Commodity Talk – Gold, Natgas, Silver and Cocoa

Gold:

- Gold is gaining fresh momentum as uncertainty spikes following the Supreme Court’s decision to strike down President Trump’s tariffs imposed under the IEEPA.

- Donald Trump has imposed a 15% global tariff on all products, leading to significant ambiguity regarding whether these are additional duties or replacements for the previous ones.

- Donald Trump’s trade policy in 2025 has been a primary driver for the gold market.

- Gold prices are further bolstered by geopolitical risks involving Iran, and to a lesser extent, the situations in the Middle East, Ukraine, and Venezuela.

- The metal is also benefiting from institutional investors’ positioning in safe-haven assets, as US and Japanese bonds continue to lose ground relative to gold.

- The Federal Reserve is widely expected to hold interest rates steady at its upcoming meeting, though February labor market data remains a crucial focal point.

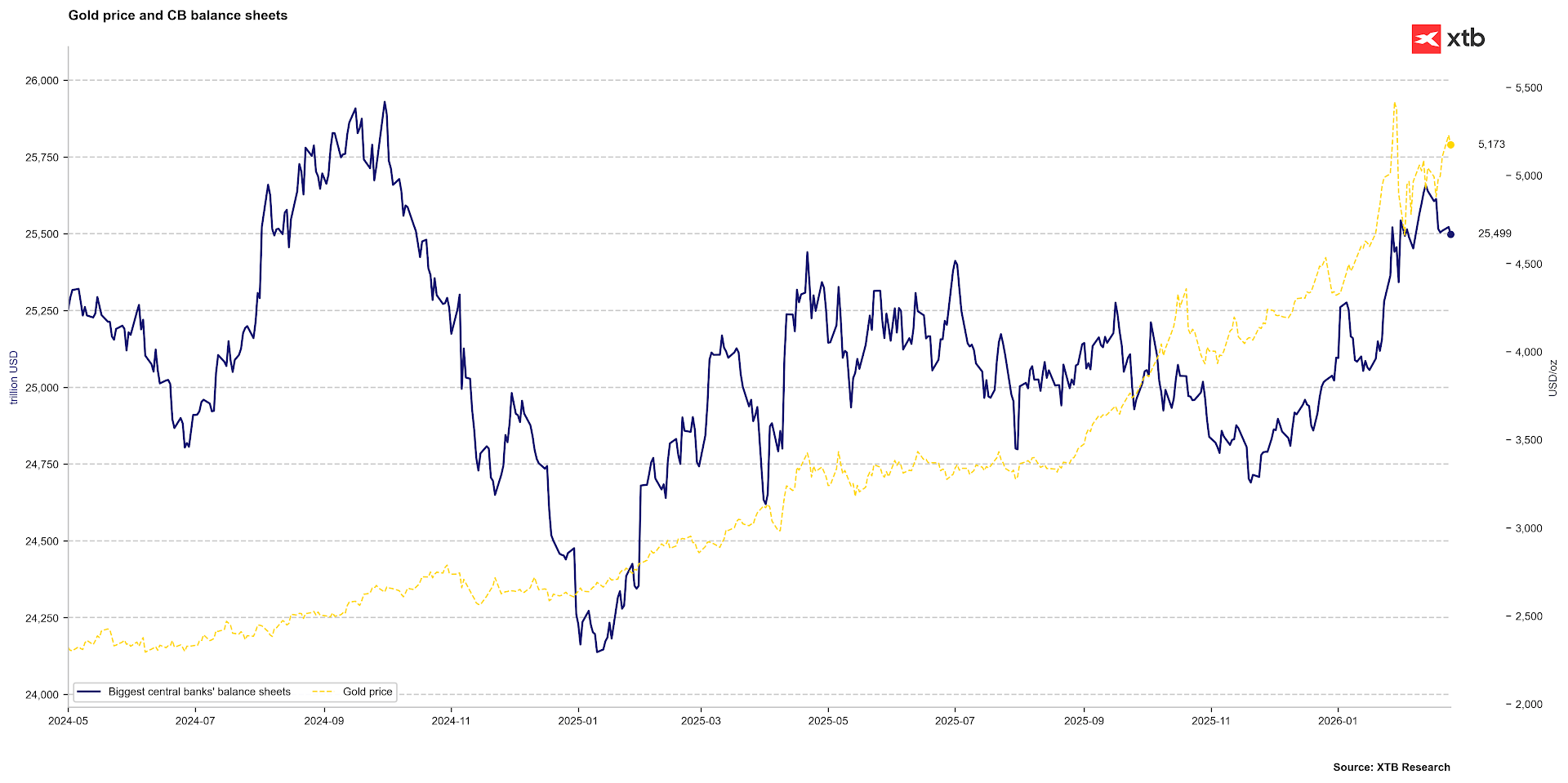

- Gold was significantly supported by expanding central bank balance sheets from November to February; the current slight reversal has impacted recent price action.

