Oil

- Crude oil prices commenced the week on a downward trajectory, pressured by a broader sell-off in the metals market and diminishing risk premiums associated with the US-Iran standoff.

- Reports suggest Iran is signaling a readiness to negotiate a new nuclear accord. This shift appears driven by fears of US-led regime change efforts, underscored by the significant buildup of American military assets in the Middle East, including the USS Abraham Lincoln carrier strike group and advanced aircraft.

- A high-stakes meeting is scheduled for Friday between US envoy Steven Witkoff and Iranian Foreign Minister Abbas Araghchi.

- The US and India have formalised a landmark trade agreement. Under the terms, Washington will remove the 25% additional tariff on Indian goods and reduce the standard 25% rate to 18%. In exchange, New Delhi will open its markets to American products and has committed to halting purchases of Russian crude, redirecting its demand toward US supply.

- It is worth noting that the recent surge in Indian demand was driven not only by rapid economic expansion but also by the lucrative re-export of refined products. India had been processing discounted Russian crude and selling refined derivatives to the global market at standard prices, capturing significant margins.

- Russia anticipates a demand recovery in the spring and summer, maintaining that the oil market remains balanced. This outlook is expected to inform OPEC+ production decisions effective from April.

- Alexander Novak of the Russian Energy Ministry noted that, despite India’s declarations regarding a halt to Russian imports, the physical trade situation remains unchanged for now.

- Preliminary data indicates that Venezuelan exports nearly doubled in January to 800,000 barrels per day (bpd), up from 498,000 bpd in December. However, this surge in exports may not reflect a recovery in production, as Venezuela has faced severe logistical bottlenecks in recent months, leading to high inventory accumulation in onshore storage and floating tankers.

- Russia continues its intensive strikes against Ukraine, maintaining that core territorial issues remain unresolved. Nevertheless, the Ukrainian conflict currently appears to sit outside Donald Trump’s immediate sphere of interest.

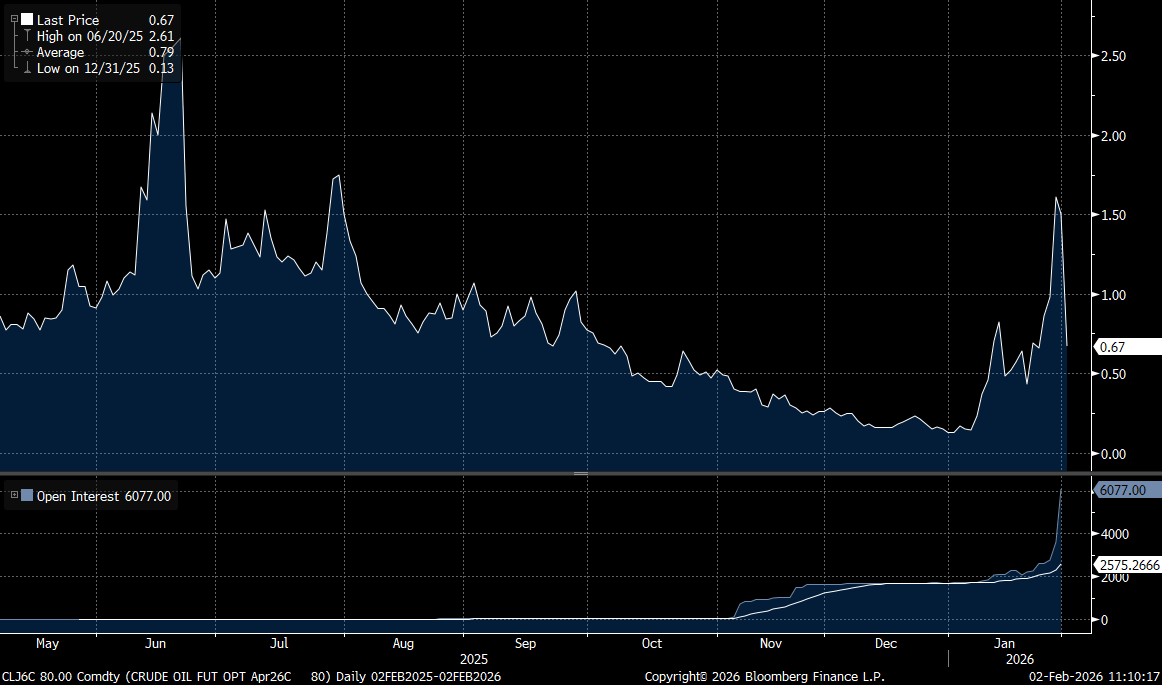

Call option prices for April WTI with an $80 strike have fallen sharply compared to last Friday’s close. Source: Bloomberg Finance LP

Call option prices for April WTI with an $80 strike have fallen sharply compared to last Friday’s close. Source: Bloomberg Finance LP

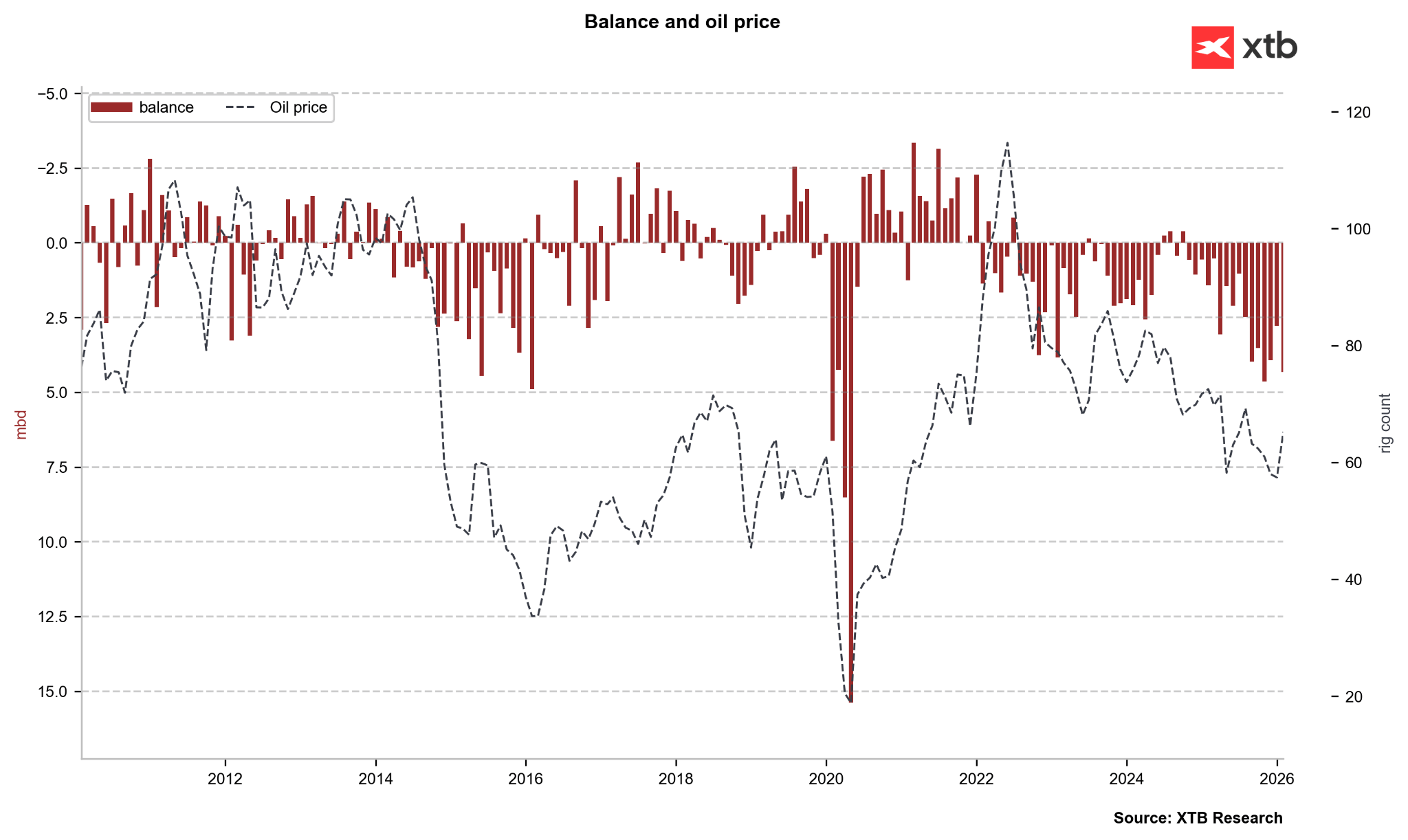

The oil market is experiencing a massive oversupply that is projected to persist throughout 2026, notwithstanding geopolitical volatility in Venezuela, Iran, and Russia. Source: Bloomberg Finance LP, XTB

