BOE preview: To pivot, or not to pivot

It’s hard not to feel sympathy for the Bank of England ahead of today’s monetary policy meeting. Less than three weeks ago there was an 80% chance of a rate cut at this meeting, now there is a small chance of a hike. This 180-degree turn in rate cut expectations has nothing to do with the BOE or the UK economy, and everything to do with the Middle East conflict that is causing an historic energy price spike.

BOE tries to buy some time

The BOE is expected to remain on hold today, and we think that the nature of the inflationary threat the UK now faces, means that the BOE will try to buy some time to see how the war plays out in the coming weeks and months. Donald Trump keeps telling us that the war will be over soon and a weakened Iran will lead to permanently lower oil prices, however, others are concerned that there is no end in sight to the conflict and it could drag on for months.

The MPC’s dilemma at this meeting is whether to worry more about inflation or the weakening growth outlook.

Why we are not going back to 2022

The risk is that central bankers, typically a conservative bunch, spook markets with bleak outlooks. The inflation shock of 2022, when global inflation rates surged to double figures are still painful for central bankers including the BOE, who were accused of being behind the curve. Bailey and co. will be sensitive to the mistakes of the past and if this forces them to focus on inflation rather than growth, it could further weigh on risky assets like stocks and hurt Gilts, causing yields to rise.

However, we think that there is a good chance that the BOE will want to stress the unique position that it finds itself in. Firstly, things are very different now compared to 2022 when Russia invaded Ukraine. Back then, the UK economy was strong, there was a post-covid boost, unemployment was at historically low levels, wages were rising rapidly and the consumer was happy to spend. The current energy price spike is happening when the UK economy is weak. There was no growth in January, and the economy has been limping along for months. The unemployment rate is also rising sharply and further increases in the jobless rate are expected in the months ahead. There is a youth unemployment crisis, and recruiters will tell you that it’s taking longer and is far harder to find a job.

A hawkish move from the BOE would be a major policy mistake

This is not the environment to hike rates, pressuring mortgage holders and hurting consumer confidence. If the BOE does suggest that rate hikes could be coming, this would be a major policy mistake in our view and would likely put the brakes on consumer spending and worsen the UK’s economic outlook.

1.8 million UK mortgage holders are expected to refinance in 2026, if they have to pay more for their mortgage, this would be disastrous in an already weak economy.

A high bar for a rate hike

Instead, we expect the BOE to be pragmatic about the current situation in the Middle East. While they are likely to stress the uncertainty and volatility of the situation, they may say that the economy is weak enough that higher energy prices will only weaken the economy further. Rather than a pure inflation threat like the energy price spike was in 2022; it is now an economic threat that could weaken our economy even more. The main message from today’s meeting could be that the bar is high for a rate hike on the back of the energy price spike, even if inflation risks remain to the upside.

Why the BOE may be more 2011 than 2022

Slamming on the brakes to slow the economy was obvious in 2022, it is not in 2026. Added to this, back in 2011, when energy prices were also elevated, the BOE did not hike interest rates. The economy was also vulnerable back then, and the BOE was more focussed on supporting a weaker economy rather than focussing on the inflationary risks. Due to this, we expect the BOE to be more 2011 than 2022, and we expect the BOE to be mindful of supporting the economy through a tough economic period ahead.

The market impact

The market impact could also be nuanced. Although the BOE is expected to keep policy unchanged, what they say about the impact from an energy price spike on their inflation and monetary policy forecasts may have a major impact on the pound. However, ultimately the oil price is driving the bus right now and where oil goes the market will follow. If the oil price rises, it will add upward pressure to the dollar and this could weaken sterling, but if the oil price retreats, it gives the pound a chance to recover.

As you can see in the chart below, the path of least resistance is for a lower GBP/USD. The cable rate is below its 200-day sma, which is a sign that long term momentum is to the downside. If the BOE is less hawkish than expected, we could see more pound weakness and the next key support level is last week’s low around $1.32.

EUR/GBP is a purer play on the BOE meeting as it will not be as directly impacted by movements in the dollar. The pound has outperformed the euro for the duration of this conflict, but EUR/GBP put in a low ahead of 0.8600, if the pound does weaken on the back of this BOE meeting, then we may see further EUR/GBP strength towards 0.8685, the 50-day sma. The ECB is also meeting today; however, they were biased towards a prolonged pause in rate cuts before this crisis, and we doubt that they will be as concerned about the growth outlook as the BOE. This opens the door to further EUR/GBP recovery, in our view.

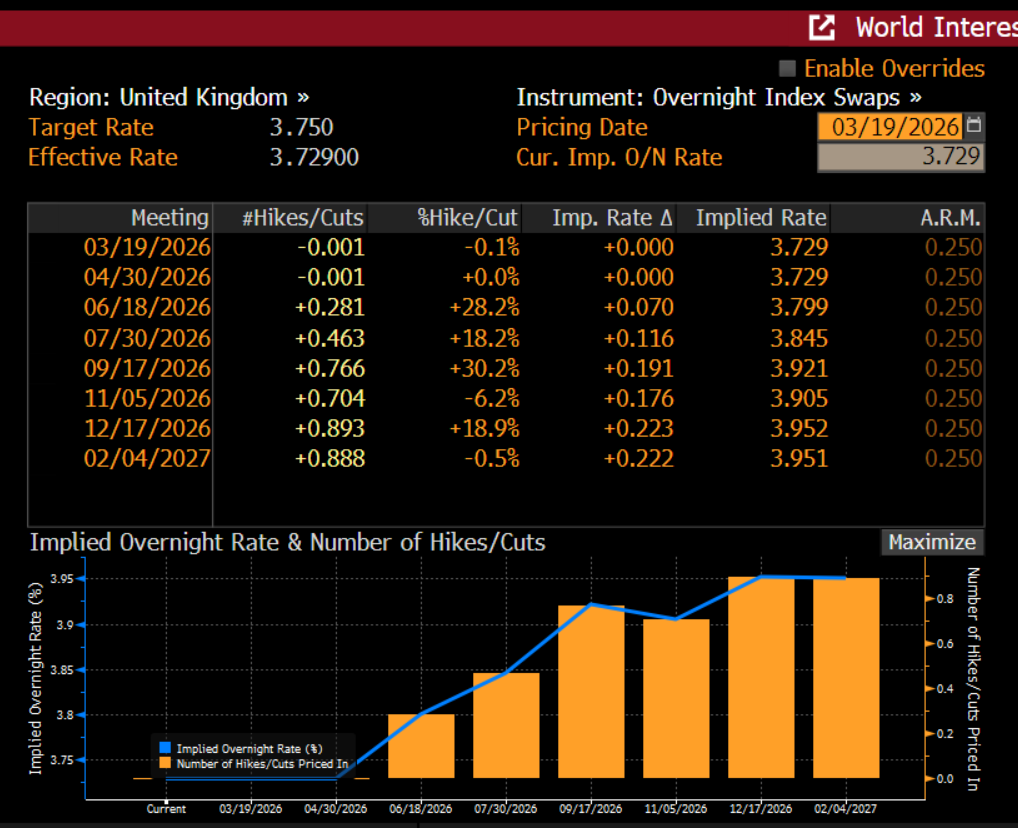

Chart 1: The UK overnight swaps market is now pricing in a high chance of a rate hike this year

Source: XTB

Chart 2: EUR/GBP

Source: XTB

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.