Commodity Talk – Oil, Gold, Natgas and Silver

- Market Reaction: Crude oil prices surged following a coordinated US and Israeli strike on Iran over the weekend. Brent crude surpassed $80 per barrel, while WTI rose above $75 per barrel.

- Fujairah Incident: Recent reports indicate a drone attack on oil storage tanks at the Port of Fujairah in the UAE, pushing Brent prices toward $83 per barrel.

- Strait of Hormuz: Iran has reportedly moved to “close” the Strait of Hormuz, a conduit for 20 million barrels of oil per day. While the passage remains technically open, most firms are unwilling to risk transit, leaving vessels idling on both sides of the strait.

- Logistical Constraints: A significant number of vessels had already halted operations due to a lack of adequate insurance. Furthermore, freight rates have spiked, raising the prospect of a physical shortage of available tankers.

- Production Risk: It is critical to note that a lack of tankers leaves no outlet for storage, which could eventually necessitate production shut-ins.

- Infrastructure: The risk of Iranian strikes on regional oil infrastructure remains a primary concern, although no major damage has been reported thus far. Any escalation could draw Arab state forces directly into the conflict.

- Military Capabilities: Initial reports suggest that Iranian attacks are weakening and lack coordination, potentially indicating successful US efforts in neutralizing key targets. However, while Iran may have exhausted a large portion of its ballistic missile arsenal, it still commands thousands of drones.

- Coalition Forces: European nations have signaled their readiness to support the US in operations against Iran.

- Market Data: Current trading volumes remain relatively thin. Open interest in futures contracts, particularly among speculators, remains notably low.

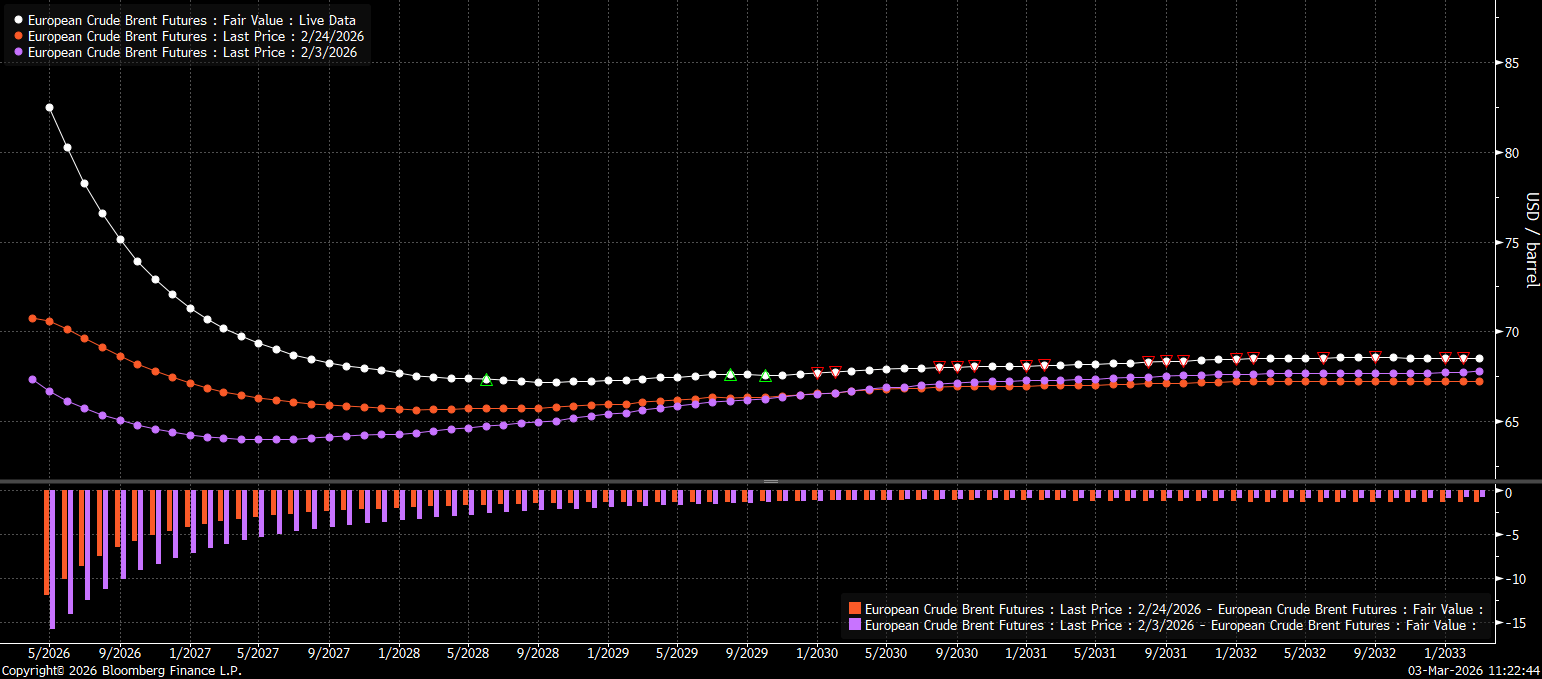

- Forward Curve: The evolution of the forward curve warrants close attention. A decline in long-term prices could signal active hedging by producers looking to lock in current levels. While the market is structurally oversupplied, the immediate crisis is one of logistics.

- Alternative Routes: Key OPEC members, including Saudi Arabia, the UAE, and Iraq, have limited alternative export capacity; however, there is scope to redirect 20–30% of the crude currently flowing through Hormuz.

- US Stance: Marco Rubio has indicated that the US is working to mitigate the impact of rising energy costs on American consumers. Simultaneously, officials have signaled that the Strategic Petroleum Reserve will not be tapped unless prices exceed $100 per barrel.

- Price Dynamics: Prices may prove more volatile than in 2021–2022, a period during which the US actively used reserves to suppress rallies.

- The China Factor: China has been an active buyer recently, bolstering its reserves, but elevated price levels may curb future purchases. Beijing sources crude not only from Iran but across the Persian Gulf. An inability to secure supplies could trigger Chinese diplomatic pressure to reopen the Strait of Hormuz.

- IRGC Blockade: Latest reports suggest that some vessels not affiliated with the US or Israel may be permitted passage. However, the IRGC (Islamic Revolutionary Guard Corps) issued a statement yesterday declaring its intent to block all oil and gas tankers.