The oil market is experiencing a massive oversupply that is projected to persist throughout 2026, notwithstanding geopolitical volatility in Venezuela, Iran, and Russia. Source: Bloomberg Finance LP, XTB

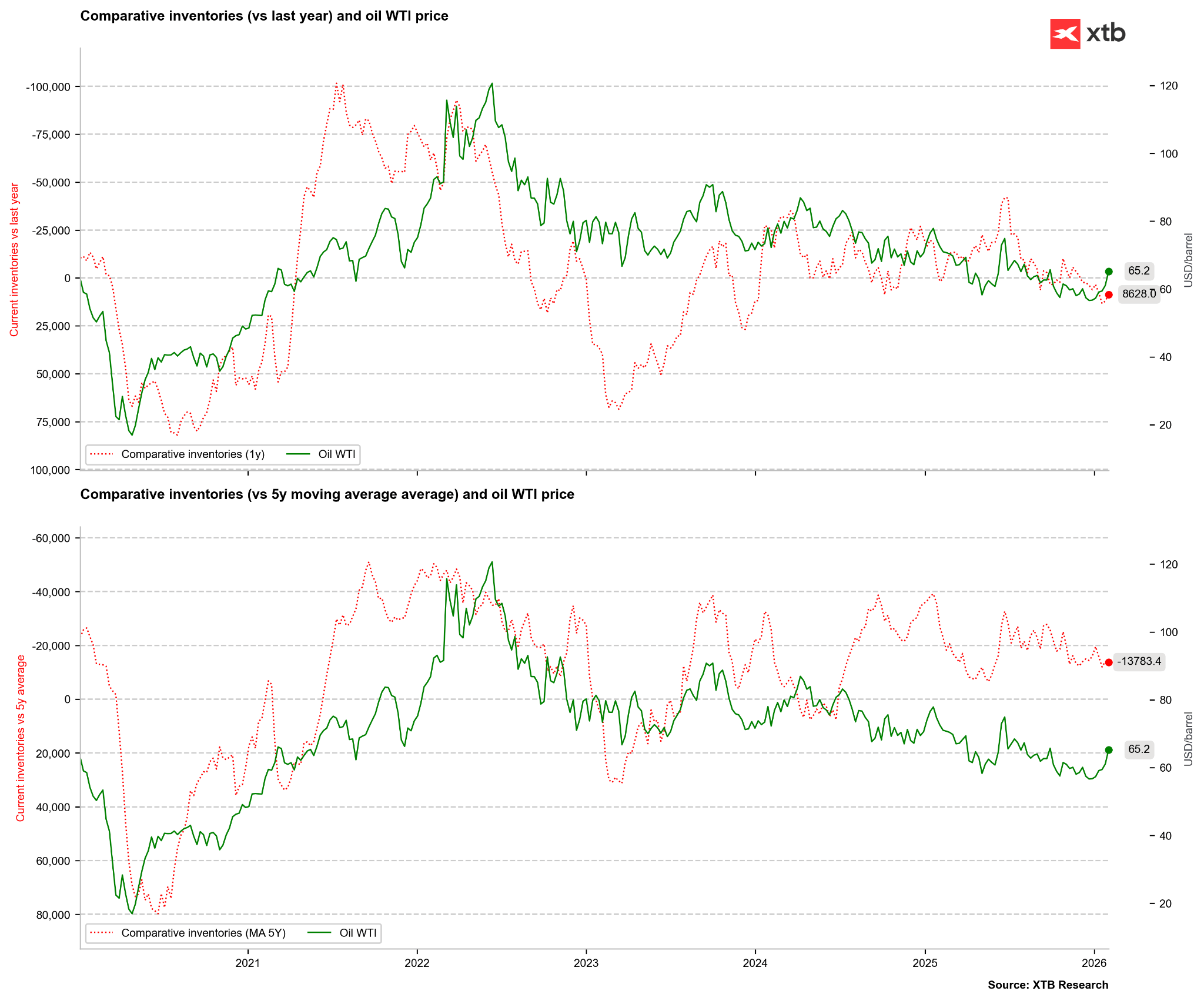

US crude inventories are higher than a year ago but remain below the five-year average. However, the gap between current stocks and the seasonal mean is narrowing. Source: Bloomberg Finance LP, XTB

US crude inventories are higher than a year ago but remain below the five-year average. However, the gap between current stocks and the seasonal mean is narrowing. Source: Bloomberg Finance LP, XTB

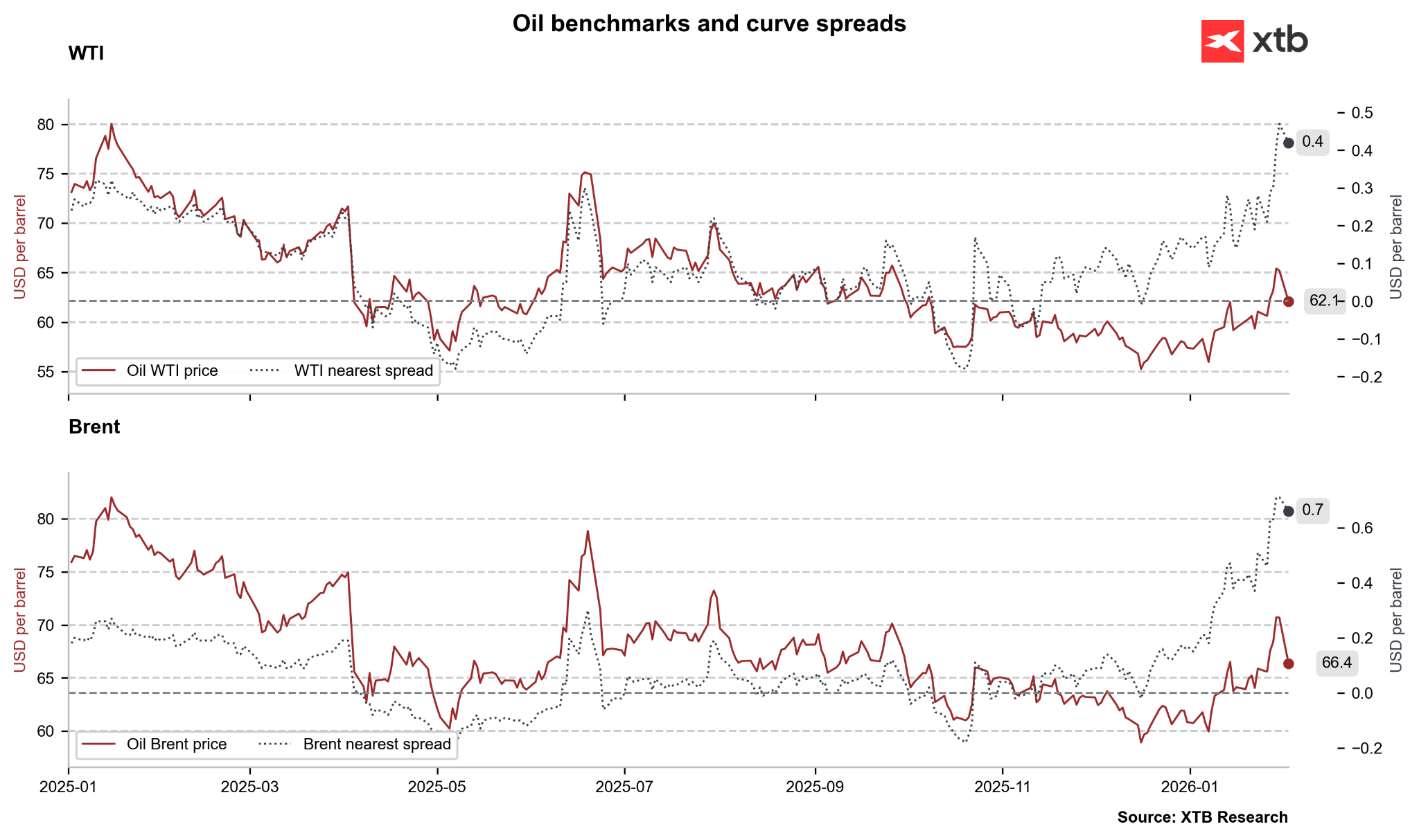

The market continues to exhibit significant backwardation, both in front-month contracts and across the forward curve. Source: Bloomberg Finance LP, XTB

The market continues to exhibit significant backwardation, both in front-month contracts and across the forward curve. Source: Bloomberg Finance LP, XTB