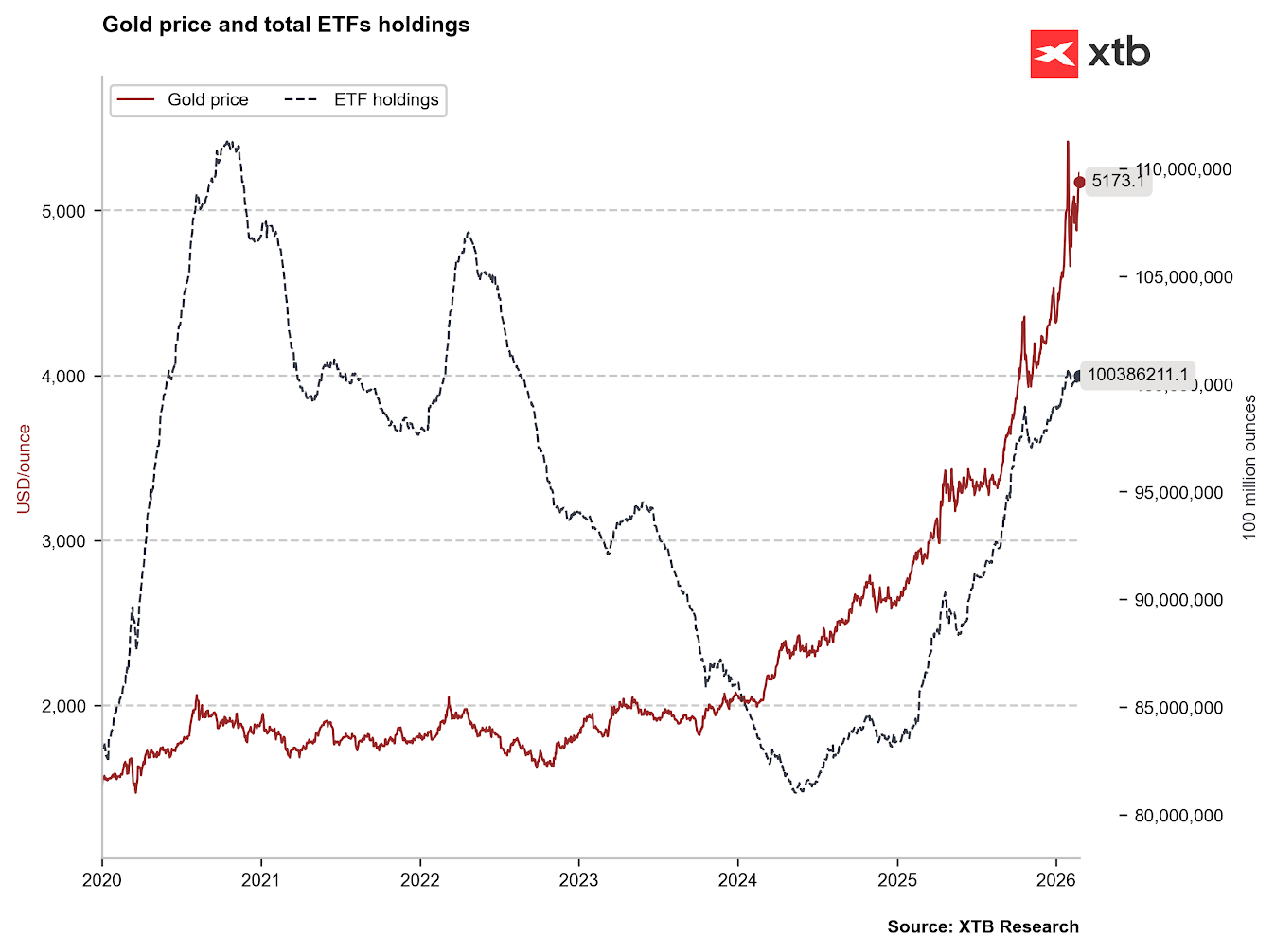

- After a brief pause, ETFs have resumed gold purchases.

Central bank balance sheets have ceased expanding, which may have halted the metal’s further gains. Source: Bloomberg Finance LP, XTB

ETFs have resumed gold purchases following a brief hiatus. Source: Bloomberg Finance LP, XTB

ETFs have resumed gold purchases following a brief hiatus. Source: Bloomberg Finance LP, XTB

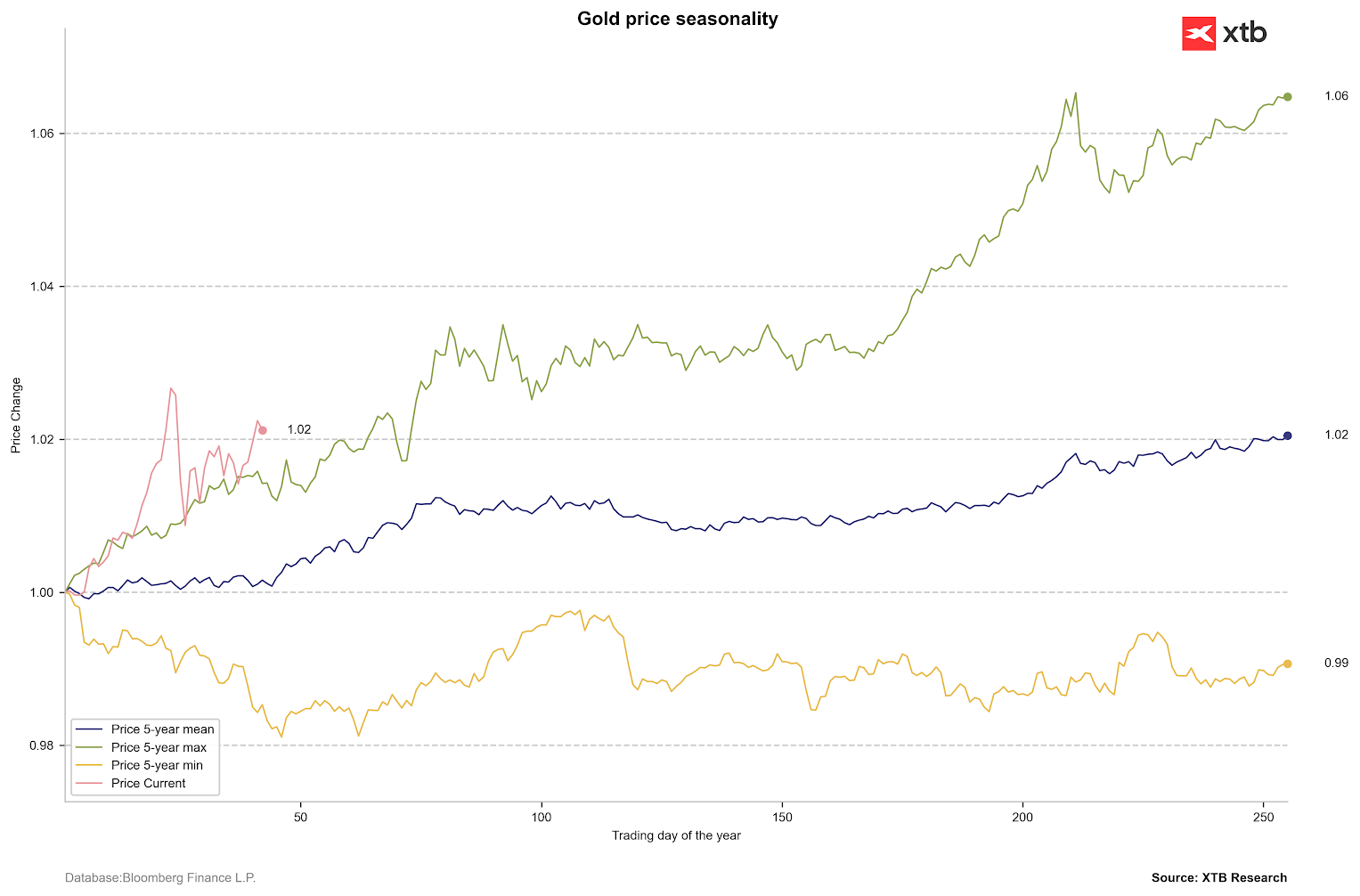

Despite late-January headwinds, gold is currently outperforming its strongest 5-year historical performance. It is worth noting that a period of consolidation typically occurs in the second quarter. Source: Bloomberg Finance LP, XTB

Despite late-January headwinds, gold is currently outperforming its strongest 5-year historical performance. It is worth noting that a period of consolidation typically occurs in the second quarter. Source: Bloomberg Finance LP, XTB

Silver:

- Silver is reacting positively in tandem with gold, driven by international trade risks and geopolitical tensions.