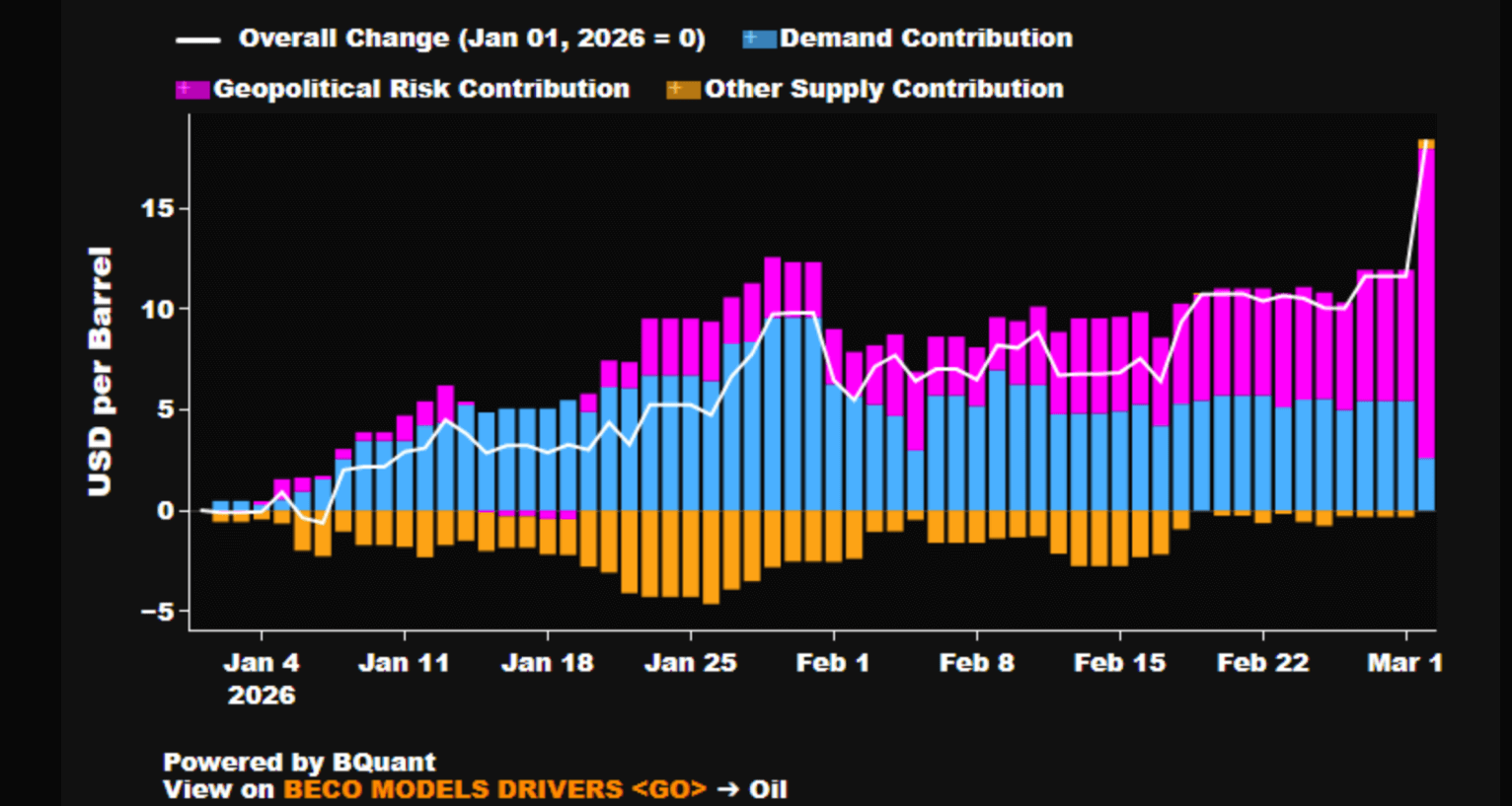

Bloomberg’s model indicates that the geopolitical premium in the oil price is approximately $15 per barrel compared to early January. Source: Bloomberg Economics

Bloomberg’s model indicates that the geopolitical premium in the oil price is approximately $15 per barrel compared to early January. Source: Bloomberg Economics

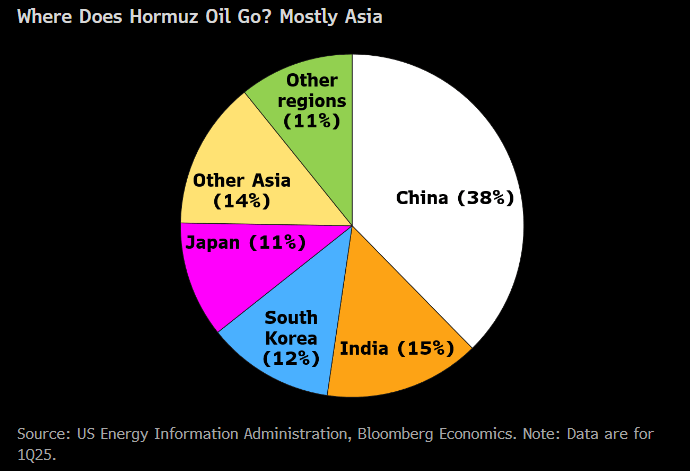

Oil from the Strait of Hormuz primarily serves Asian markets. Consequently, the highest degree of anxiety is visible across Asian equity indices. Theoretically, a sustained surge in oil and gas prices could compel the Bank of Japan to accelerate interest rate hikes. Source: Bloomberg Finance LP

Oil from the Strait of Hormuz primarily serves Asian markets. Consequently, the highest degree of anxiety is visible across Asian equity indices. Theoretically, a sustained surge in oil and gas prices could compel the Bank of Japan to accelerate interest rate hikes. Source: Bloomberg Finance LP

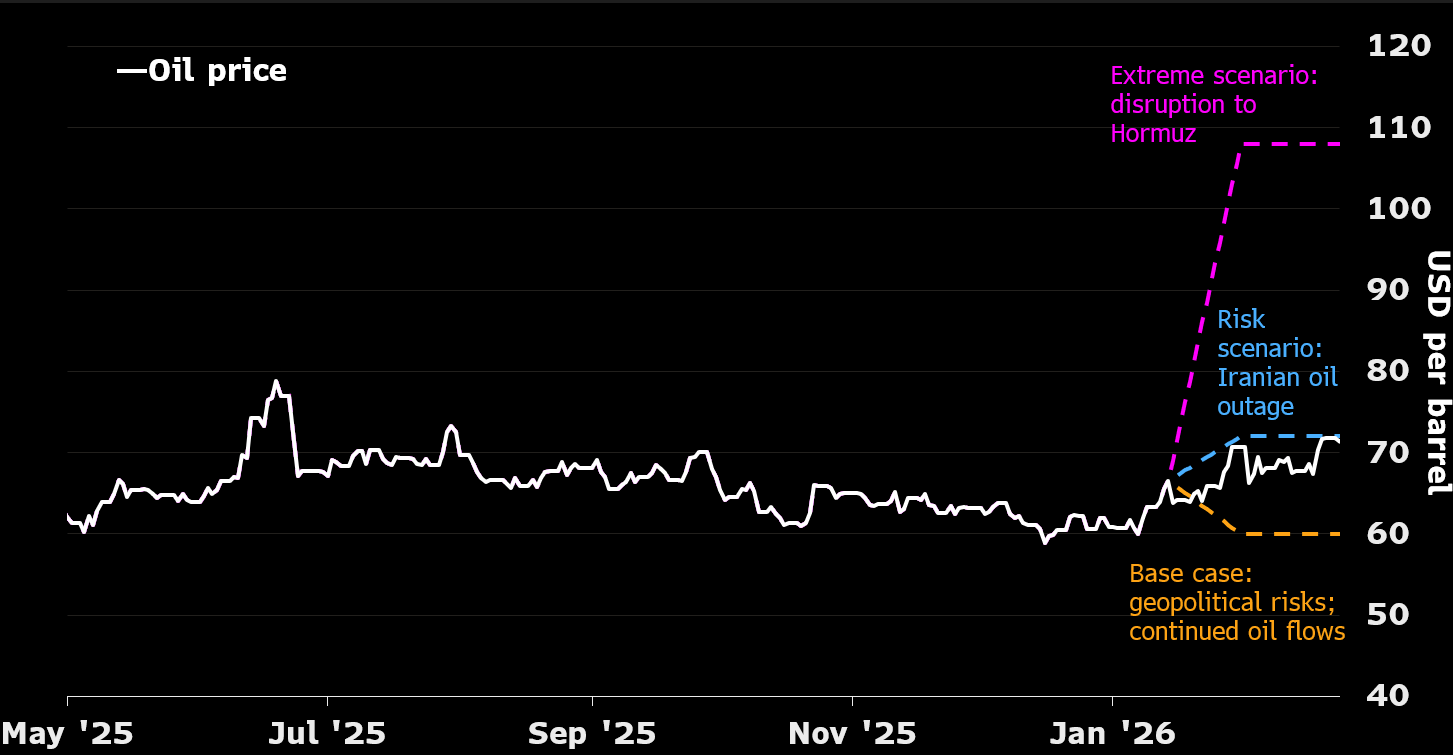

In an extreme scenario, oil prices could exceed $100–$110 per barrel. It is worth noting that the global market is ill-equipped to handle a shortage of Middle Eastern crude lasting longer than a few days to a couple of weeks. Source: Bloomberg Finance LP