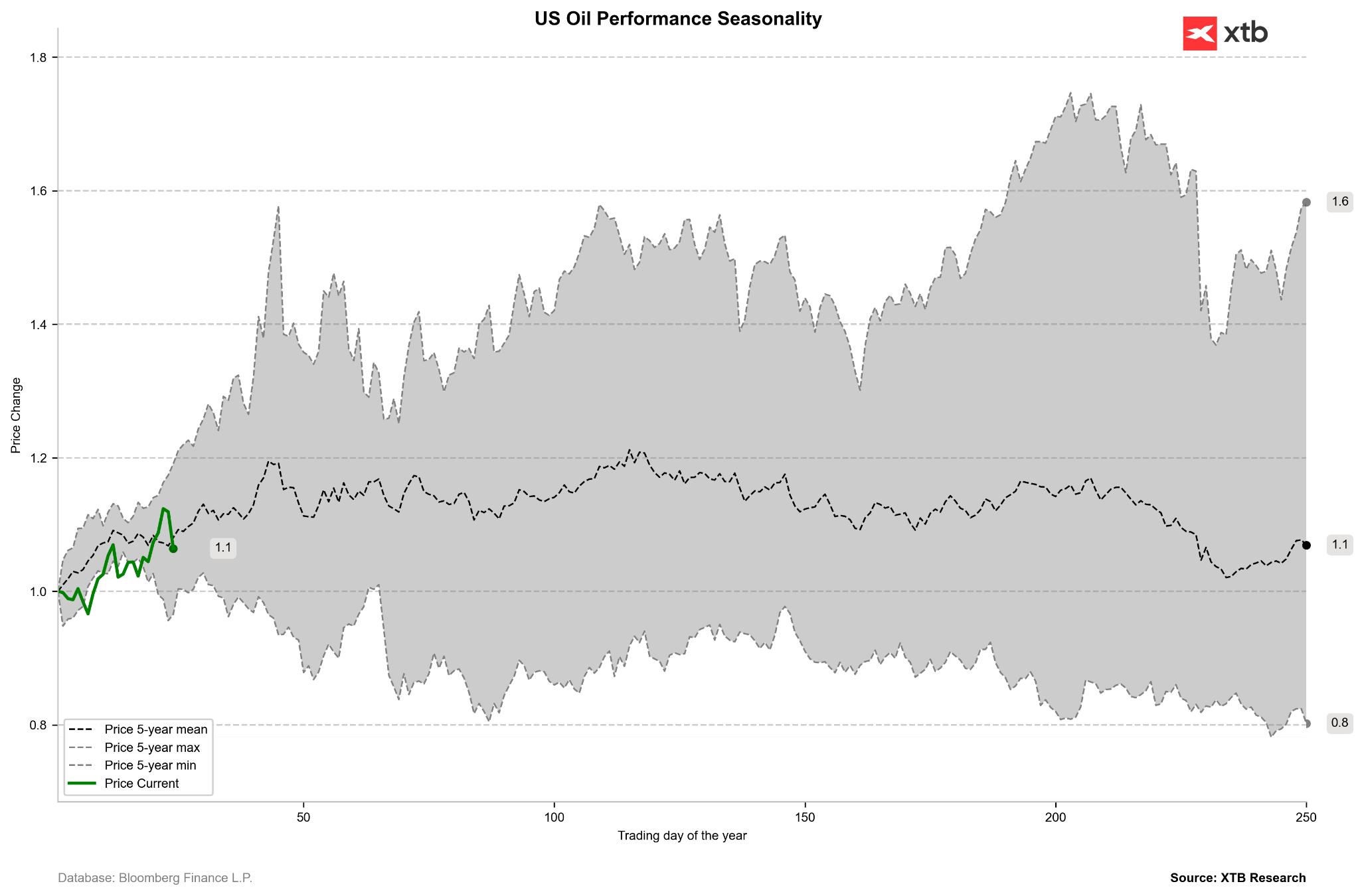

Oil market seasonality suggests that the first two months of the year typically face upward pressure, followed by a period of consolidation in March and April. Source: Bloomberg Finance LP, XTB

Oil market seasonality suggests that the first two months of the year typically face upward pressure, followed by a period of consolidation in March and April. Source: Bloomberg Finance LP, XTB

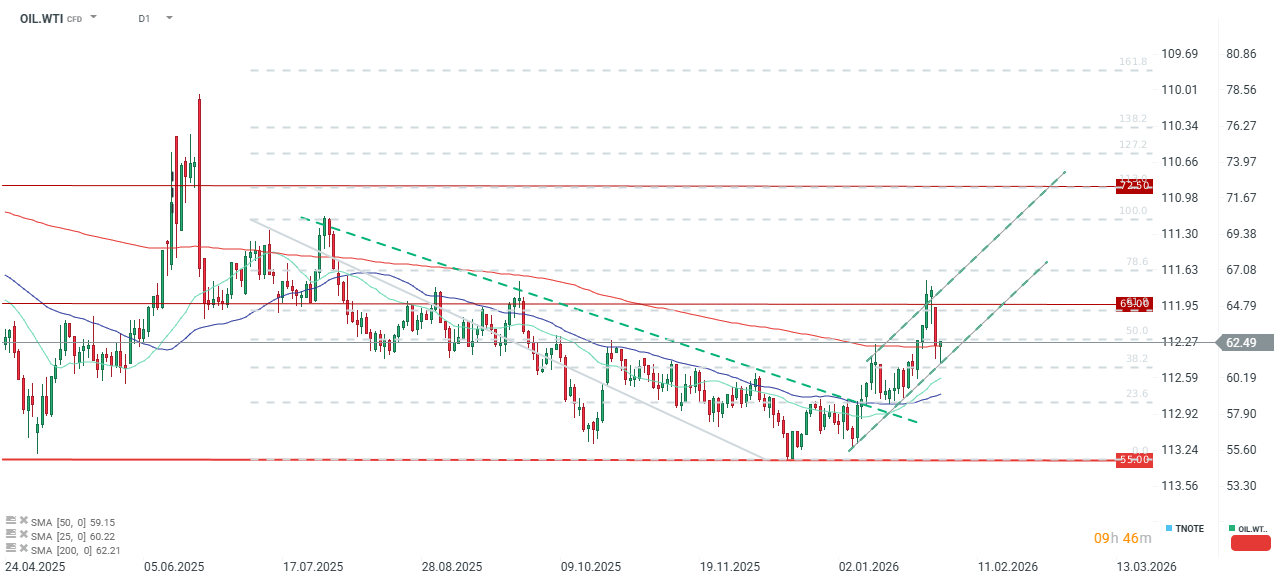

Crude prices are attempting a recovery following a highly negative opening in early February. The lower boundary of the ascending trend channel remains intact. Source: xStation5

Crude prices are attempting a recovery following a highly negative opening in early February. The lower boundary of the ascending trend channel remains intact. Source: xStation5

Silver

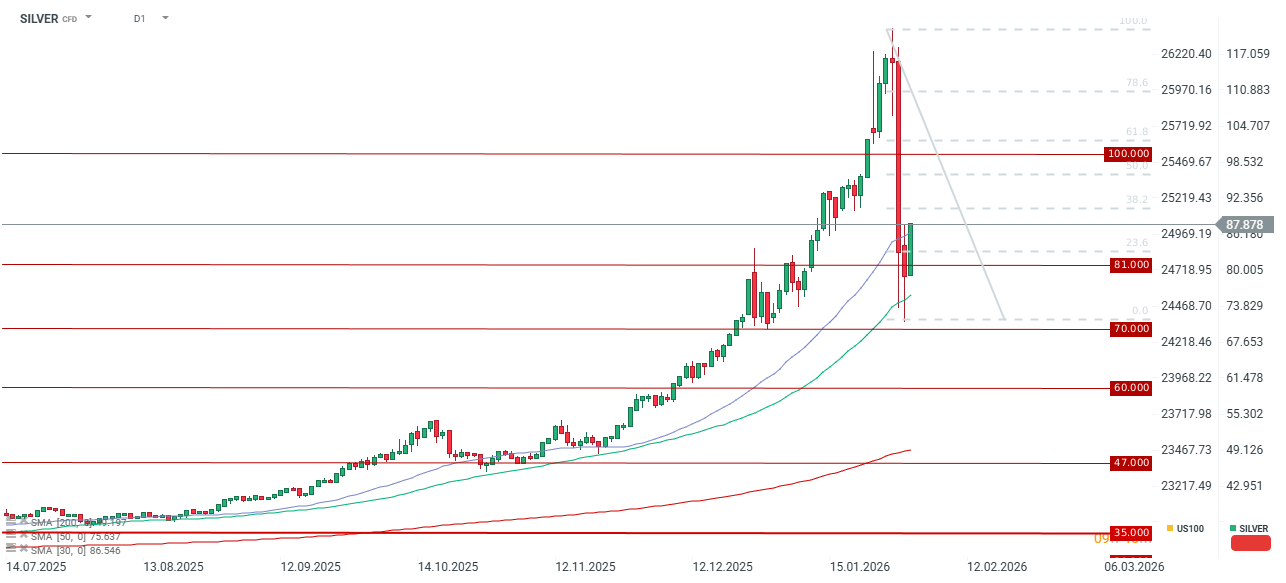

- Silver experienced what was likely its largest single-day retracement during the final session of January last Friday. Prices plunged by approximately 28%, with intraday losses reaching as high as 36%.