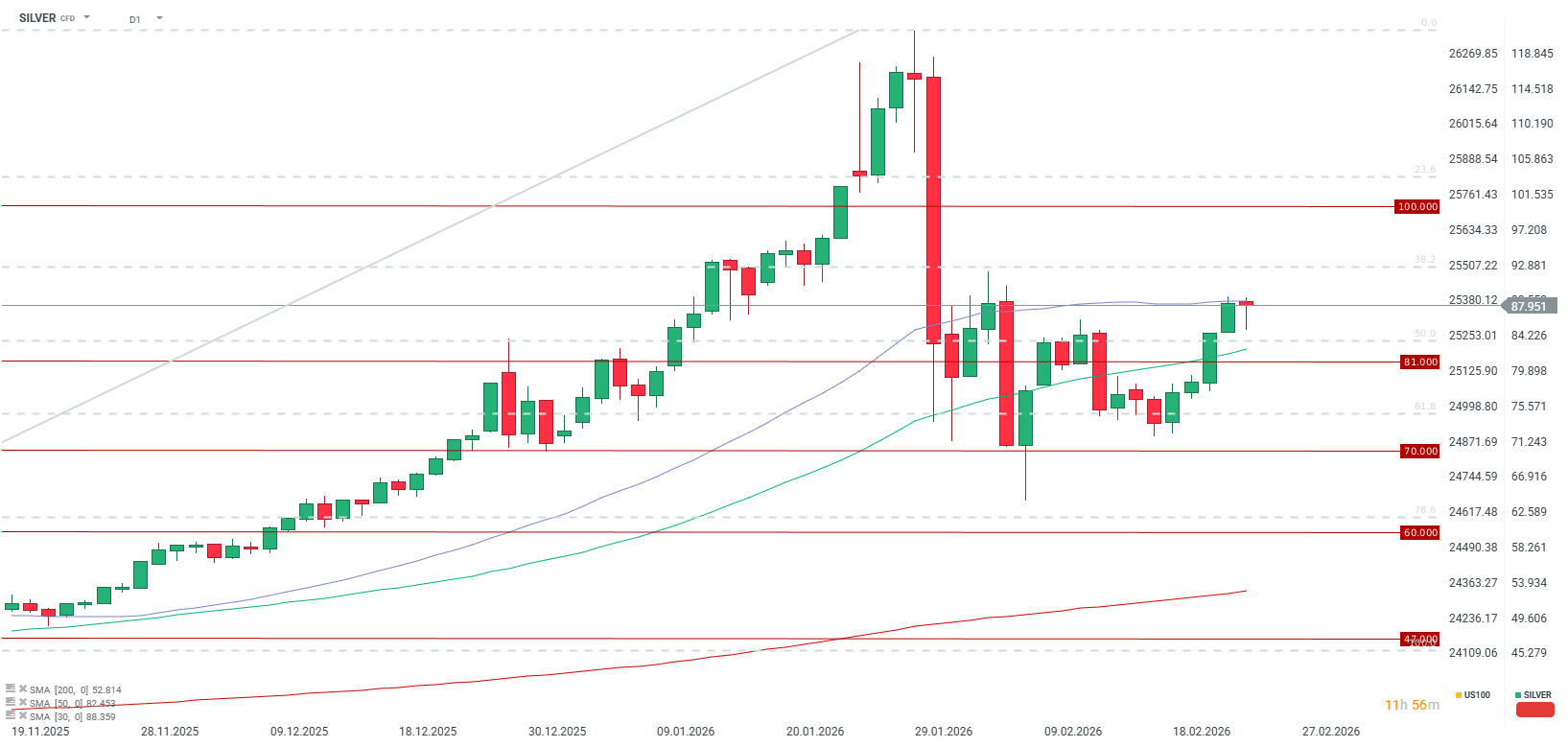

- Prices have returned to levels near $90 per ounce, reclaiming peaks seen in early February; the 30-day SMA is currently being tested.

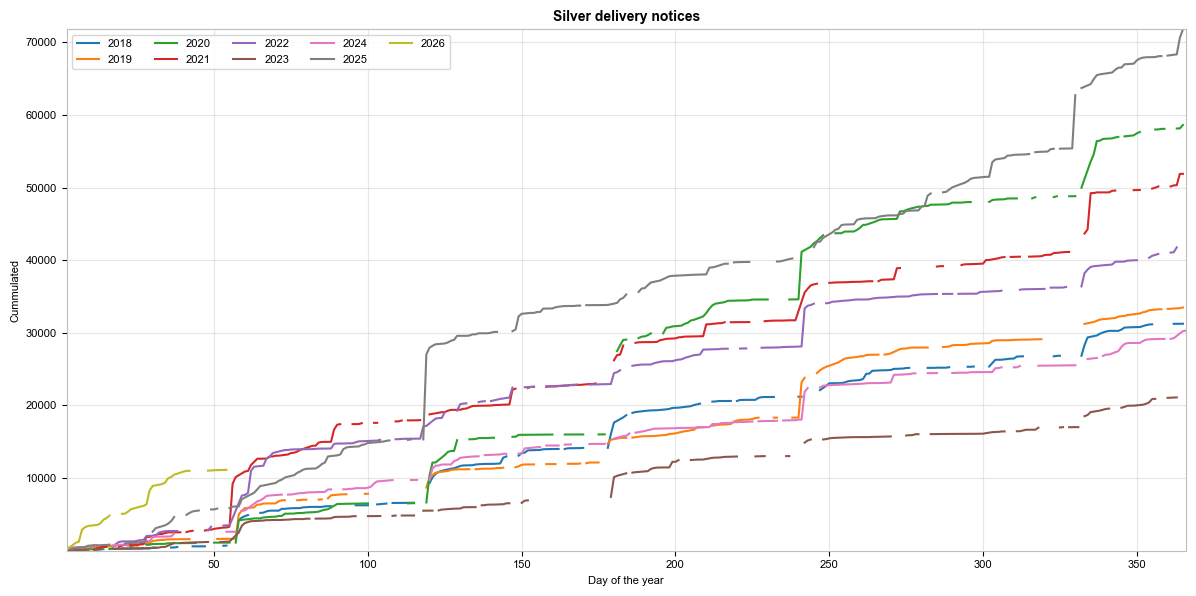

- Approximately two-thirds of the March contract positions have already been rolled over. While there has been no surge in delivery notices in recent days, the beginning of March remains a critical window when such notices typically rise significantly.