In an extreme scenario, oil prices could exceed $100–$110 per barrel. It is worth noting that the global market is ill-equipped to handle a shortage of Middle Eastern crude lasting longer than a few days to a couple of weeks. Source: Bloomberg Finance LP

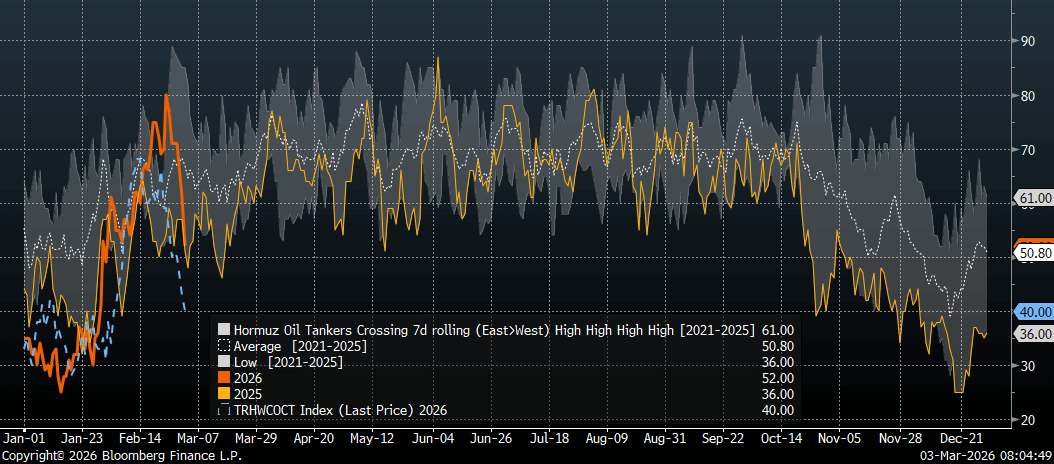

The chart illustrates the 7-day moving average of vessel traffic entering (orange line) and exiting (dashed blue line) the Strait of Hormuz. Source: Bloomberg Finance LP

The chart illustrates the 7-day moving average of vessel traffic entering (orange line) and exiting (dashed blue line) the Strait of Hormuz. Source: Bloomberg Finance LP

We are seeing a marked increase in backwardation for Brent crude compared to one week and one month ago. However, extreme spreads between the two front-month contracts have yet to materialize. Source: Bloomberg Finance LP

We are seeing a marked increase in backwardation for Brent crude compared to one week and one month ago. However, extreme spreads between the two front-month contracts have yet to materialize. Source: Bloomberg Finance LP

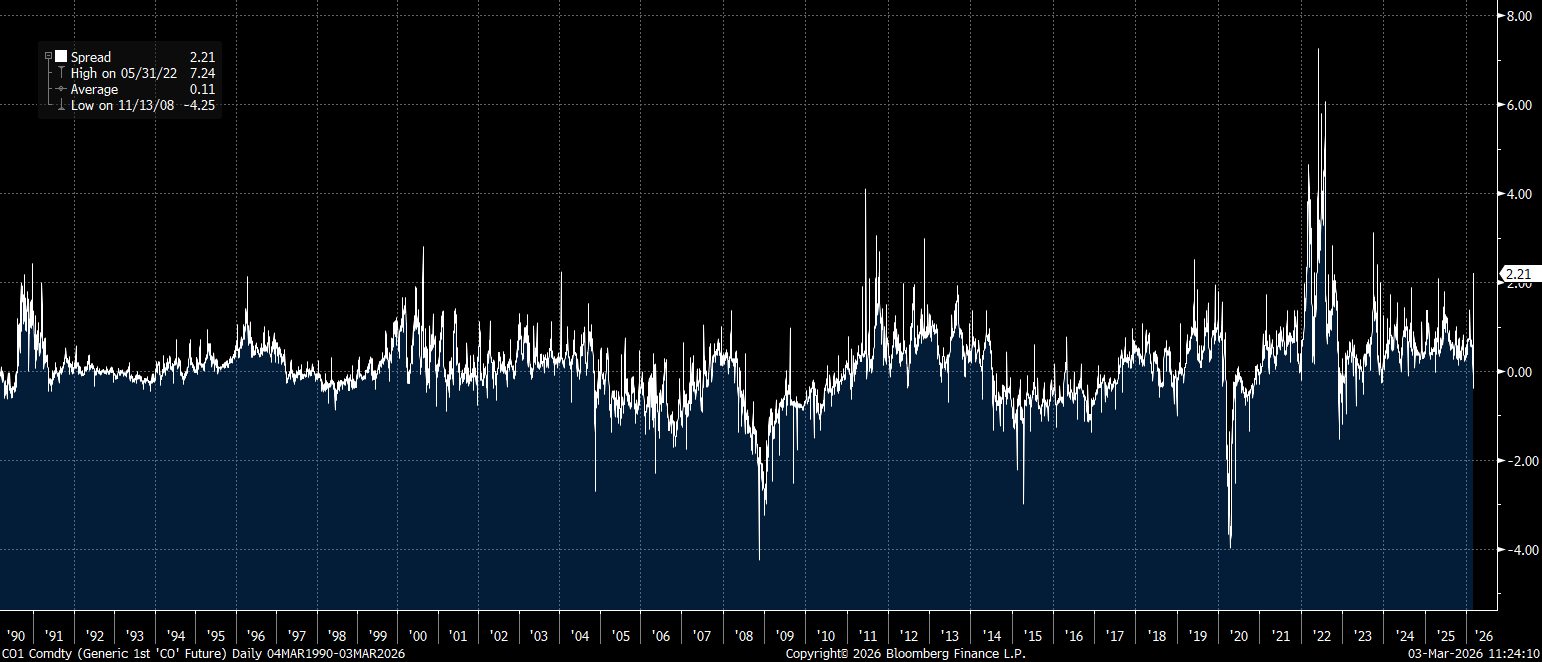

The spread between the current and the next front-month Brent contract exceeds $2. Over the last two years, this has served as a clear contrarian indicator. Nonetheless, 2011 and particularly 2022 demonstrate that oil prices still possess upside potential at the short end of the curve before reaching total extremes. Source: Bloomberg Finance LP

The spread between the current and the next front-month Brent contract exceeds $2. Over the last two years, this has served as a clear contrarian indicator. Nonetheless, 2011 and particularly 2022 demonstrate that oil prices still possess upside potential at the short end of the curve before reaching total extremes. Source: Bloomberg Finance LP