- The metal attempted a rebound during Monday’s opening after initial losses deepened and tested the $70 per ounce level. Prices reacted for a second time to the 50-period moving average; following a bounce to $86 per ounce, the 25-day SMA is now being tested.

- The silver market was extremely overbought from an options perspective, with Risk-Reversal indicators hitting levels not seen since 2020.

- Concurrently, silver lease rates fell toward zero. The 12-month silver swap rates rebounded significantly to approximately -0.5%.

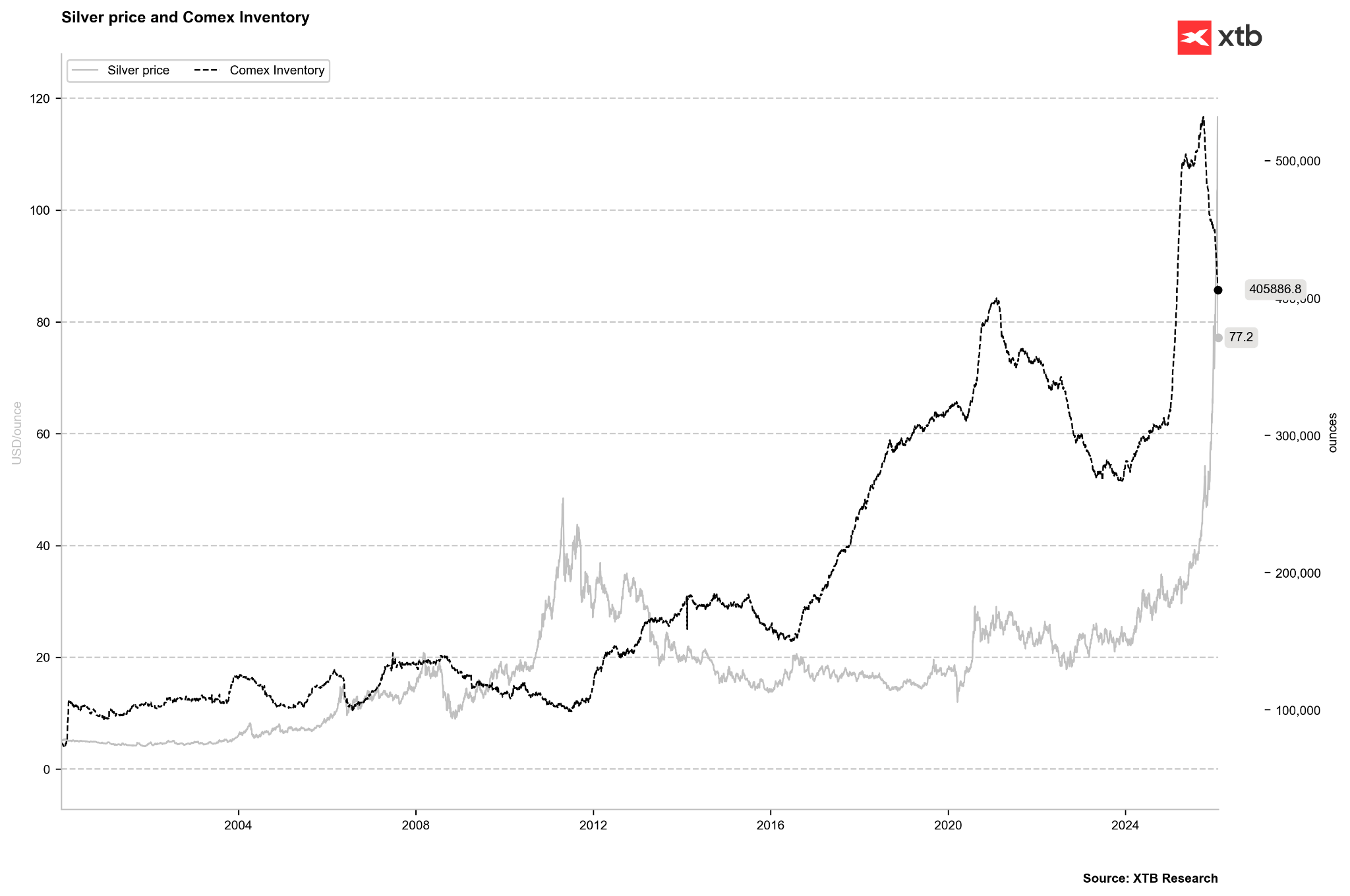

- COMEX inventories continue to decline, currently hovering near the 400 million ounce mark. Only one-quarter of these are “registered” stocks available for delivery; the remainder consists of “eligible” stocks held by institutions with no immediate intention to deliver.

- A more pressing structural issue is the persistent high price premium in China, where the market is in backwardation. Chinese investors continue to show a strong preference for physical delivery.

- It is important to remember that the Shanghai Futures Exchange imposes a 17% daily price limit, which constrains price movements relative to the volatility seen on COMEX.

- Recently, the UBS SDIC Silver Futures Fund LOF—popular among Chinese retail investors—underwent a revaluation. Intense demand for this fund had previously pushed its premium over Net Asset Value (NAV) as high as 100%.

- We have also observed a marked decrease in silver held by ETFs, primarily in the US. While some attribute this to profit-taking, speculators suggest that closing ETF positions may be a strategy to withdraw physical supply from the exchange. An investor selling ETFs can take a long position in futures to take physical delivery. A recent spike in COMEX delivery notices coincided with the decline in ETF holdings.

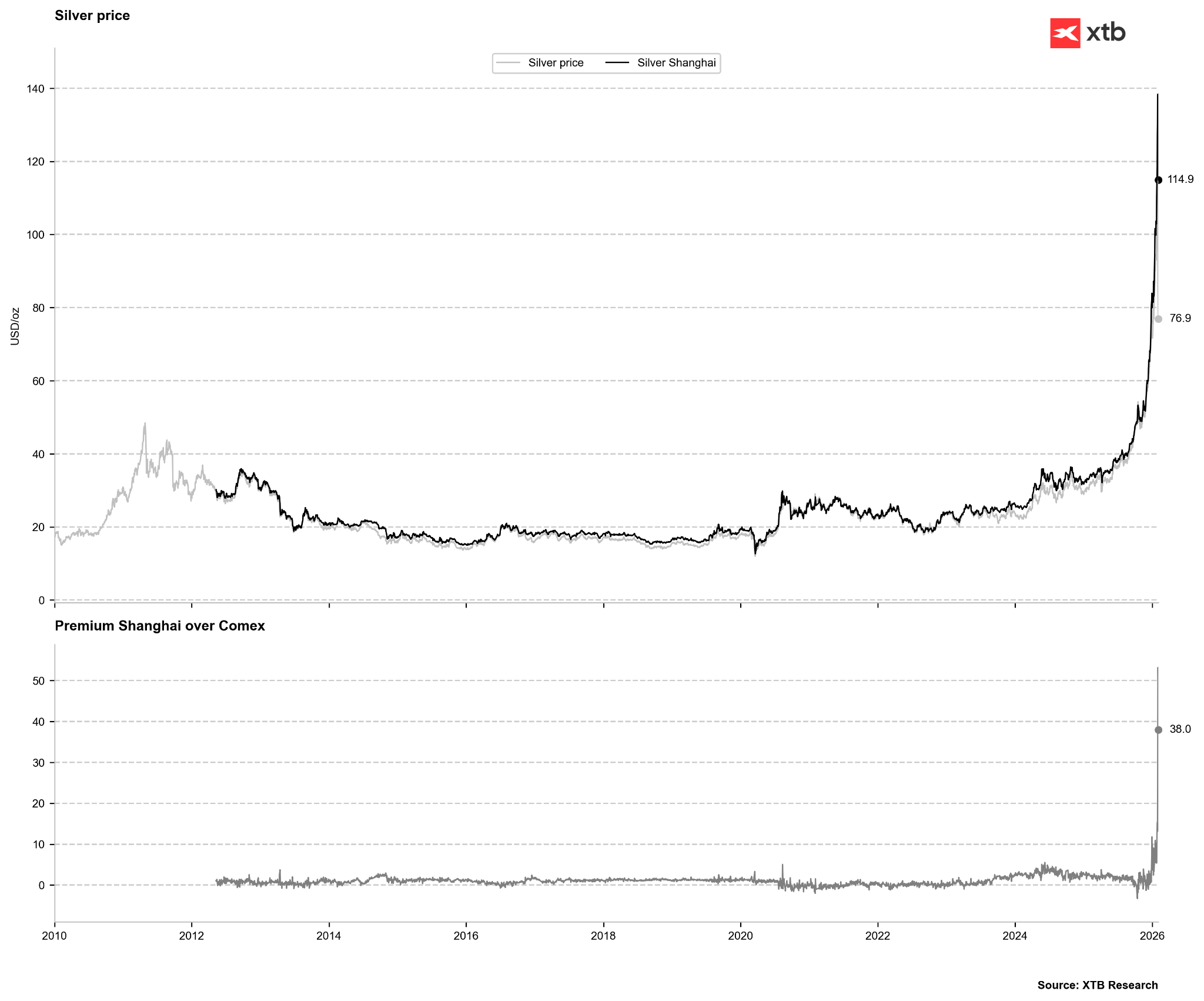

The price premium in China remains extremely large relative to the US. Source: Bloomberg Finance LP, XTB