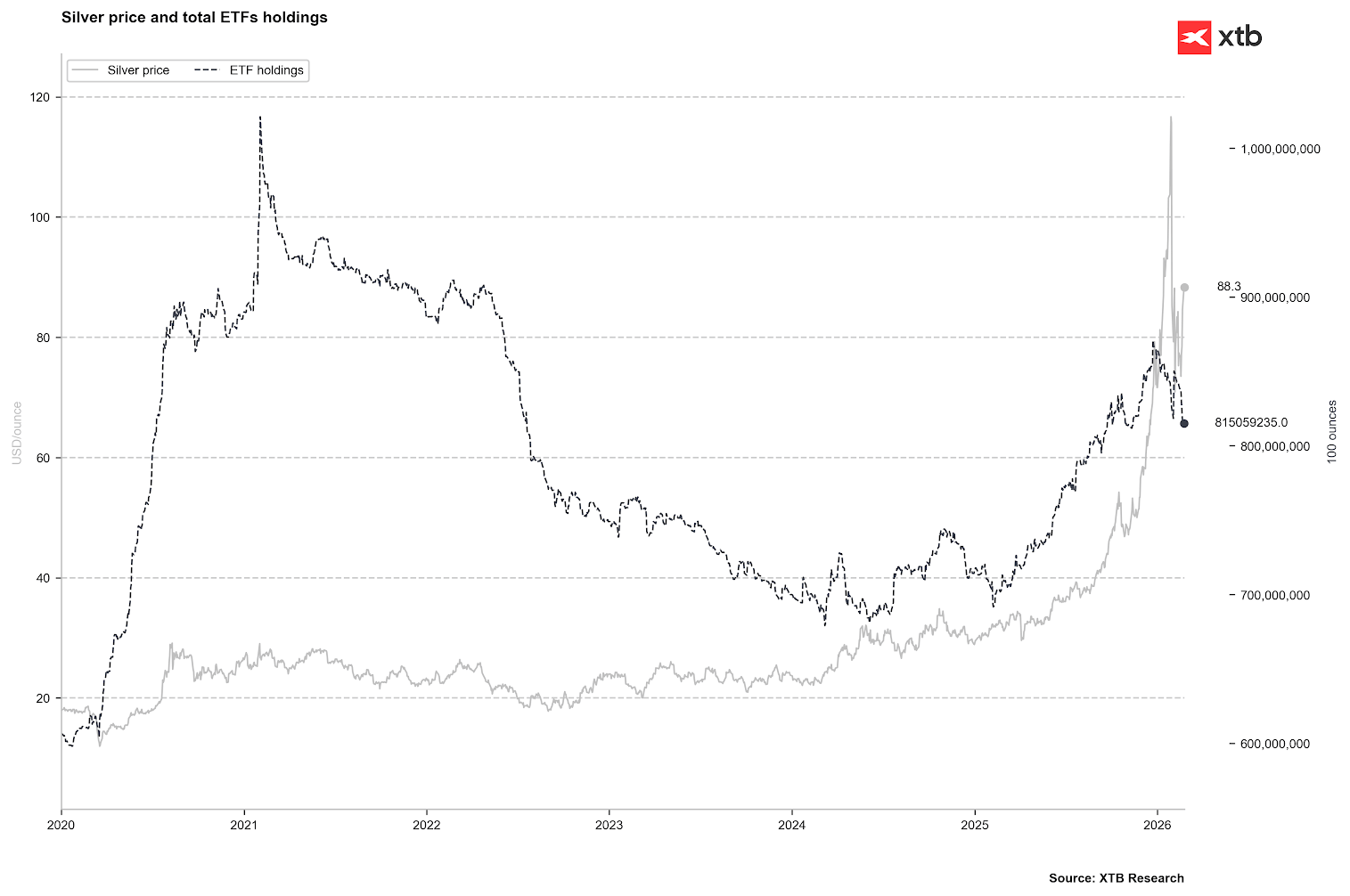

- ETF funds continue to liquidate silver holdings; COMEX inventories are falling sharply but remain at relatively high levels, even amidst increased demand for physical delivery.

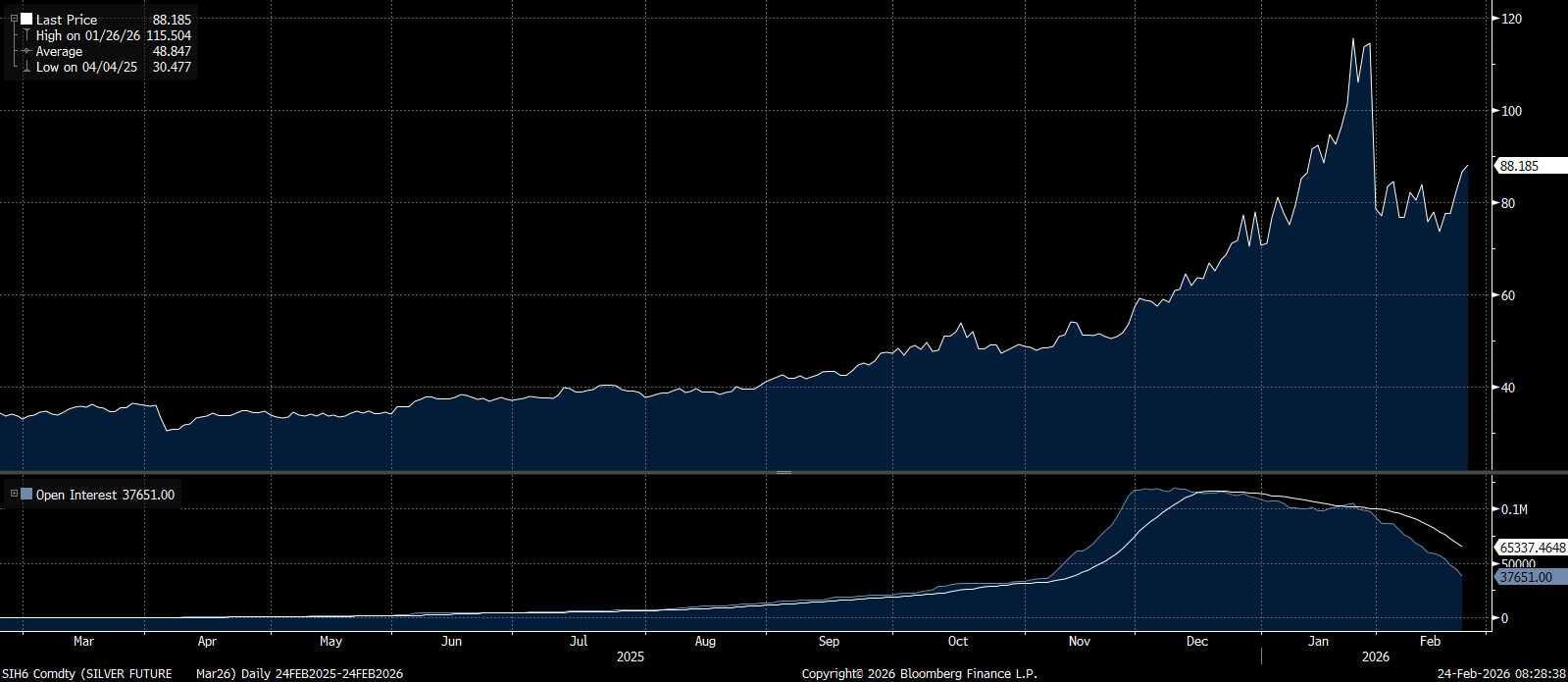

Open interest on the March contract currently stands at 37,000 contracts. The decline in open positions is notably more pronounced than in previous delivery months. Source: Bloomberg Finance LP