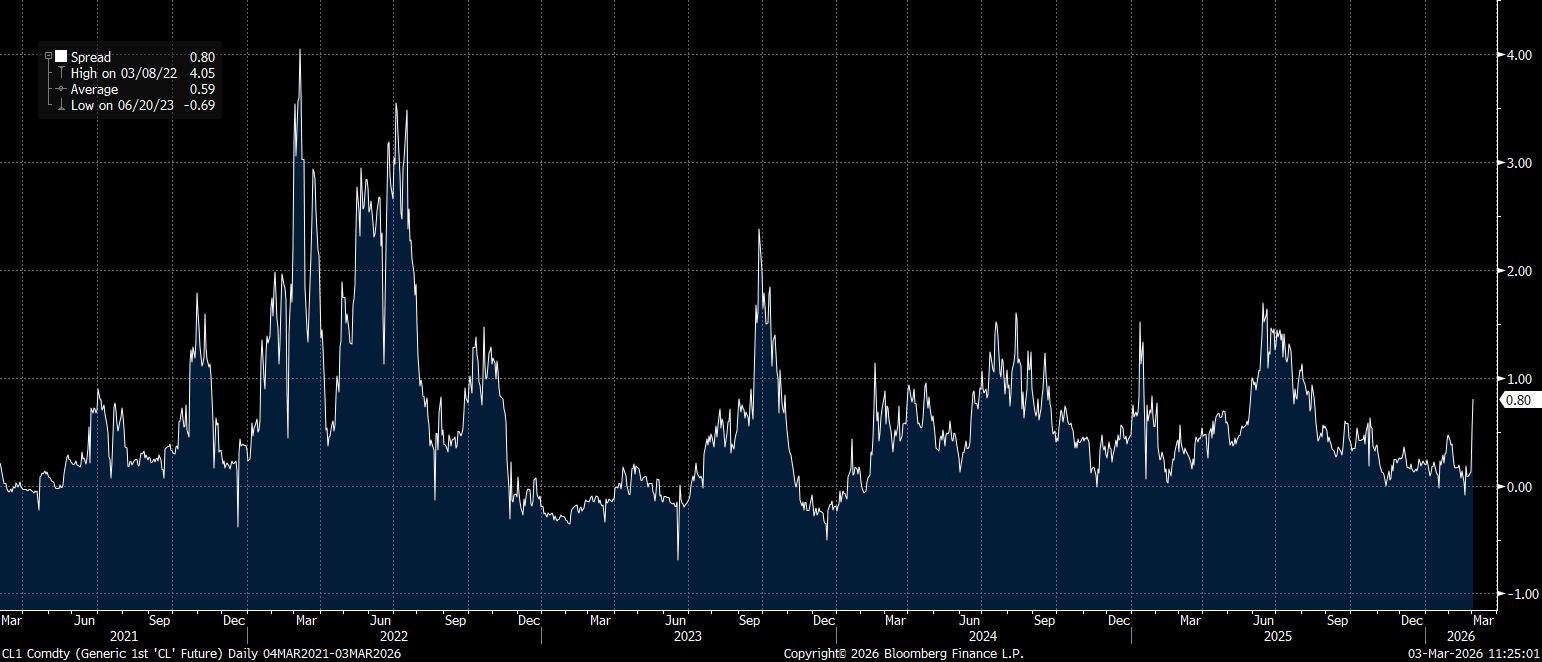

The front-month spread for WTI reflects its relative distance from the conflict. However, WTI is likely to sharply narrow the gap with Brent in the event of a prolonged conflict. Source: Bloomberg Finance LP

The front-month spread for WTI reflects its relative distance from the conflict. However, WTI is likely to sharply narrow the gap with Brent in the event of a prolonged conflict. Source: Bloomberg Finance LP

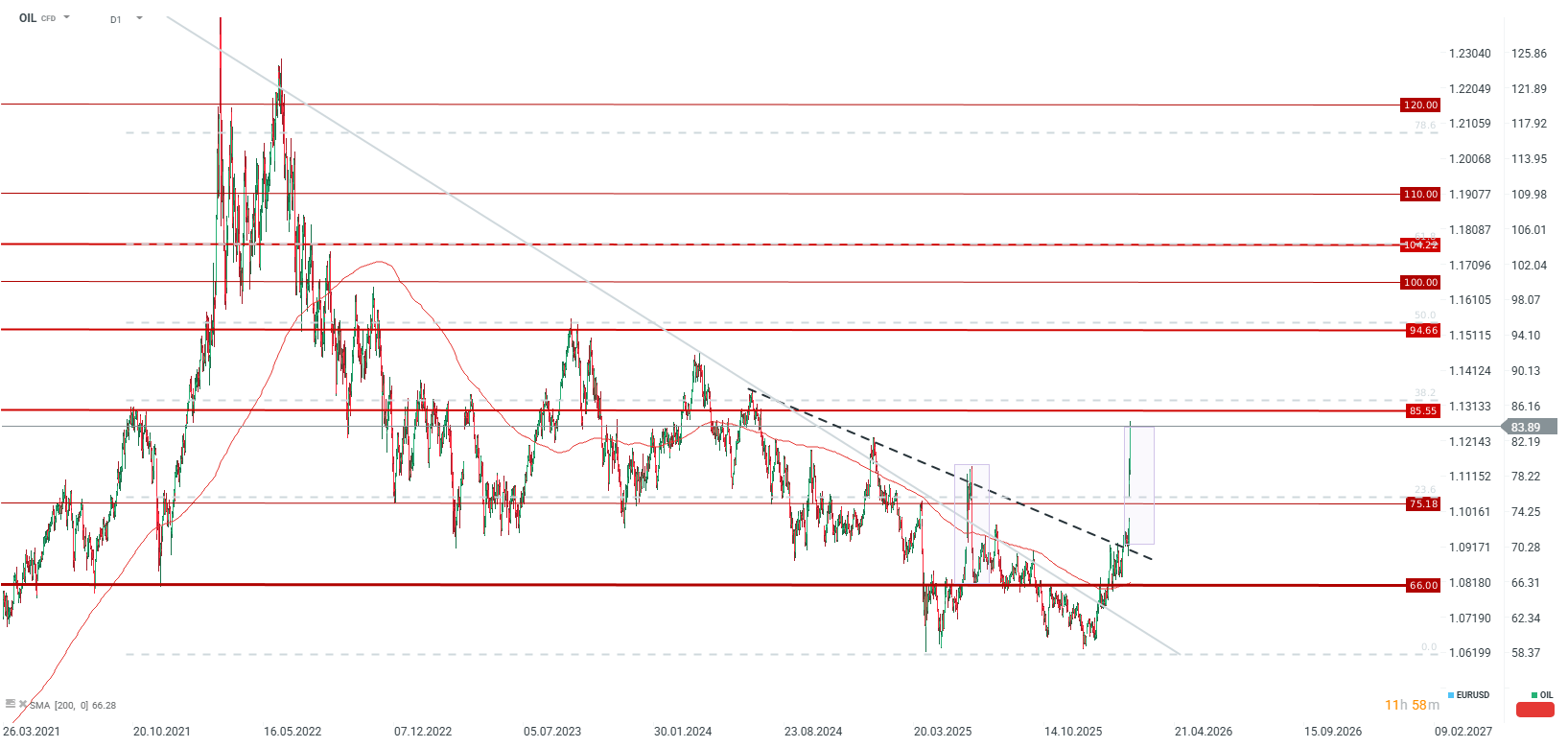

Brent crude is currently testing the $84 per barrel level, its highest point since July 2024. Source: xStation5

Brent crude is currently testing the $84 per barrel level, its highest point since July 2024. Source: xStation5