The price premium in China remains extremely large relative to the US. Source: Bloomberg Finance LP, XTB

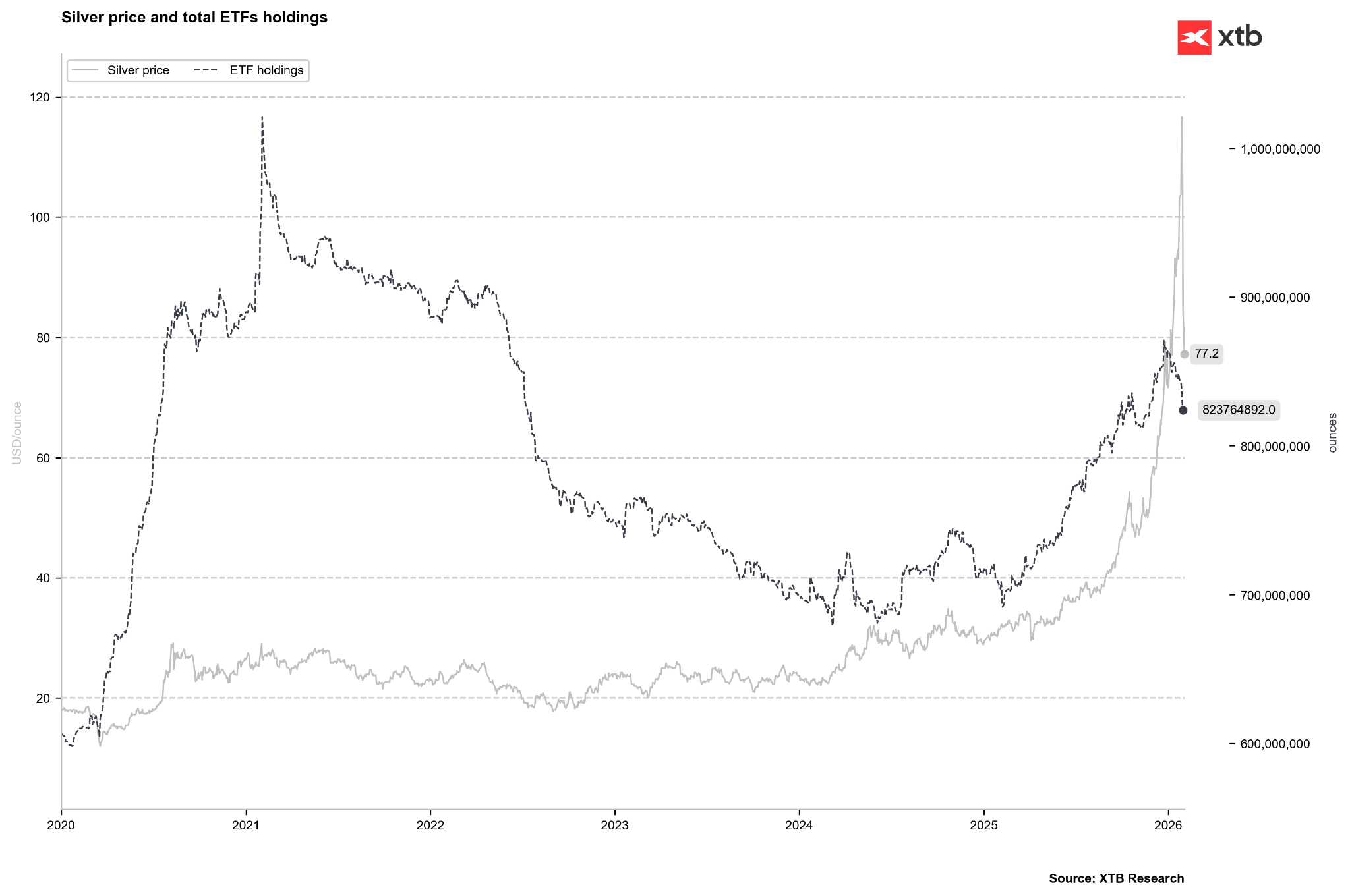

Silver holdings in ETFs have been falling sharply since late December, a trend that coincides with declining COMEX inventories. Source: Bloomberg Finance LP, XTB

Silver holdings in ETFs have been falling sharply since late December, a trend that coincides with declining COMEX inventories. Source: Bloomberg Finance LP, XTB

COMEX inventories continue their steep decline, though historically, stock levels remain elevated. Source: Bloomberg Finance LP, XTB

COMEX inventories continue their steep decline, though historically, stock levels remain elevated. Source: Bloomberg Finance LP, XTB

A price close above $85 may suggest a bullish engulfing pattern on the chart. Key resistance lies near $100, between the 50% and 61.8% retracement of the latest downward wave. The price rebounded from the zone between the 25 and 50 SMAs, mirroring the October correction, though the current percentage move is more than twice as large. Source: xStation5

A price close above $85 may suggest a bullish engulfing pattern on the chart. Key resistance lies near $100, between the 50% and 61.8% retracement of the latest downward wave. The price rebounded from the zone between the 25 and 50 SMAs, mirroring the October correction, though the current percentage move is more than twice as large. Source: xStation5