Open interest on the March contract currently stands at 37,000 contracts. The decline in open positions is notably more pronounced than in previous delivery months. Source: Bloomberg Finance LP

Delivery notices have stalled for some time, but the critical period ahead of the March contract rollover looms. Source: Bloomberg Finance LP, XTB

Delivery notices have stalled for some time, but the critical period ahead of the March contract rollover looms. Source: Bloomberg Finance LP, XTB

ETFs continue their silver sell-off. Notably, similar levels in November triggered a price rebound. Source: Bloomberg Finance LP, XTB

ETFs continue their silver sell-off. Notably, similar levels in November triggered a price rebound. Source: Bloomberg Finance LP, XTB

Silver has rallied to a key resistance level corresponding to the post-correction highs following the late-January price slump. Further aggressive trade policy moves by Trump or a US strike on Iran could push prices above $100 per ounce. However, approximately $10 of the current price is estimated to be a direct result of recent risk escalation. Source: xStation5

Silver has rallied to a key resistance level corresponding to the post-correction highs following the late-January price slump. Further aggressive trade policy moves by Trump or a US strike on Iran could push prices above $100 per ounce. However, approximately $10 of the current price is estimated to be a direct result of recent risk escalation. Source: xStation5

Natural Gas:

- Natural gas prices have retreated below $3/MMBTU following a sudden spike in demand in recent days. Weather outlooks suggest a significant drop in heating requirements over the next two weeks.

- Early-week production reached nearly 114 bcfd, up 9% year-on-year. Demand exceeded averages at 108.2 bcfd (+15% YoY).

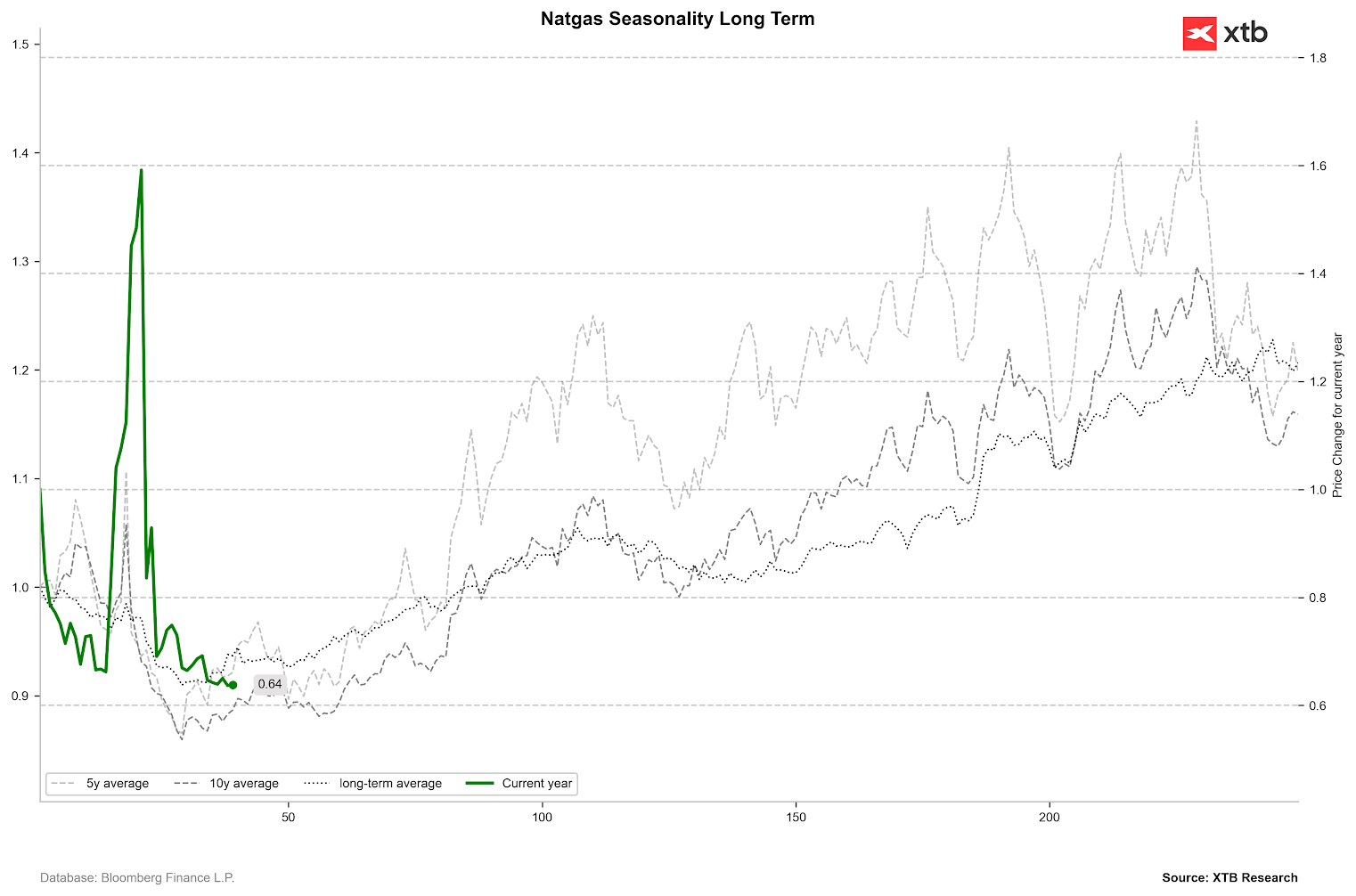

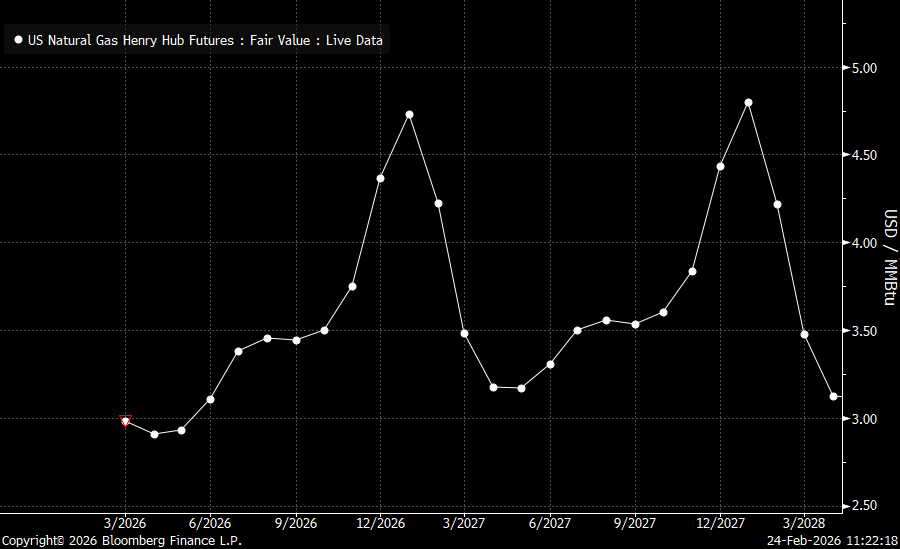

- Seasonality suggests flat price action in the near term. The market is currently in slight backwardation for the front two contracts but remains in deep contango for the remainder of the year, signaling significant oversupply (low current prices relative to high expectations for the next heating season).