Natural Gas

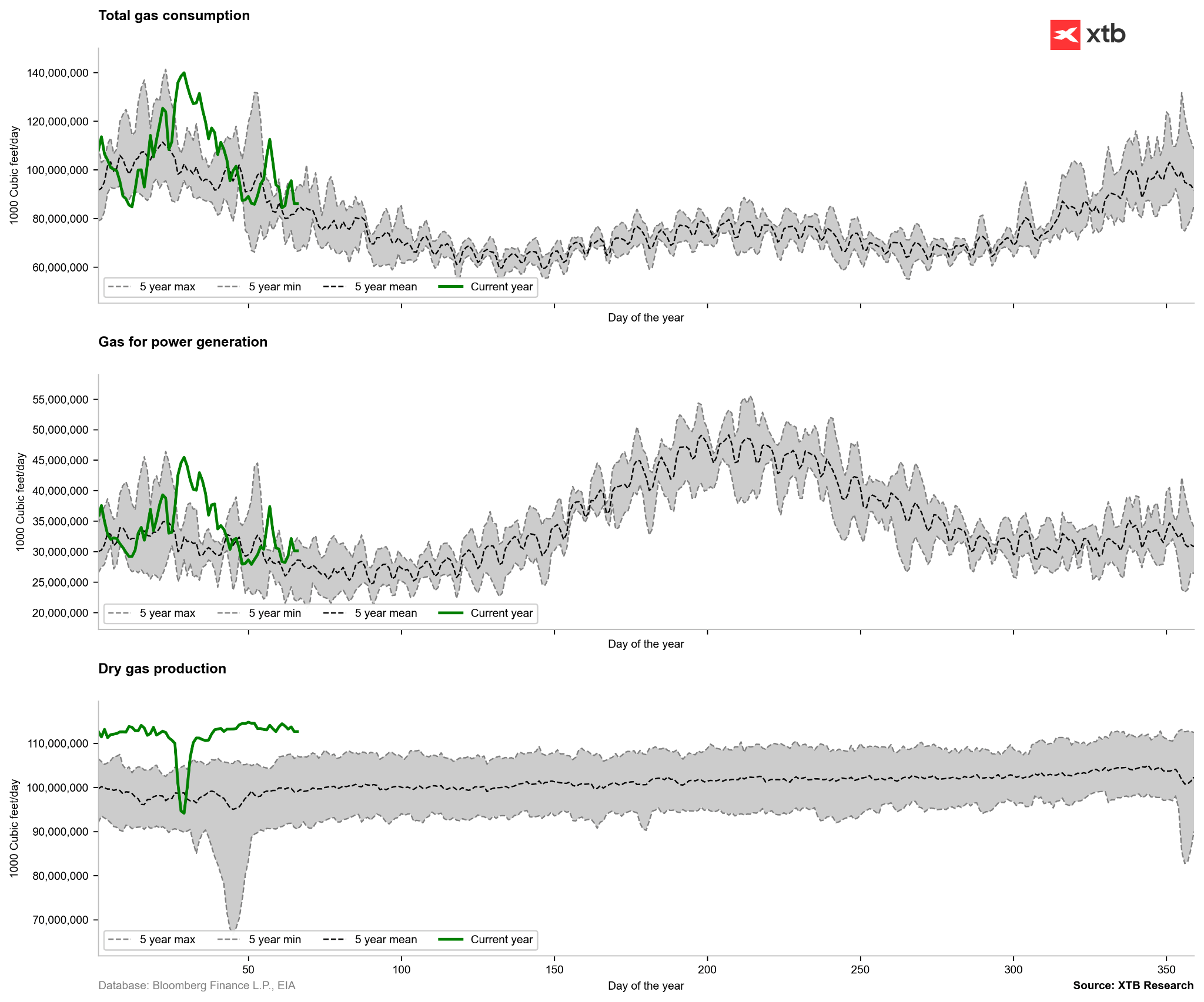

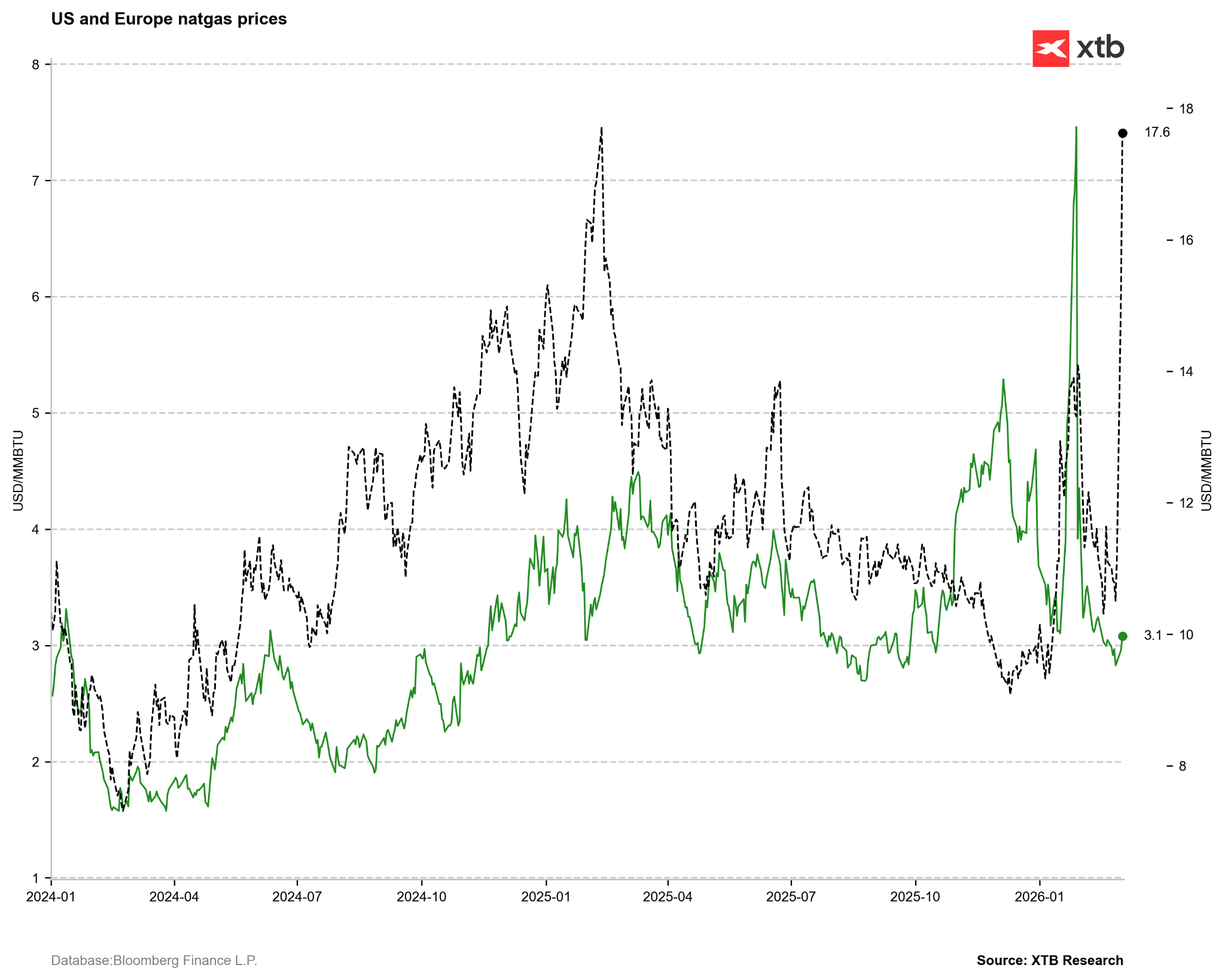

- US Domestic Situation: US natural gas prices are primarily reacting to domestic factors. Weather forecasts indicate a significant decline in heating demand.

- LNG Pricing: Conversely, LNG prices in Europe and Asia are surging to extreme highs. A rise in spot LNG prices could partially pull US domestic prices higher.