Natural Gas

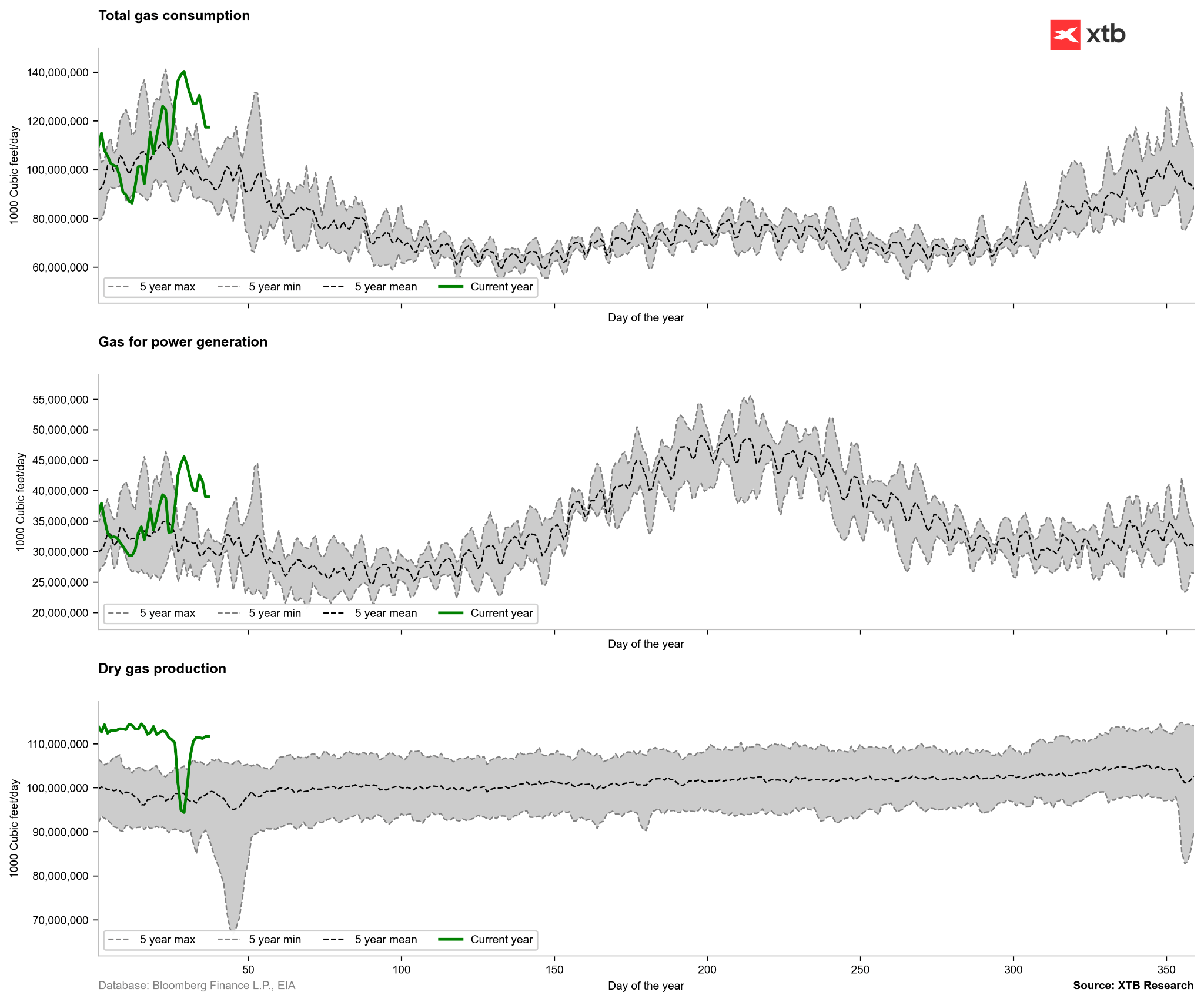

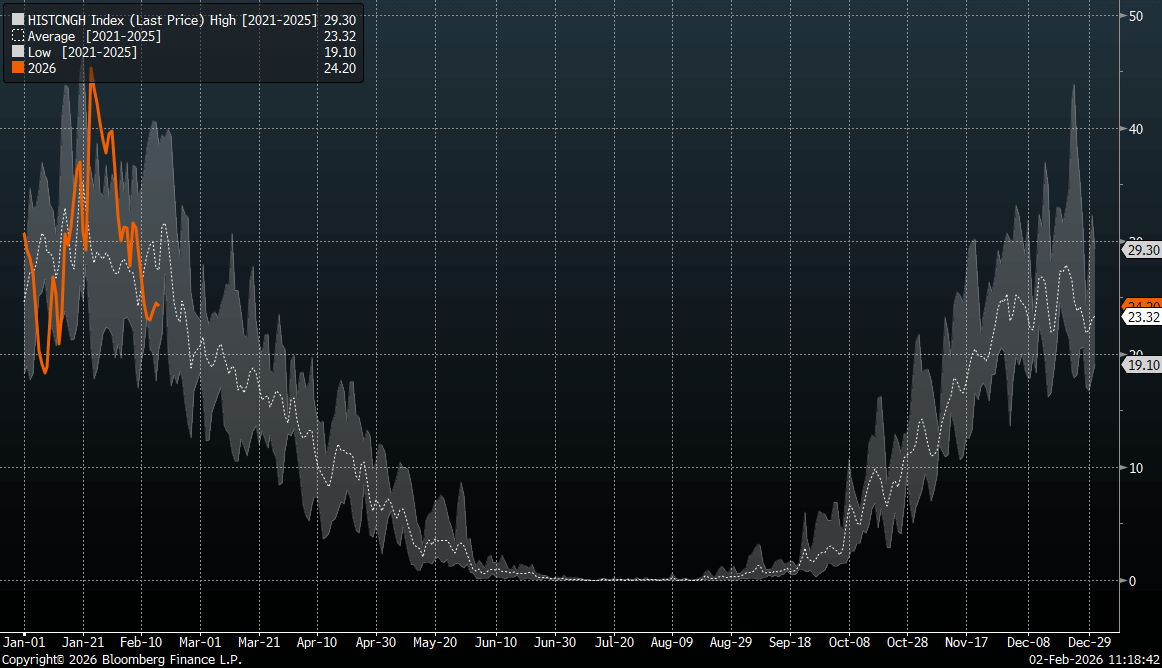

- Indications suggest the worst of the US winter is over. Heating Degree Days (HDD) have fallen below the five-year average, and production has returned above 100 bcfd.

- Forecasts for the next two weeks point to above-average temperatures across almost the entire United States.

- Commodity Weather Group indicates that heating demand for gas could drop below seasonal norms within the next 10 days.

- Despite a recent substantial inventory draw of 242 bcf, stocks remain nearly 10% above last year’s levels and 5% above the five-year average, suggesting the market is well-buffered against any late-season cold snaps.

- Base demand may remain elevated due to increased gas consumption for power generation and higher LNG export volumes.

Demand is beginning to retreat from highly elevated levels. Gas production is returning toward 110 bcfd. Source: Bloomberg Finance LP, XTB

Demand is beginning to retreat from highly elevated levels. Gas production is returning toward 110 bcfd. Source: Bloomberg Finance LP, XTB

The number of Heating Degree Days (HDD) forecasted for the first two weeks of February is falling below the five-year average. Source: Bloomberg Finance LP

The number of Heating Degree Days (HDD) forecasted for the first two weeks of February is falling below the five-year average. Source: Bloomberg Finance LP

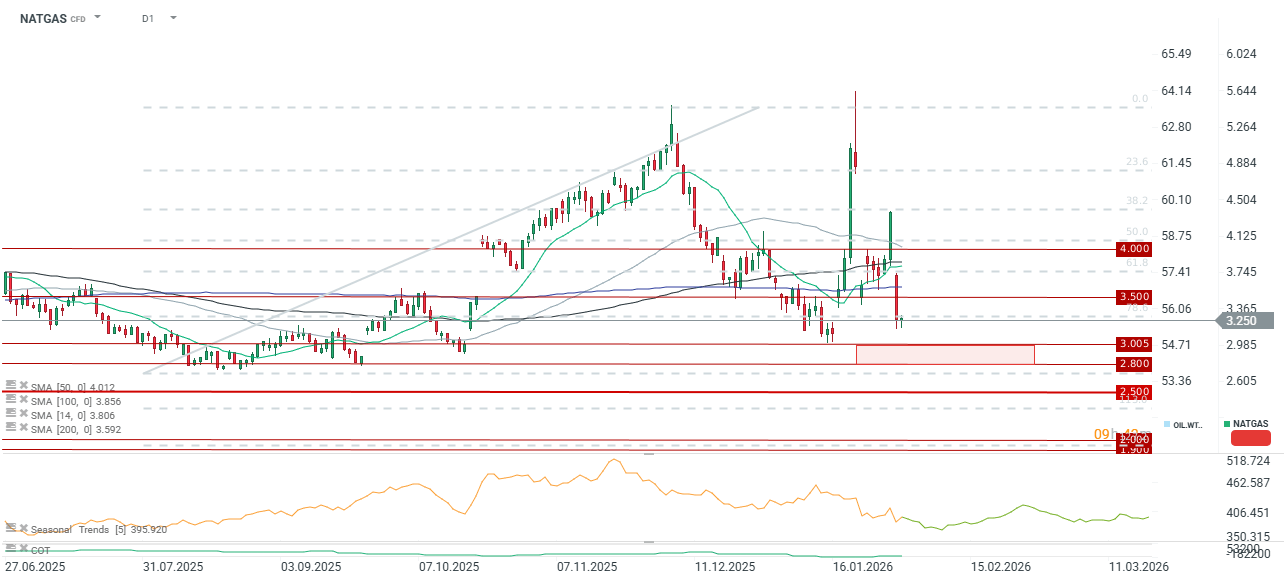

Given the shift in fundamentals, prices may be vulnerable to a drop toward the $2.8–$3.0/MMBTU zone, which would mark the lowest levels since early autumn. However, a return of wintry conditions in late February or March cannot be ruled out. Source: xStation5

Given the shift in fundamentals, prices may be vulnerable to a drop toward the $2.8–$3.0/MMBTU zone, which would mark the lowest levels since early autumn. However, a return of wintry conditions in late February or March cannot be ruled out. Source: xStation5

Cocoa

- Cocoa prices are stabilising above $4,200 per tonne amid slowing arrivals at ports in Ivory Coast. While many reports suggest a lack of appetite among exporters, the slowdown may also point to harvest complications.

- Prices previously dipped below $4,000—the lowest since 2023. Futures are down roughly 30% this year, making cocoa one of the few commodities to suffer such heavy losses in early 2026.

- Port arrivals in Ivory Coast from October 1 to February 1 totalled 1.23 million tonnes, compared to 1.29 million tonnes in the same period last year.

- Technical indicators suggest cocoa is extremely oversold. However, without a demand-side recovery or negative supply signals, this technical oversold condition could theoretically deepen.