Heating degree days are once again falling sharply below the 5-year average. Source: Bloomberg Finance LP

Heating degree days are once again falling sharply below the 5-year average. Source: Bloomberg Finance LP

Seasonality indicates a stabilization of gas prices in the near term. Source: Bloomberg Finance LP, XTB

Seasonality indicates a stabilization of gas prices in the near term. Source: Bloomberg Finance LP, XTB

A very steep contango is observed between the current contract and January 2027. Theoretically, such strong contango signals heavy oversupply. Source: Bloomberg Finance LP

A very steep contango is observed between the current contract and January 2027. Theoretically, such strong contango signals heavy oversupply. Source: Bloomberg Finance LP

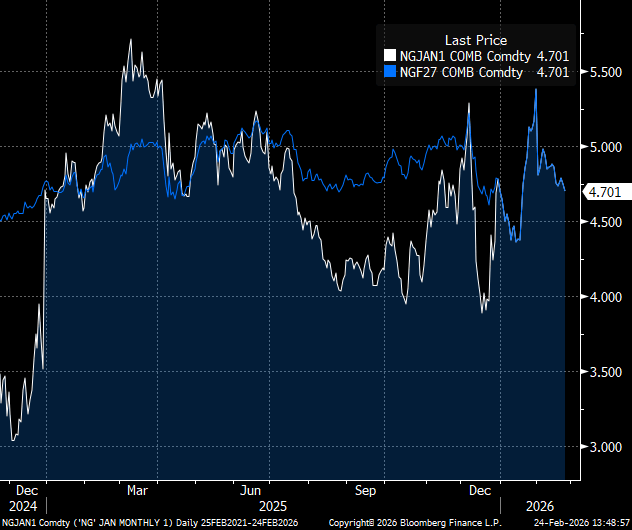

Comparison of January continuing contracts (white line) with the January 2027 contract (blue line). Prices are beginning to fall significantly, suggesting that amid expected oversupply, forward prices may remain excessively high. Source: Bloomberg Finance LP, XTB

Comparison of January continuing contracts (white line) with the January 2027 contract (blue line). Prices are beginning to fall significantly, suggesting that amid expected oversupply, forward prices may remain excessively high. Source: Bloomberg Finance LP, XTB

Cocoa:

- Cocoa prices are attempting to stabilize slightly above $3,000 per tonne, following a nearly 50% decline this year and a drop of over 75% from historical peaks (excluding futures contract rollovers).

- The price collapse is attributed to a lack of physical demand. International processors and exporters are reluctant to purchase West African beans as local prices remain above market rates.

- Ahead of elections in Côte d’Ivoire, the guaranteed farmgate price was raised to $5,000 per tonne. The “mid-season” price for April is expected to be announced at month-end; the Ministry of Agriculture is considering significant price cuts, similar to recent moves in Ghana.

- Ghana recently slashed its price by nearly 30% to $3,700 per tonne, which remains above current market levels.

- The current and upcoming harvest seasons are expected to yield an oversupply of 200,000 to 300,000 tonnes, following several years of deep deficits that had pushed prices above $12,000 per tonne.

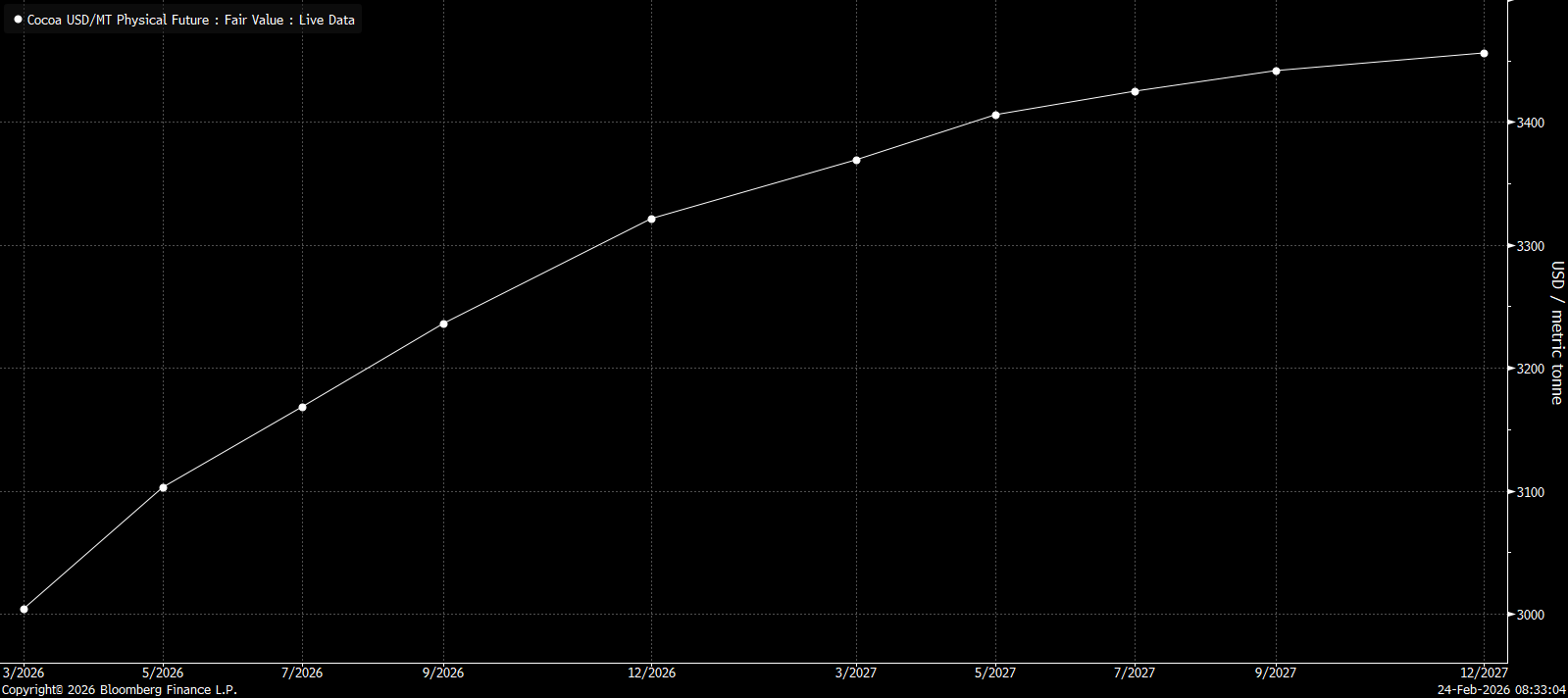

- The forward curve for cocoa is currently in contango, with a spread of just over $400 between the front month and the end of 2027.