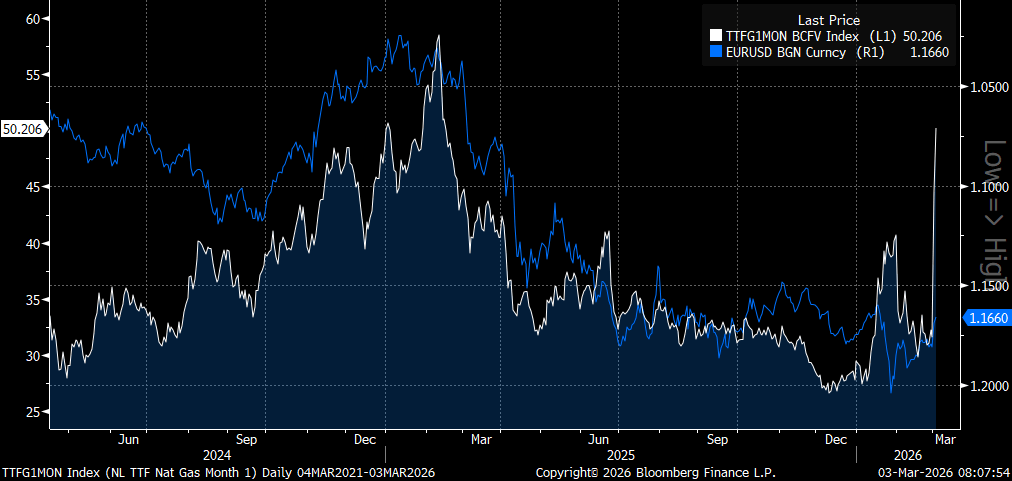

- European Volatility: European TTF gas prices rose 40% today, and nearly 100% since Monday. This surge is drastic for all energy-importing nations, including the EU, Japan, South Korea, India, and parts of China.

- Currency Impact: The Euro is highly vulnerable to further spikes in TTF prices, as evidenced by a clear correlation. Should current gas price trends persist, the EURUSD pair is at risk of falling below 1.10.

- Storage Levels: Despite the end of the heating season in Europe, storage facilities are only 30% full. In the US, the heating season is also theoretically nearing its conclusion.

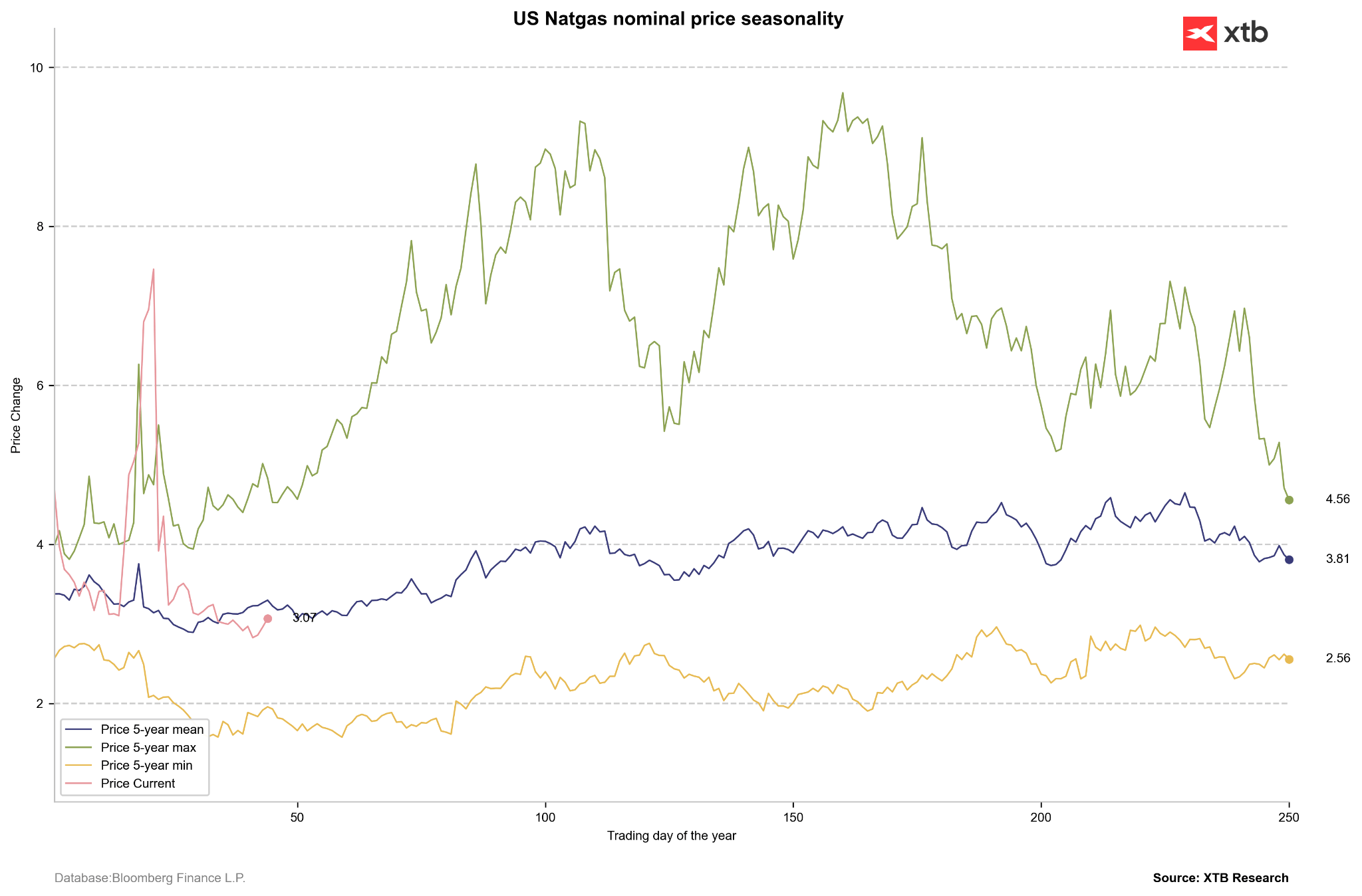

- Technical Outlook: Given the current trend, US prices could test the $3.3–$3.5/MMBTU range.

A sharp rise in European gas prices could lead to significant Euro weakness. Source: Bloomberg Finance LP

A sharp rise in European gas prices could lead to significant Euro weakness. Source: Bloomberg Finance LP

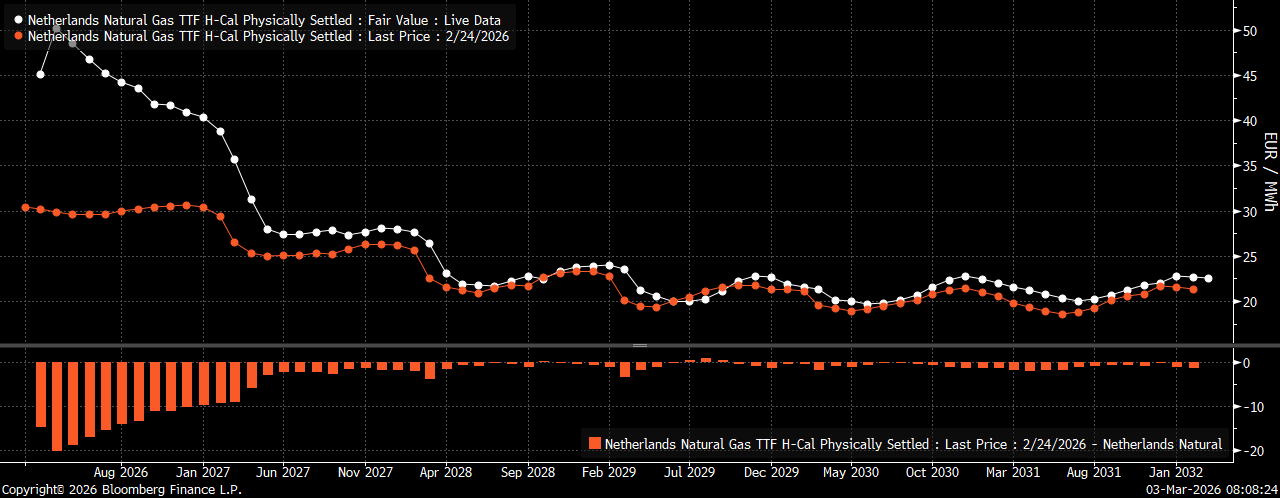

Significant backwardation has emerged in the natural gas market within the last week. Interestingly, while Qatar is not a dominant player for Europe in terms of immediate deliveries, the market is reacting sharply. Source: Bloomberg Finance LP