- Weather conditions remain conducive to the harvest (the “main crop” is ending, with the “mid-season” due in April). Nonetheless, experts warn that deteriorating weather now could negatively impact the mid-season crop at its peak in May.

- Mondelez is set to report earnings after the Wall Street close. The company is expected to post revenue of $10.31bn, up from $9.6bn. However, profits are projected to fall to 69 cents from $1.30 last year.

- Mondelez has spent several months expressing optimism regarding lower costs due to cheaper cocoa. Analysts expect the company to show a stabilising European market alongside persistent challenges in the US.

- StoneX forecasts a cocoa surplus of 287,000 tonnes for the 25/26 season and 267,000 tonnes for 26/27.

- The ICCO’s late-January report indicated that global cocoa stocks rose to 1.1 million tonnes last season (+4.2% y/y).

- Q4 grind data revealed continued demand destruction, particularly in Europe, where processing fell 8.3% y/y to 304,500 tonnes. Asian grinding dropped 4.8% y/y to 197,000 tonnes, while North America saw a slight 0.3% rise to 103,000 tonnes. Usually, Q4 is seasonally strong due to holiday demand.

- Cocoa is currently relatively cheap, trading at just one-third of its 2024 record highs. However, chocolate prices remain near records as producers are still processing much more expensive beans. Additionally, manufacturers are using high margins to recoup 2024 losses and compensate for market contraction.

- Theoretically, cheaper cocoa should lead to lower chocolate prices, primarily in the second half of this year.

- Notably, cocoa returns to the Bloomberg Commodity Index in 2026. This triggered a return of liquidity to the futures market, though the index-linked buying process was spread over weeks, leading to a massive capitulation of speculative long positions.

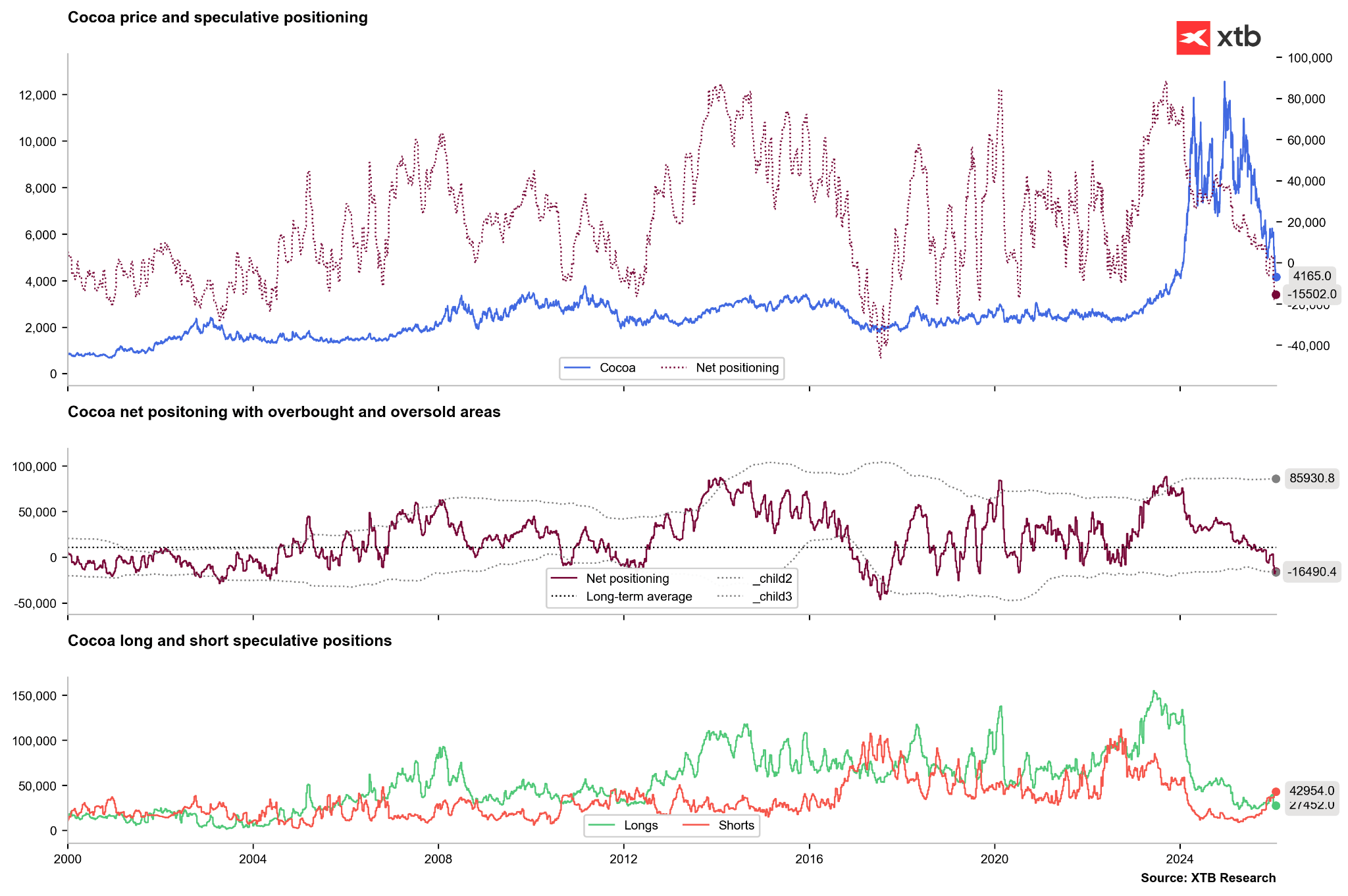

- Open interest remains elevated relative to recent months, but speculators are extremely short-biased according to the CFTC COT report.

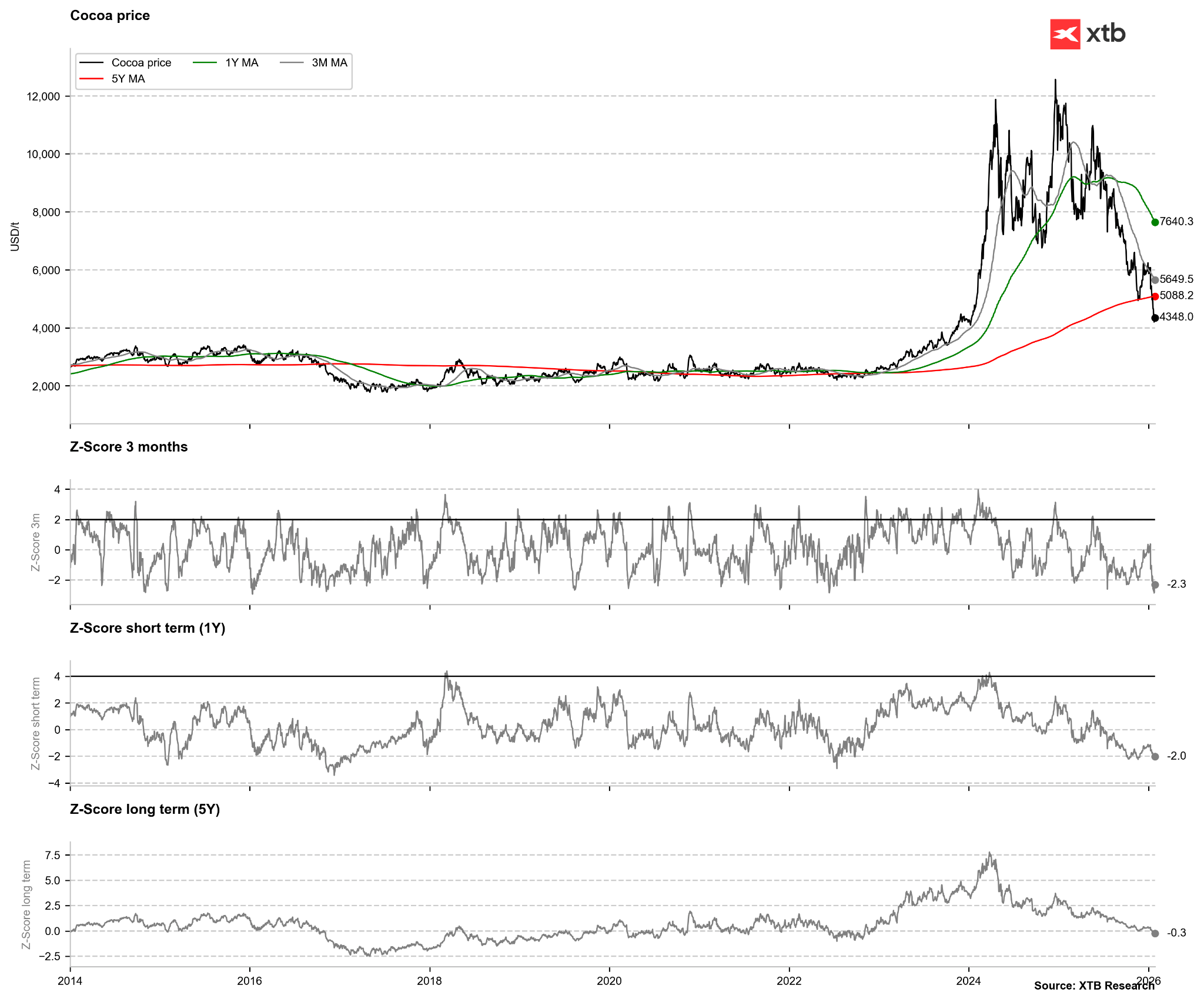

Cocoa is extremely oversold relative to its 3-month and 12-month moving averages. Prices have also fallen below the five-year average. Source: Bloomberg Finance LP, XTB