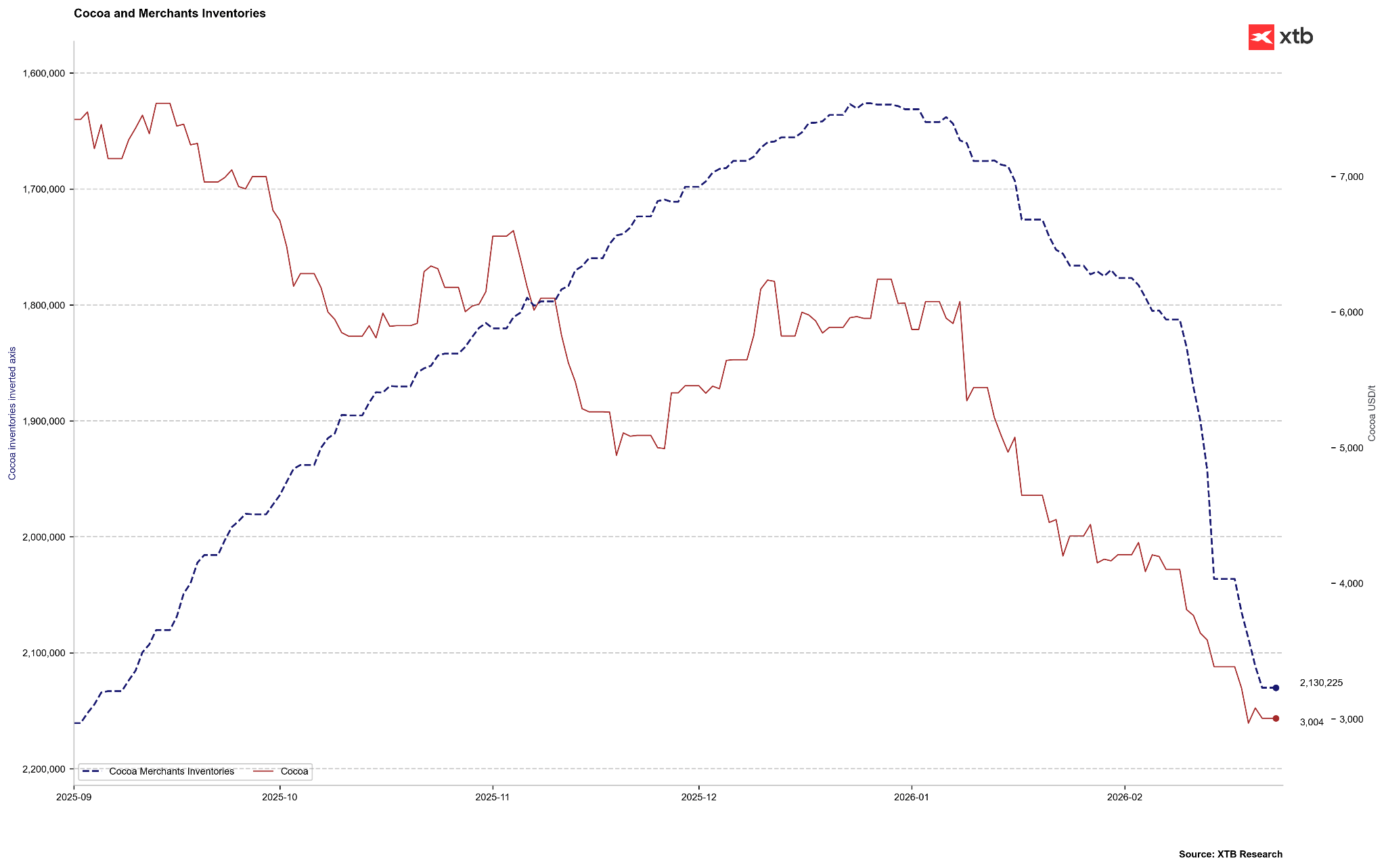

- Signs of oversupply are emerging on terminal exchanges; ICE inventories have risen to over 2.1 million bags, hitting a nearly six-month high.

The cocoa market is in clear contango. The curve structure suggests classic market oversupply. Source: Bloomberg Finance LP, XTB

The cocoa market is in clear contango. The curve structure suggests classic market oversupply. Source: Bloomberg Finance LP, XTB

ICE inventories are rising significantly to over 2.1 million bags. The current accumulation resembles periods of significant oversupply. Source: Bloomberg Finance LP, XTB

ICE inventories are rising significantly to over 2.1 million bags. The current accumulation resembles periods of significant oversupply. Source: Bloomberg Finance LP, XTB