Significant backwardation has emerged in the natural gas market within the last week. Interestingly, while Qatar is not a dominant player for Europe in terms of immediate deliveries, the market is reacting sharply. Source: Bloomberg Finance LP

US gas demand is stabilizing, but prices may react to the shifting dynamics of the global LNG market. Source: Bloomberg Finance LP, XTB

US gas demand is stabilizing, but prices may react to the shifting dynamics of the global LNG market. Source: Bloomberg Finance LP, XTB

Seasonality in the gas market currently suggests a potential recovery through the end of April and into early May. Source: Bloomberg Finance LP, XTB

Seasonality in the gas market currently suggests a potential recovery through the end of April and into early May. Source: Bloomberg Finance LP, XTB

TTF gas served as a benchmark for US gas prices in 2024. On the other hand, we rarely observe moves as large as 40% in a single day or 100% within two days. Source: Bloomberg Finance LP, XTB

TTF gas served as a benchmark for US gas prices in 2024. On the other hand, we rarely observe moves as large as 40% in a single day or 100% within two days. Source: Bloomberg Finance LP, XTB

Gold

- Geopolitical Hedge: Gold rallied at the start of the week in response to escalating risks in the Middle East. Prices approached record closing highs, though they remain some distance from the intraday ATH (All-Time High).

- Correction and Cash Demand: The second day of the week saw a massive 3% retracement, likely tied to a surge in demand for cash. Simultaneously, EURUSD has pulled back below the 1.16 level.

- Inflation and Rates: The spike in oil and gas prices may signal a return of inflation and a corresponding rise in rate hike expectations. The market is currently pricing in only 1.5 rate cuts from the Fed this year. Notably, the ISM Manufacturing Prices Paid index rose above 70, signaling a clear resurgence of price pressure.

- Monetary Factors: While institutional demand for gold is likely to persist, a shift in monetary rhetoric could undermine the foundation for further price appreciation.

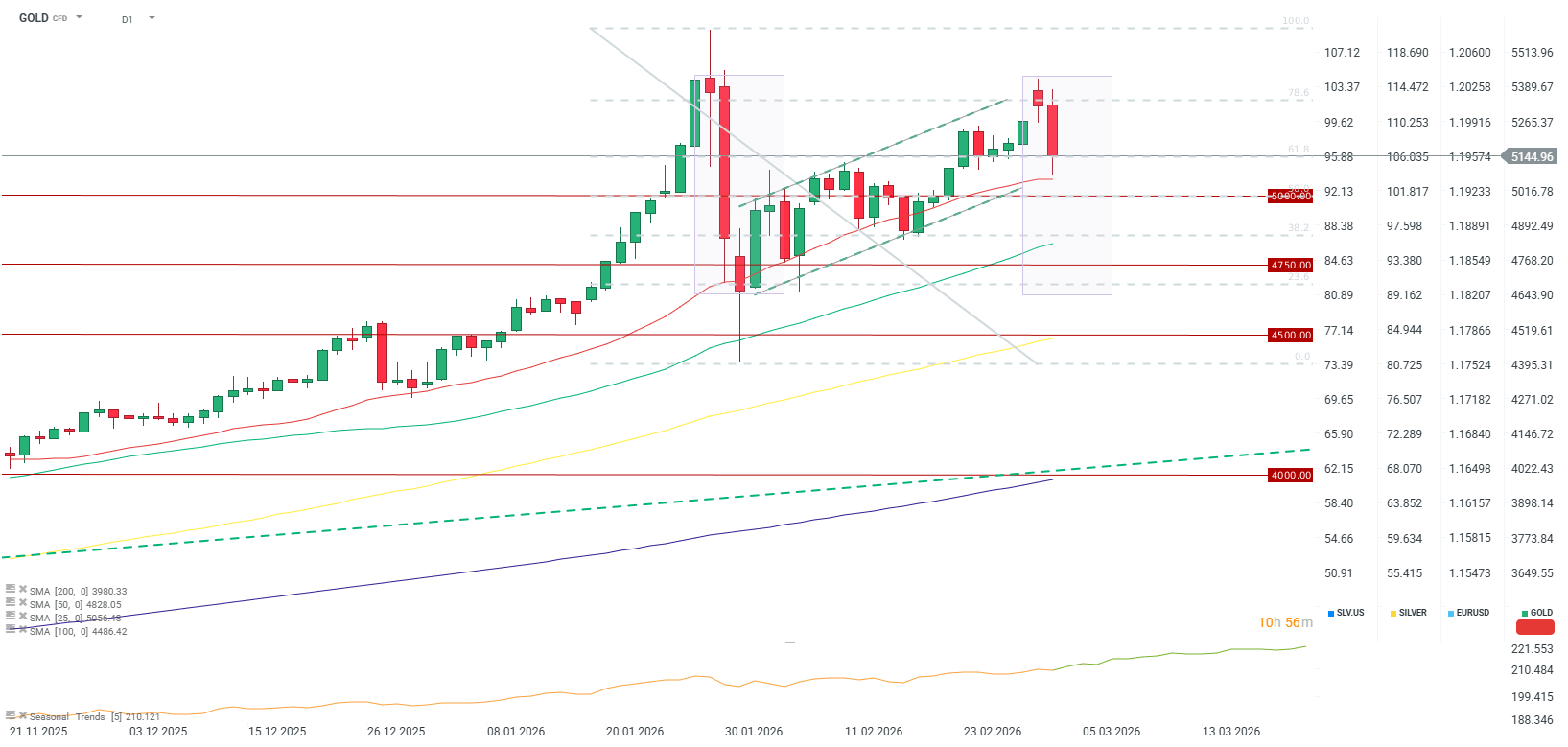

- Technical Analysis and the Dollar: Gold is clearly losing ground as the US Dollar strengthens. We are observing a period of appreciation similar to that seen in late January/early February. From a technical standpoint, a double-top formation is appearing on the gold chart.

Gold is weakening significantly alongside the strengthening US Dollar. We are currently observing a reinforcement similar to that of the turn of January and February. Theoretically, we are also dealing with a double-top on gold. Source: xStation5

Gold is weakening significantly alongside the strengthening US Dollar. We are currently observing a reinforcement similar to that of the turn of January and February. Theoretically, we are also dealing with a double-top on gold. Source: xStation5

Silver

- Geopolitical Reaction: Silver opened near $95 following the weekend strikes by the US and Israel on Iran.

- Profit Taking: A “buy the rumor, sell the fact” scenario is unfolding in both gold and silver. Investors are opting to realize profits following the aggressive rallies of the past fortnight.

- Sharp Sell-off: Silver has shed up to 9% during the second session of the week, with losses reaching as much as 12% at one point during Tuesday’s trading.

- Options Market: The silver options market remains extremely overheated, as investors continue to hedge against violent price spikes on a weekly or monthly horizon.

- Asset Class Profile: Silver is currently being treated more as a speculative asset, though it remains a precious metal highly correlated with gold.

