected to stress the volatile and uncertain situation that the world faces, and this supports remaining on hold to fight both inflation risks and risks to growth.

Are we returning to 2022?

The tone will also be important to determine the market reaction to this meeting. Will Jerome Powell sound concerned about a return to 2022, or will he herald the energy price spike a temporary blip in an otherwise disinflationary period for the global economy?

There is some cautious positioning as we lead up to tonight’s Fed meeting. Stocks have posted gains after a rough two weeks, although sentiment remains fragile. Bonds are also in recovery mode and Treasuries have fallen about 8bps so far this week. We believe that the Treasury market will take directions from the Fed before making its next move.

Dot Plot: the Fed buys itself time

The updated Dot Plot will also be worth watching closely, we expect that the median projection for rate cuts in 2026 will be pushed out until much later this year to buy the Fed time in this unprecedented global environment. If the Fed accompanies this with a caveat that all projections are subject to change due to excess uncertainty, the market reaction may be mild.

Chart 1: Federal Funds Futures expectations for US interest rates

Source: XTB and Bloomberg

What now for the dollar?

The dollar is coming under pressure this week, and the dollar index is back below 100, however, the longer-term trend remains supportive. The greenback is still one of the top performing currencies in the G10 FX space so far this month, with the euro, the Swedish krone and the New Zealand dollar suffering the largest declines.

The longer-term outlook remains supportive for further dollar gains, although the short-term picture is more nuanced. Demand for the dollar remains strong and we do not see this ending until there is a clearer picture of how the conflict in the Middle East will end.

Chart 2: The dollar index remains well supported on the downside

Source: XTB

The confirmation of the next Fed chair…

There is another dimension to this meeting, who will replace Jerome Powell as chair? Kevin Warsh is Trump’s pick; however, his nomination has been held up, and he may not be able to take over on May 15th.

Republican Senator Thom Tillis has vowed to block Warsh’s nomination until the Department of Justice’s criminal investigation into the current Fed chair Jerome Powell is resolved. This risks delaying Warsh’s nomination. The President could nominate a temporary Fed chair as we wait for Warsh to get Senate approval. Stephen Miren is the most likely candidate. He is also a noted dove, and he may lead a charge to cut interest rates later this year. Thus, regardless of the global macro environment, big changes are coming down the line for the Fed.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.