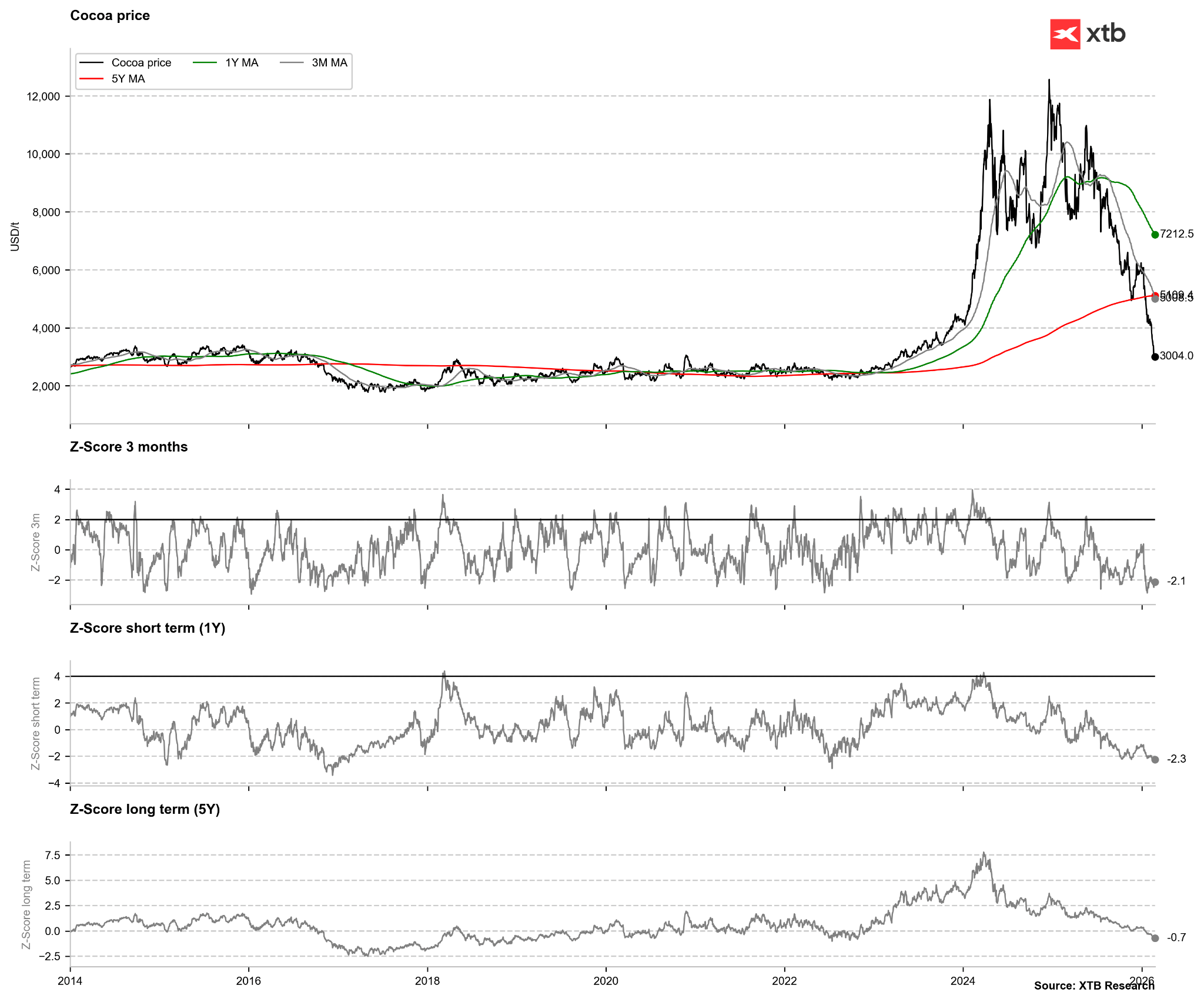

Cocoa is extremely oversold from a technical perspective. Significant undervaluation is evident relative to both the 3-month and 1-year moving averages. While cocoa is oversold relative to the 5-year average, it has not yet reached the extremes seen in 2017. Source: Bloomberg Finance LP, XTB

Cocoa is extremely oversold from a technical perspective. Significant undervaluation is evident relative to both the 3-month and 1-year moving averages. While cocoa is oversold relative to the 5-year average, it has not yet reached the extremes seen in 2017. Source: Bloomberg Finance LP, XTB

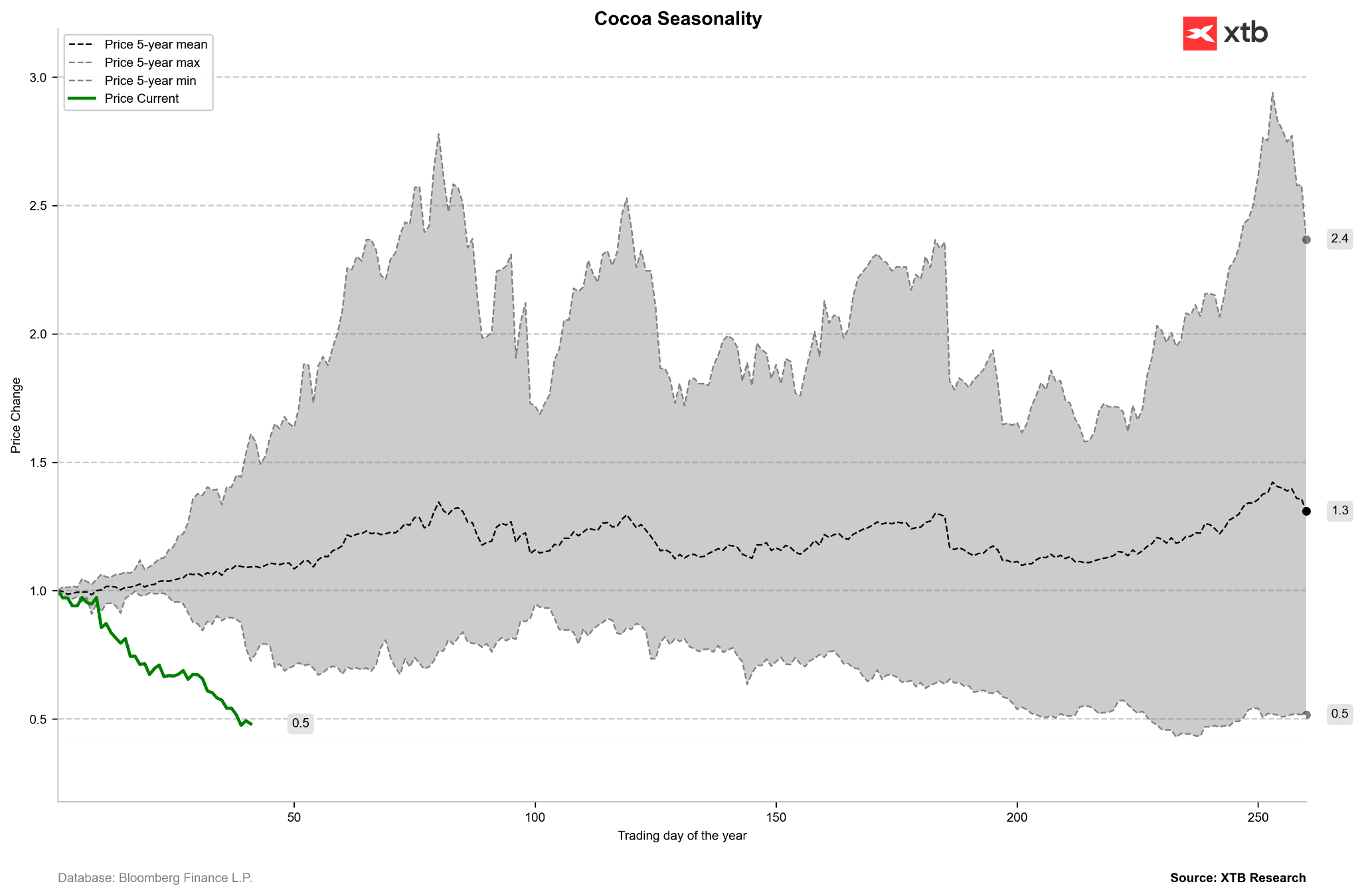

Cocoa prices are falling sharply at the start of the year, contrary to typical seasonality. Historical performance over the last 5 years suggests stabilization may be imminent. Source: Bloomberg Finance LP

Cocoa prices are falling sharply at the start of the year, contrary to typical seasonality. Historical performance over the last 5 years suggests stabilization may be imminent. Source: Bloomberg Finance LP

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.