- Equities Correlation: Silver may now react more acutely to moves in equity markets. A sharp sell-off in stocks could weigh on silver prices; on Tuesday, March 3, we observed a pullback of nearly 7%.

- Risk Factors and COMEX: The heat in the options market was driven by two factors: the risk of war with Iran and fears regarding a shortage of deliverable silver on the COMEX.

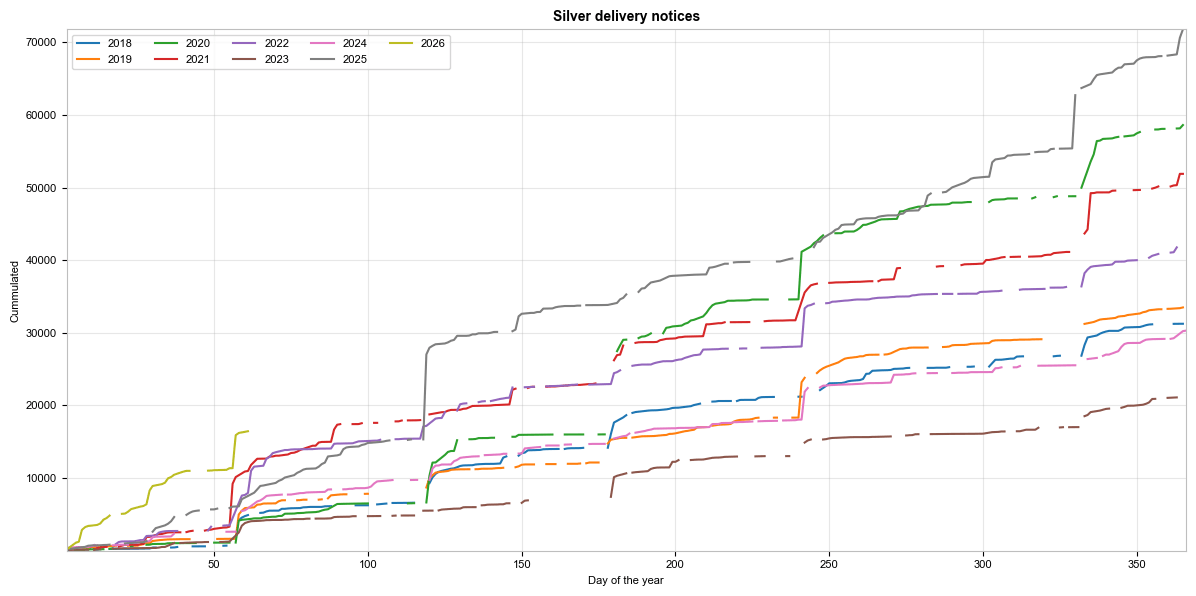

- Deliveries and Inventories: The latter risk factor has been largely mitigated. On Monday, March 2, nearly 5,000 delivery contracts were closed (though there is no current evidence that this silver has been withdrawn from warehouses). Currently, only 1,500 open contracts remain on the March maturity, with registered stocks at approximately 80 million ounces.

Delivery notices. A clear increase is visible at the beginning of March, but the number of open positions on the March contract is now minimal. Further concerns regarding silver availability are not expected until April, ahead of the May contract expiry. Source: Bloomberg Finance LP, XTB

Delivery notices. A clear increase is visible at the beginning of March, but the number of open positions on the March contract is now minimal. Further concerns regarding silver availability are not expected until April, ahead of the May contract expiry. Source: Bloomberg Finance LP, XTB

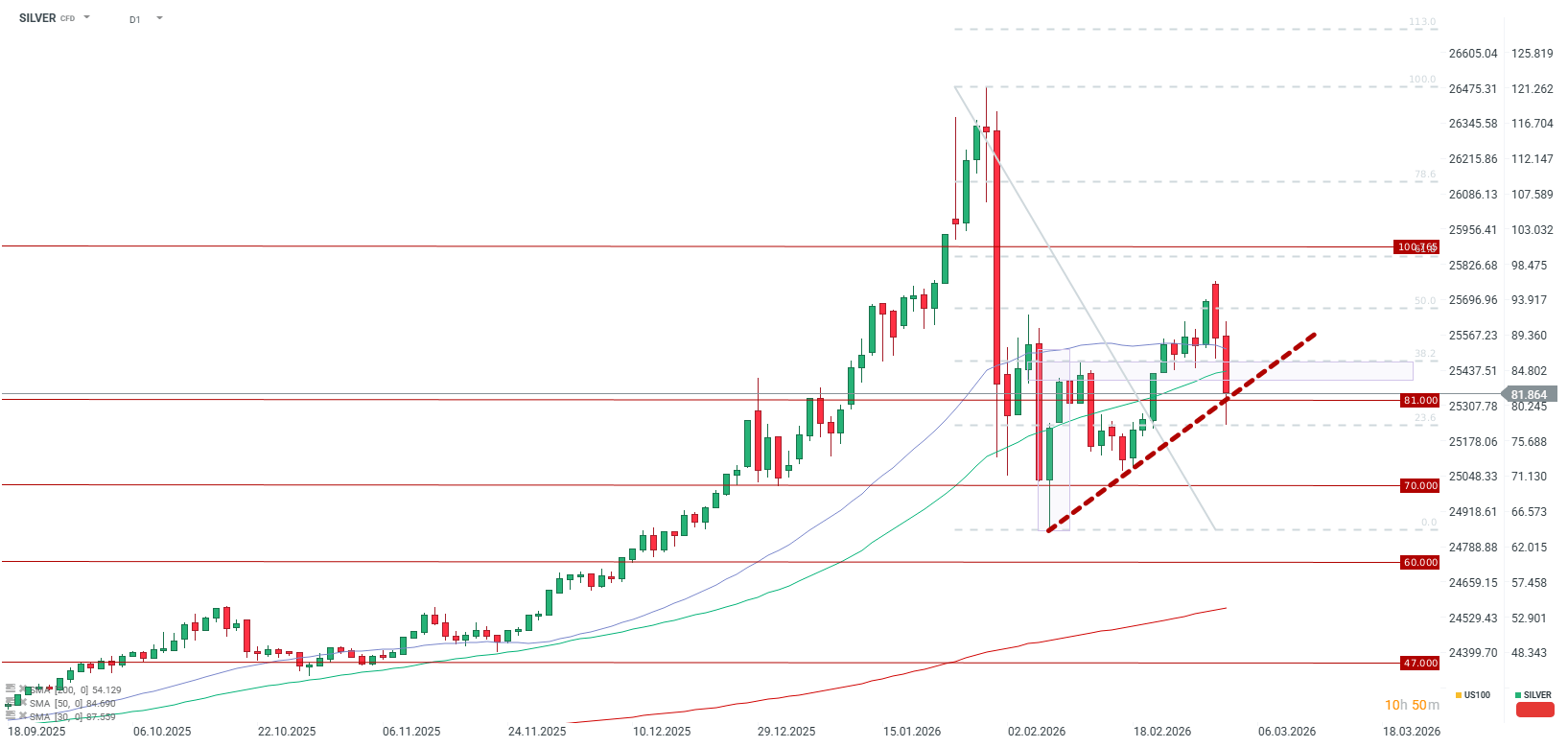

Silver is reacting to equity market declines, the rising probability of an inflation rebound, and profit-taking. If the price closes below $80 per ounce, a move to retest $70 is possible. A return above the 30-50 day moving averages would suggest a potential base for a rally toward the $100–$120 range. Source: xStation5

Silver is reacting to equity market declines, the rising probability of an inflation rebound, and profit-taking. If the price closes below $80 per ounce, a move to retest $70 is possible. A return above the 30-50 day moving averages would suggest a potential base for a rally toward the $100–$120 range. Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.