Cocoa is extremely oversold relative to its 3-month and 12-month moving averages. Prices have also fallen below the five-year average. Source: Bloomberg Finance LP, XTB

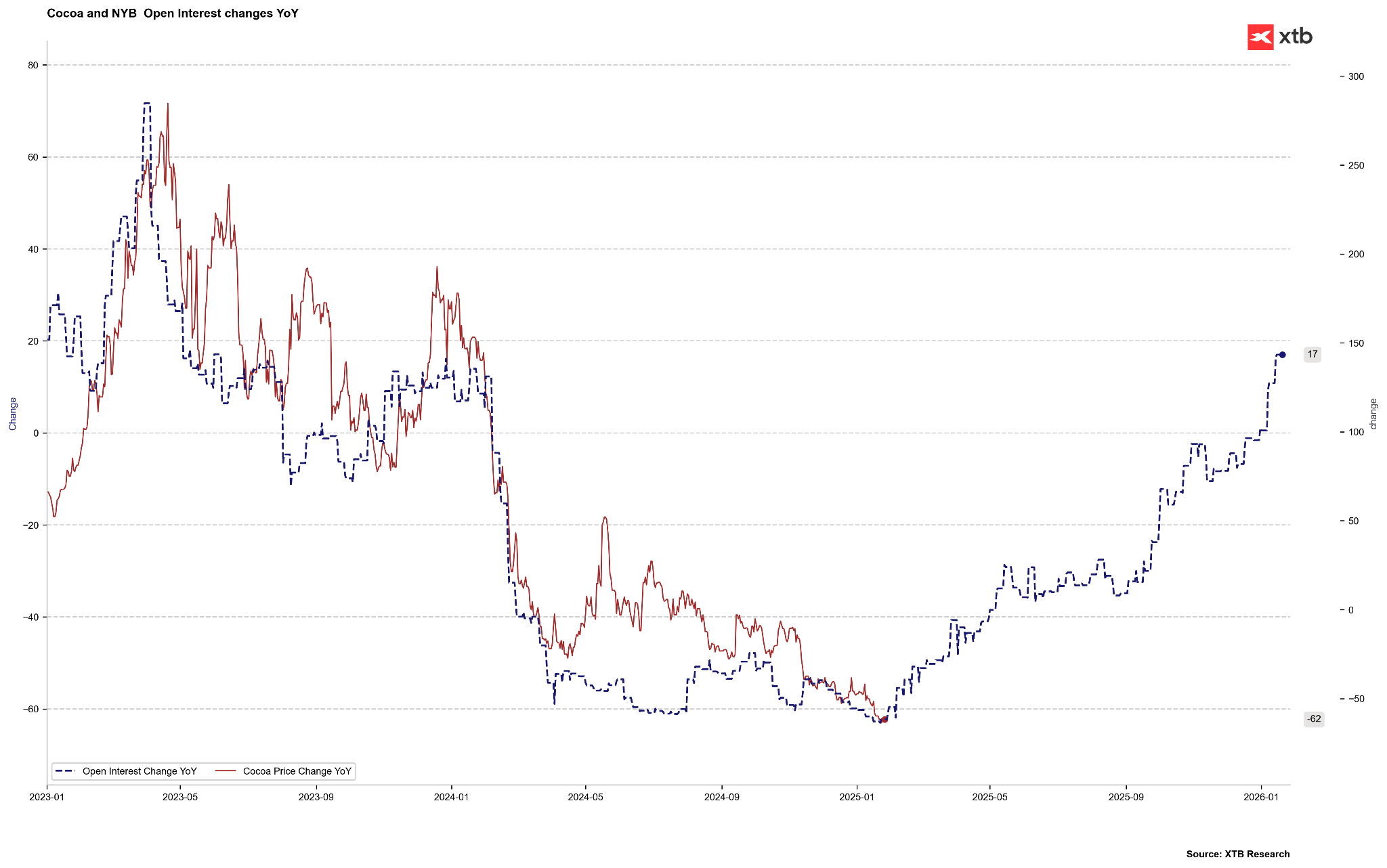

If open interest shifted forward by 12 months serves as a leading indicator for the 12-month price change, it would suggest prices could return to the $8,500–$8,700 range by May. Source: Bloomberg Finance LP, XTB

If open interest shifted forward by 12 months serves as a leading indicator for the 12-month price change, it would suggest prices could return to the $8,500–$8,700 range by May. Source: Bloomberg Finance LP, XTB

Speculators are extremely oversold in the cocoa futures market. Net positions have dropped to levels not seen since 2019/2020. Source: Bloomberg Finance LP

Speculators are extremely oversold in the cocoa futures market. Net positions have dropped to levels not seen since 2019/2020. Source: Bloomberg Finance LP

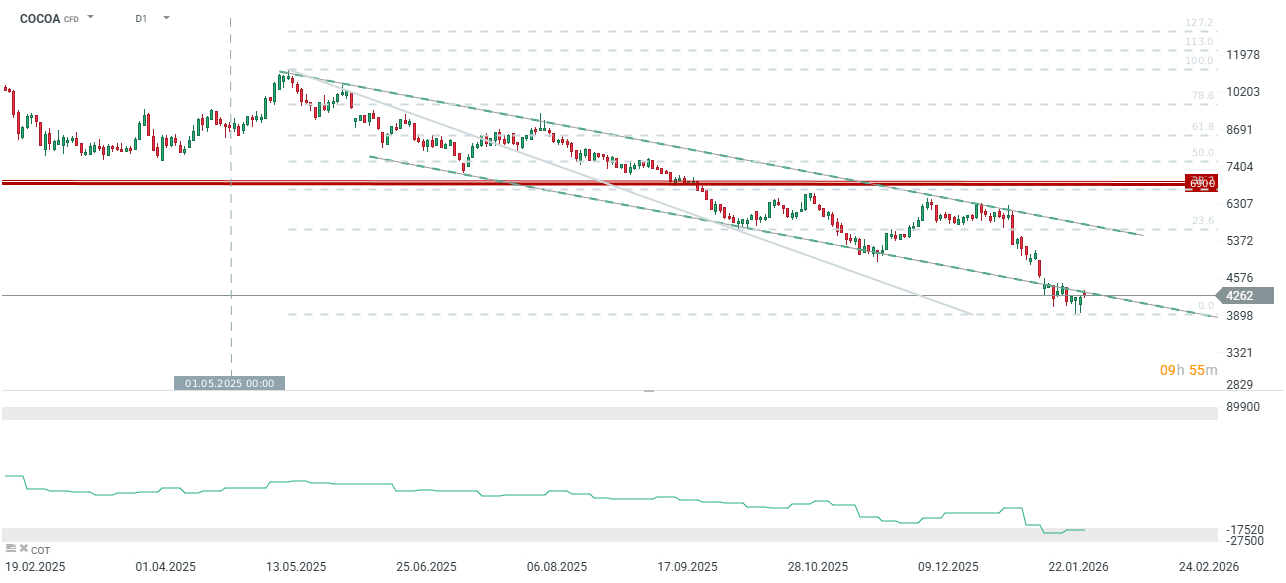

Prices briefly fell below $4,000 per tonne but are showing signs of a slight recovery. A return above the lower limit of the descending trend channel could target $5,000, followed by $5,700 at the 23.6% retracement. Conversely, fresh selling pressure could target the $3,400–$3,500 demand zone. Source: xStation5

Prices briefly fell below $4,000 per tonne but are showing signs of a slight recovery. A return above the lower limit of the descending trend channel could target $5,000, followed by $5,700 at the 23.6% retracement. Conversely, fresh selling pressure could target the $3,400–$3,500 demand zone. Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.